Belden has had an impressive run over the past six months as its shares have beaten the S&P 500 by 13.8%. The stock now trades at $120.71, marking a 28% gain. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Belden, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.We’re glad investors have benefited from the price increase, but we don't have much confidence in Belden. Here are two reasons why BDC doesn't excite us and a stock we'd rather own.

Why Is Belden Not Exciting?

With its enamel-coated copper wire used in WWI for the Allied forces, Belden (NYSE: BDC) designs, manufactures, and sells electronic components to various industries.

1. Long-Term Revenue Growth Disappoints

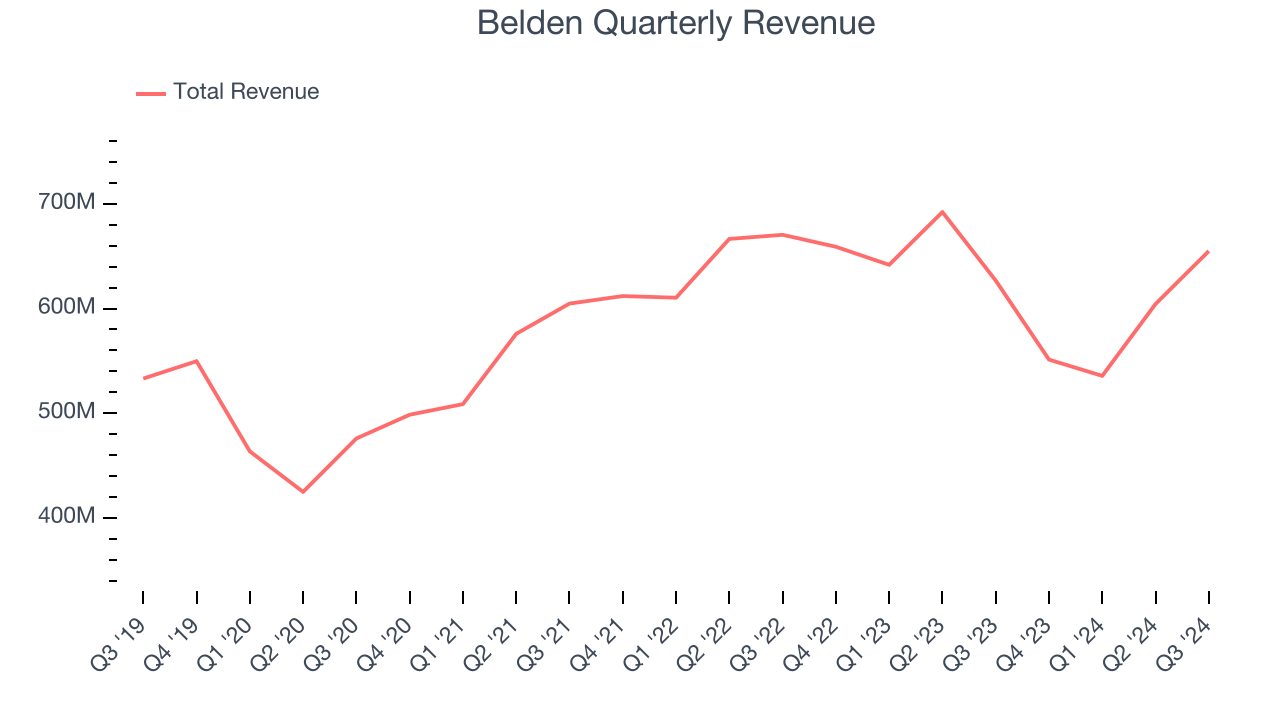

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Belden’s sales grew at a sluggish 1.9% compounded annual growth rate over the last five years. This fell short of our benchmarks.

2. EPS Barely Growing

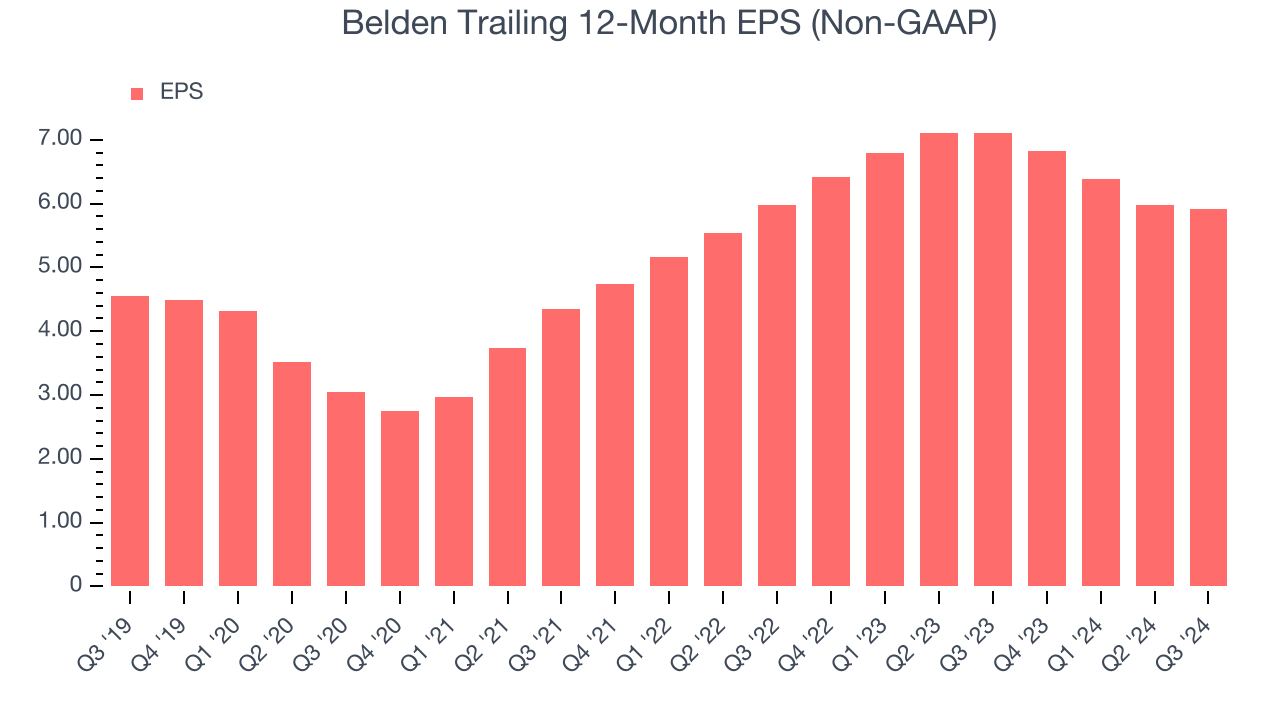

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Belden’s EPS grew at an unimpressive 5.4% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 1.9% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

Belden’s business quality ultimately falls short of our standards. With its shares topping the market in recent months, the stock trades at 16.8x forward price-to-earnings (or $120.71 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at Yum! Brands, an all-weather company that owns household favorite Taco Bell.

Stocks We Would Buy Instead of Belden

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.