Alibaba (BABA) stock has traded sideways for the last three weeks after a drastic fall in the first two months of the year. This is usually an ideal time to buy for those looking to accumulate shares. It doesn’t come as a surprise that Michael Burry was doing exactly that. Burry disclosed that Alibaba was a significant part of his portfolio at just over 6%. He believes the stock’s weak year-to-date (YTD) performance offers an entry point that is too good to ignore.

While Burry’s bets are often based on risks that the market continues to ignore, he has had a good few months after questioning the sustainability of the AI trade and pointing out the lack of accounting transparency in the way companies book their AI investments. The Mag 7 has struggled in the recent past, and so people have started taking the famed investors more seriously than before. His recent stake in Alibaba comes in addition to his significant position in JD.com (JD) and GME (GME).

About Alibaba Stock

Alibaba offers technology infrastructure and marketing tools to retailers, merchants, brands, and other businesses. The company operates major e-commerce platforms such as Tmall, AliExpress, and Taobao, as well as international platforms like Daraz and Lazada. It also provides food delivery, logistics, maps, entertainment, and video streaming. Alibaba was founded by Chung Tsai and Yun Ma in 1999.

The company's stock delivered a 22% return over the last year, consistent with the broader index. However, looking at the stock’s performance so far this year, it is down 13%, while the S&P 500 ($SPX) is barely in the green at only 0.4%. There's no doubt the stock has been a poor performer, but that is precisely what brings the opportunity.

Alibaba is expected to grow its earnings at 50% in fiscal 2027 and 32% in fiscal 2028. These are impressive growth numbers, but the problem is that the company is based in China. Investors, therefore, don’t look at the forward P/E of 22.52x in the same way as they do Nvidia’s (NVDA), which has the same multiple on slower growth. Unfortunately, as a Chinese company, Alibaba can do nothing about this perceived risk.

On a forward price-to-sales basis, the multiple of 1.9x is 20% below its own five-year average multiple of 2.36x. The forward price-to-cash-flow ratio of 14.95 is trading at a 31.26% premium to its historic average. These numbers may not look attractive enough, but considering the firm is a major AI player in China, the upside could be huge. Just today, the company revealed that its “Happy Horse” Video AI model had claimed the top spot in global rankings, possibly hinting at the exact attraction that Michael Burry finds in the stock. If something like this materializes, the valuation would be the last concern for investors.

Alibaba's Ambitious $100 Billion Plan

Alibaba reported its third-quarter fiscal 2026 earnings on March 19. As reported, the company’s total revenue for the quarter reached RMB 284.8 billion. The China e-commerce segment generated RMB 159.3 billion in revenue, marking a 6% increase. Revenue from quick commerce came in at RMB 20.8 billion, up 56%. However, due to higher spending on quick commerce and technology, the adjusted EBITA for the China E-commerce business fell 43%.

Going forward, the company aims to generate over $100 billion in combined cloud and AI external revenue over the next five years, including Mobility as a Service (MaaS). CEO Yongming Wu expects MaaS to become the biggest revenue contributor within the Cloud Intelligence segment. According to the management, the quick commerce business is likely to turn profitable by fiscal 2029. These opportunities once again point to the thesis that Michael Burry might be more impressed by the growth prospects than an attractive valuation.

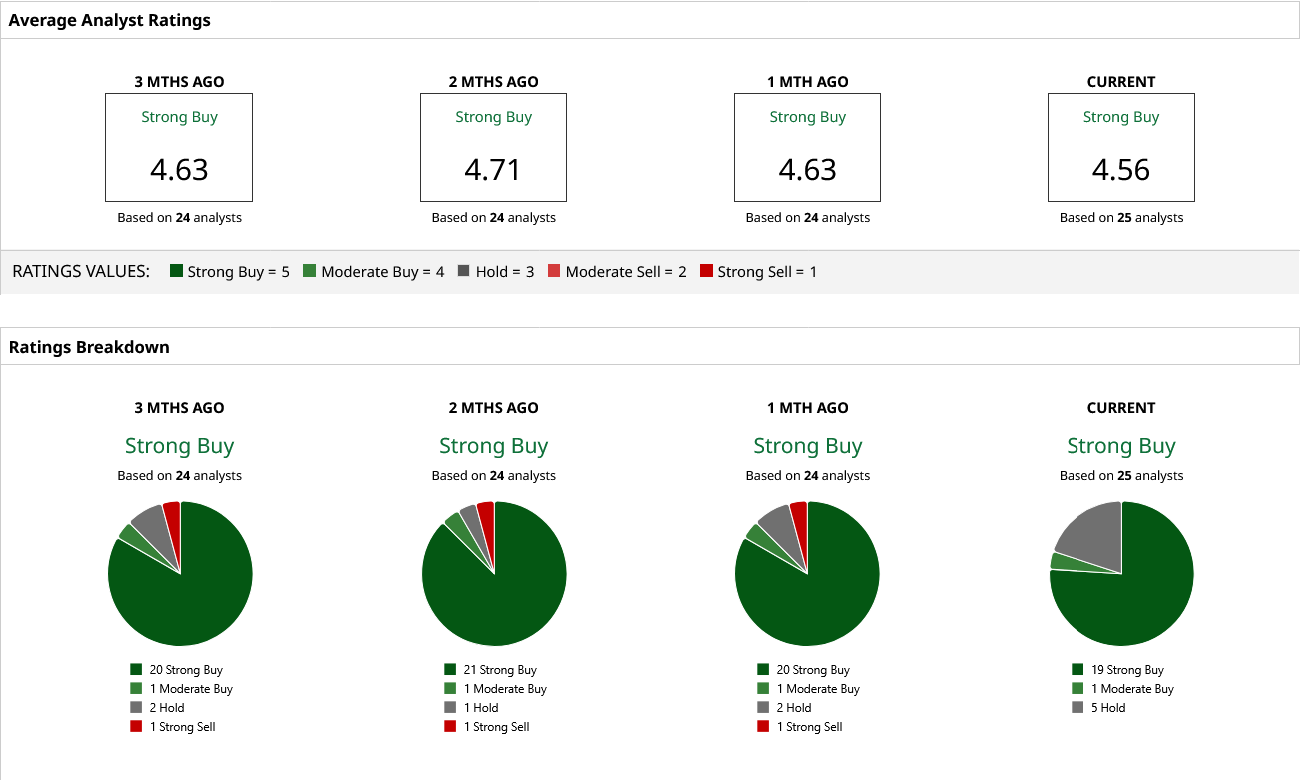

What Are Analysts Saying About BABA Stock?

On April 10, CBM International Securities analyst Saiyi He raised the firm’s price target on the stock from $203.70 to $206.10 while keeping a “Buy” rating. In contrast to CBM International Securities, Jefferies cut its price target on Alibaba while maintaining a “Buy” rating on April 8. Jefferies analyst Thomas lowered the firm’s price target on the stock from $212 to $185.

The 25 analysts covering the stock on Wall Street have a consensus “Strong Buy” rating. The most bullish sentiment suggests that the stock could jump to $206.10, which offers impressive upside of approximately 62%.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart