When the man who predicted the 2008 housing collapse starts buying a stock, it tends to get people's attention. Michael Burry, the hedge fund manager made famous by the film "The Big Short," recently disclosed he added shares of JD.com (JD) and opened a new position in Alibaba (BABA).

Burry wrote in a post on Substack that he viewed recent weakness in both stocks as “an attractive entry point.” JD.com's stock rose roughly 2% on the news. But a single day of momentum is not a thesis. So what exactly is Burry seeing? And more importantly, does the underlying business hold up?

Michael Burry Turns Bullish on JD.com Stock

Burry told his Substack subscribers that JD represents "a significant add" to his portfolio, with the position now slightly above 6% of his holdings. Alibaba was also described as a new position at just over 6%. JD.com stock has pulled back and is trading 24% below its 52-week high, making it attractive to Burry.

JD.com is China's second-largest e-commerce platform. It operates more like Amazon (AMZN) than a pure marketplace. The company owns its own warehouses, employs its own delivery workers, and controls much of its supply chain from end to end.

That model is slower to scale but produces a more consistent experience for shoppers and, over time, stronger unit economics.

The fourth-quarter 2025 earnings call told a layered story.

- Total revenues for the quarter grew by 2% year-over-year (YoY) to approximately $52.8 billion.

- For the full year of 2025, total revenues climbed 13% to roughly $195 billion.

- JD Retail, the core business, reported an operating margin of 4.6%, up 52 basis points YoY.

- It was the sixth consecutive year of margin expansion for the business segment.

CFO Ian Shan said the company's long-term margin target of high single digits remains unchanged. JD.com CEO Sandy Xu also highlighted multiple near-term growth drivers.

- General merchandise revenue rose 12.1% in the fourth quarter and 15.3% for the full year.

- Categories like supermarket, fashion, and health care all posted double-digit growth.

- Quarterly active customers grew 30% YoY in the fourth quarter, and the company crossed 700 million annual active customers for the first time.

- User shopping frequency surged more than 40% YoY for the full year.

JD Stock Is Not Without Risks

None of this means JD stock is without execution risk.

- JD.com's electronics and home appliances segment, historically one of its biggest revenue drivers, fell 12% in the fourth quarter due to a tough YoY comparison with a government trade-in subsidy program that pulled demand forward in early 2025. Management acknowledged that the headwind will linger into the first half of 2026.

- The company is also investing heavily in new businesses. Its food delivery venture, JD Food Delivery, is still losing money, though losses narrowed by nearly 20% quarter-over-quarter in the fourth quarter.

- JD is expanding internationally, launching Joybuy in Europe in March 2026 with same-day and next-day delivery in the UK, Germany, France, and the Netherlands. These bets require capital and long-term execution.

Free cash flow for 2025 came in at approximately $900 million, down 85% YoY, largely due to cash outflows tied to the trade-in program. However, analysts forecast JD.com to improve free cash flow to $8.6 billion in 2028. JD.com ended 2025 with $33.75 billion in cash, repurchased 6.3% of its outstanding shares for $3 billion, and declared a cash dividend of $1 per share in 2025.

The Final Takeaway

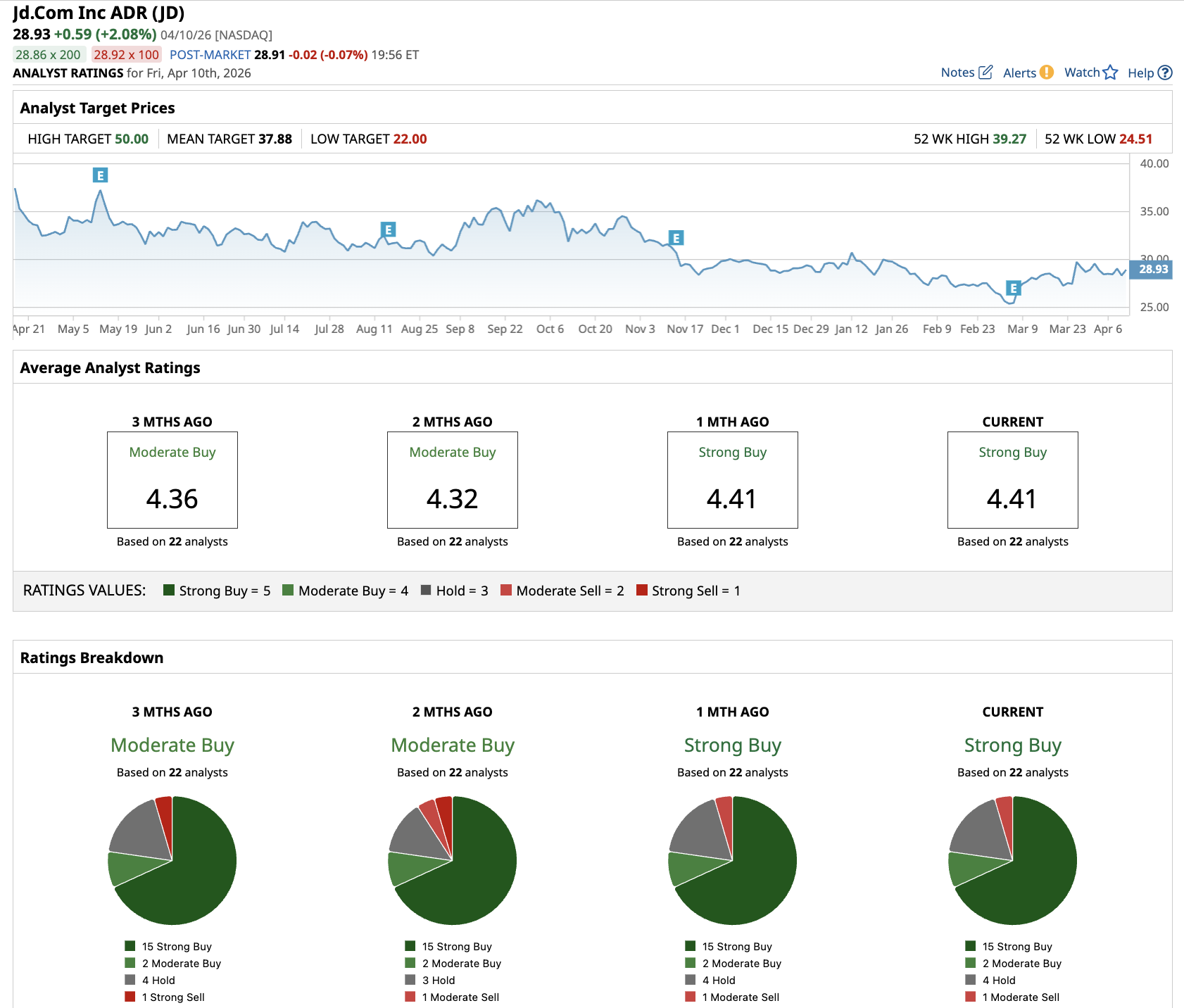

Out of the 22 analysts covering JD stock, 15 recommend “Strong Buy,” two recommend “Moderate Buy,” four recommend “Hold,” and one recommends “Moderate Sell.” The average JD price target is $37.88, above the current price of about $29.

If JD stock is priced at 10 times forward FCF, it could more than double over the next two years. Burry is making the case that the market has overpenalized JD.com for near-term noise while the underlying business keeps growing, margins keep expanding, and users keep coming back more often.

Whether you follow him depends on your comfort level with Chinese equities, your investment horizon, and your tolerance for volatility. But the business itself is worth a close look.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart