Berkshire Hathaway (BRK.A), the U.S. multinational holding company, is still adding to its big Japan bet. The company has increased its stake in Sumitomo (SSUMY) to 10.05% as of May 7, pushing past the key 10% mark and looking more like a long-term partner than just a large investor.

With this move, Berkshire now owns more than 10% of all five major Japanese trading houses, a bet that started in 2019 and has kept growing under new leadership. This comes at a time when Japan’s economy is gaining momentum, helped by the Bank of Japan’s rate hike from 0.5% to 0.75%, the highest level in about 30 years.

Berkshire’s stakes in Mitsubishi (MSBHF), Mitsui (MITSF), Itochu (ITOCF), Marubeni (MARUF), and Sumitomo are now worth more than $30 billion combined, and they throw off hundreds of millions of dollars in dividends each year. The timing is notable, arriving just days after Greg Abel led his first Berkshire annual meeting as CEO, where he described the Japanese holdings as long-term, “permanent” investments meant to deliver steady income and growth over many years.

What does Berkshire see in Sumitomo right now that makes a 10%-plus stake worth holding for decades? Let’s take a closer look.

Sumitomo’s Numbers Back Berkshire’s Patience

Headquartered in Tokyo, Japan, Sumitomo operates across resources, energy, infrastructure, machinery, and consumer businesses in markets around the world. That gives it several income streams and helps explain why long-term investors are interested in the stock.

U.S.-listed shares of Sumitomo recently traded around the $46 mark, with the stock up 33% so far this year and almost 84% over the past 52 weeks.

SSUMY trades at 14.1 times trailing earnings and 10.9 times price-to-cash flow, compared with sector medians of 26.7 times and 14.8 times. That suggests the stock still trades at a discount to its sector. Sumitomo's market capitalization is about $55.13 billion, and the company also offers a forward annual dividend of $0.68 per share with a 1.45% yield.

Sumitomo released its latest results on May 1, posting quarterly EPS of $1.02. Full-year figures for the period ending March 2026 show sales of $48.74 billion, a small 0.20% increase that still points to a steady top line amid a tougher backdrop.

The company generated net income of $3.98 billion for the year, up 6.4% year-over-year (YOY), which shows that profits are growing faster than revenue as margins improve. Operating cash flow reached $4.08 billion, so earnings are clearly supported by cash coming into the business rather than just accounting gains.

However, Sumitomo’s net cash flow came in at -$648 million, marking a massive change from $73 million in the prior year. This swing mainly reflects heavier spending and investment, the sort of capital deployment that can help drive the next leg of growth.

Sumitomo’s Satellite Bet

Sumitomo is pushing hard into high-growth tech areas. Last year, the company took an equity stake in Ursa Space Systems, a U.S. satellite intelligence company that uses radar satellites and data analysis to turn images into useful information for businesses and government agencies.

Announced in August 2025, the deal also gives Sumitomo exclusive rights to market and support Ursa Space Systems' services in Japan. This partnership puts Sumitomo right in the middle of the growing commercial geospatial intelligence market, where Ursa already works with clients such as the U.S. National Geospatial-Intelligence Agency.

Analyst Confidence Lines Up With Berkshire’s Patience

Sumitomo's next earnings release is set for July 30. The full-year view is clear, with forecasts for the year ending March 2027 calling for EPS of $3.45, up from $3.31 last year. That would represent a steady 4%-plus gain, which fits the kind of reliable growth Berkshire likes.

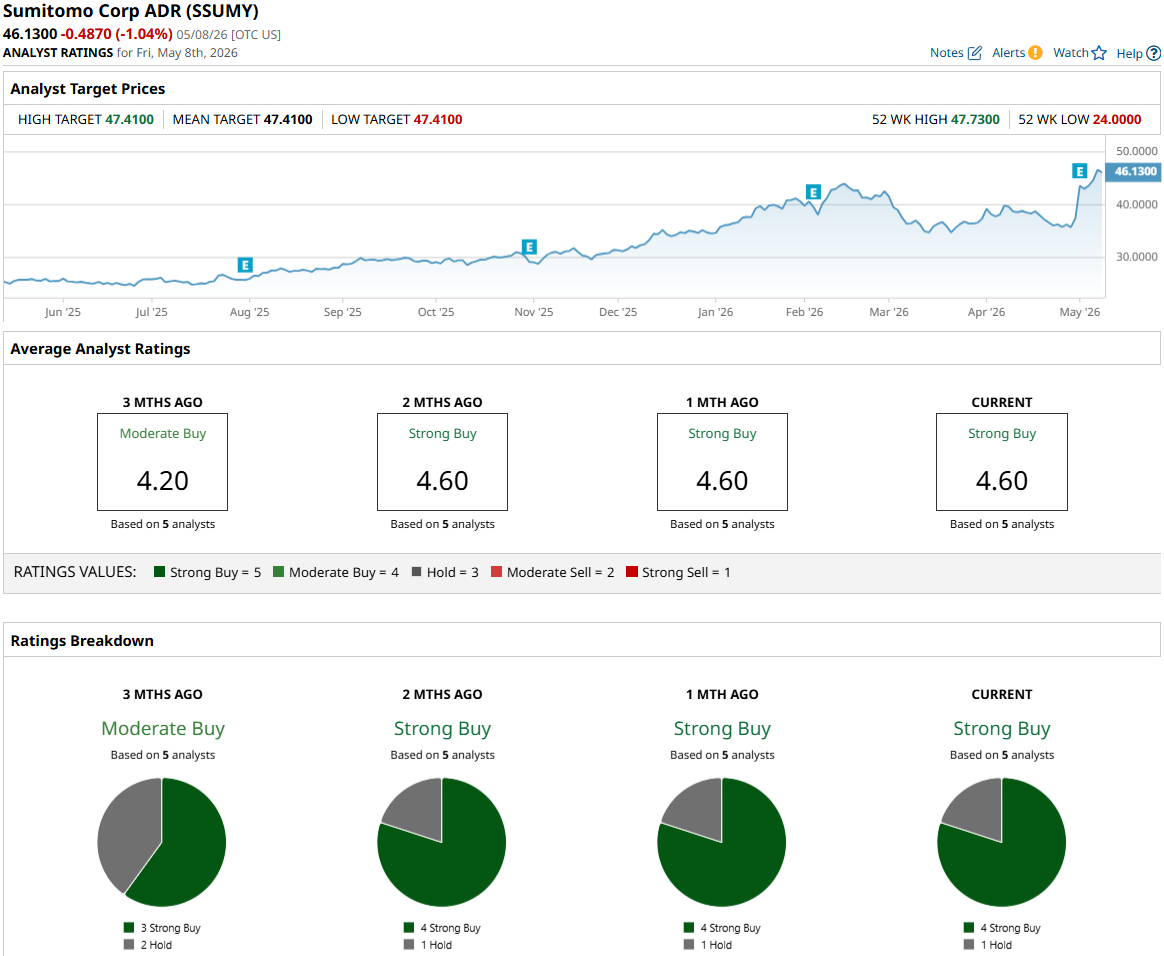

On the rating front, five analysts covering SSUMY stock have landed on a consensus “Strong Buy" rating. The average 12‑month price target is $47.41, which points to about 3% potential upside from here, on top of strong recent gains and a growing dividend.

Conclusion

Berkshire raising its Sumitomo stake above 10% and planning to hold it for decades points to a slow and steady income story, not a quick flip. Sumitomo still trades at a fair price compared with its sector, and its earnings and cash flow are moving in the right direction with solid growth drivers behind them. With that backdrop, the balance of risk and reward looks tilted toward a slow move higher rather than a sharp drop, even if gains ease after the recent rally. Taken together, the stock appears to be set up for modest, medium-term upside.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Berkshire Hathaway Just Upped Its Stake in Sumitomo Stock. Greg Abel Says It’s Holding for the Long Term.

- After Major Layoffs, Block Stock Is Staging a Turnaround. CEO Jack Dorsey Says AI Is Leading the Way.

- This Analyst Just Raised the Price Target on Coherent Stock by 50%. What to Know.

- CoreWeave Stock Falls as the AI Growth Story Slows Down