In the high-stakes race to power artificial intelligence (AI), few companies have emerged as pivotal enablers quite like CoreWeave (CRWV). As hyperscalers and AI labs pour billions into compute capacity, investors are increasingly turning their attention to the infrastructure layer, and Wall Street is taking notice ahead of the company’s May 7 earnings report.

That growing optimism is now being underscored by Citigroup (C), where one analyst, Tyler Radke, is making a notably bullish call. Citi recently lifted its price target on CoreWeave shares to $155 from $126 while reiterating a “Buy” rating, citing surging demand for AI infrastructure, accelerating backlog growth, and expanding customer diversification as key drivers of upside. The firm expects backlog to grow as much as 35% to 40% quarter-over-quarter in Q1, signaling that demand for high-performance computing tied to generative AI remains far from saturated.

In addition, the firm pointed to long-term upside catalysts, including new deals with Jane Street and Meta Platforms (META) that could ramp through 2027 and potentially push CoreWeave beyond its $30 billion annual recurring revenue target.

On the margin side, the firm also believes that higher pricing for next-gen hardware and lower capital costs from investment-grade debt could support upward earnings revisions through 2026.

While the stock is already rebounding sharply and expectations are building into earnings, can CoreWeave deliver results strong enough to justify the mounting bullishness? Or has the bar been set too high?

About CoreWeave Stock

Based in Livingston, New Jersey, CoreWeave was founded in 2017 and has transformed from its roots in cryptocurrency mining into a top-tier provider of GPU-optimized cloud infrastructure for AI training and inference. With a current market cap of $56.65 billion, the company continues to expand its presence in the rapidly growing AI infrastructure market.

CoreWeave’s stock has been one of the most explosive and volatile AI trades since its public debut.

Following its March 2025 IPO at $40, the stock quickly turned into a momentum phenomenon. Within just a few months, shares surged massively, driven by blockbuster AI deals and enthusiasm around its positioning as a key GPU cloud provider. That early rally culminated in a sharp spike to its 52-week and all-time high of $187 in June 2025, marking one of the most dramatic post-IPO ascents in recent tech listings.

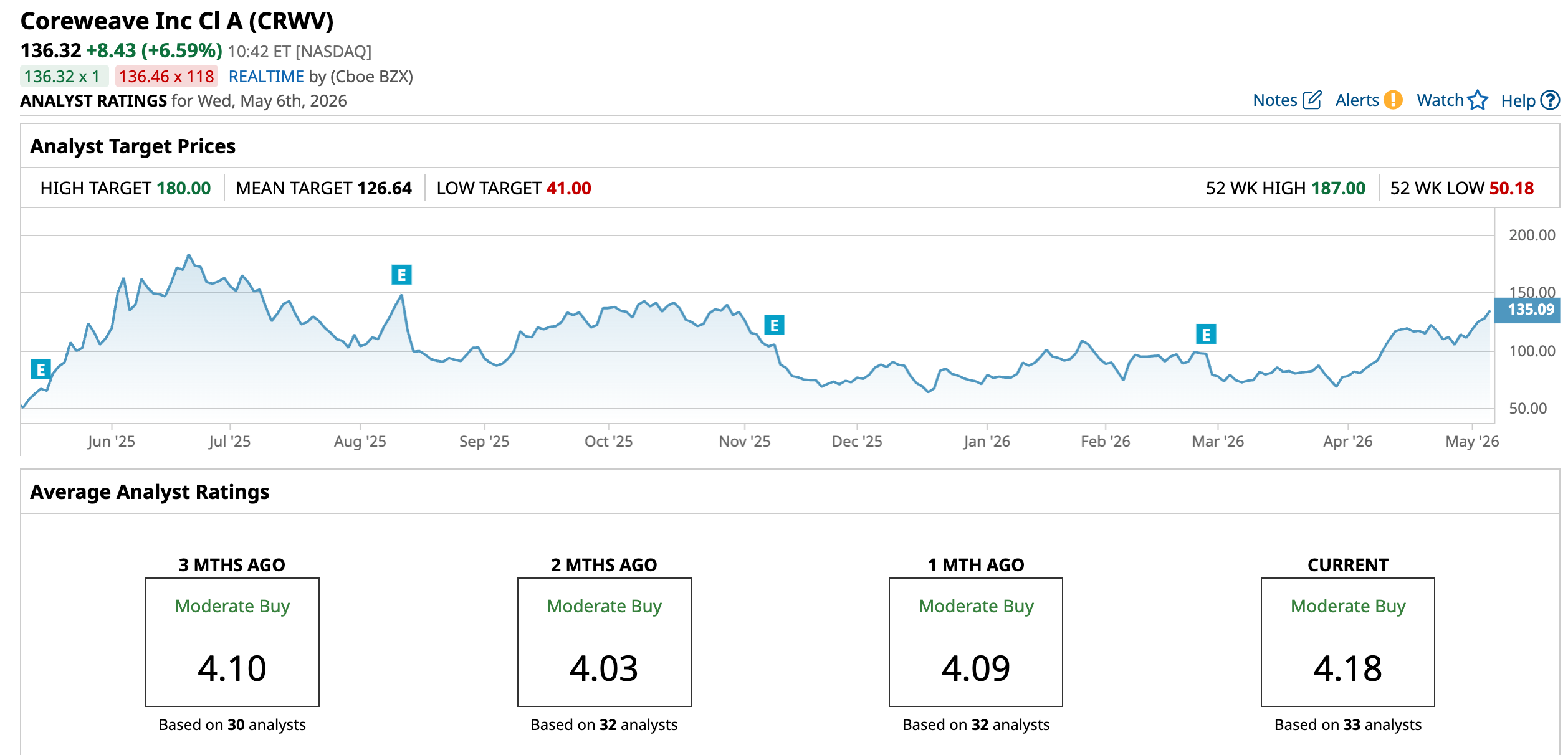

Over the past 52 weeks, the magnitude of the move remains striking. CoreWeave has delivered 143.73% returns over the past year, even after significant pullbacks from peak levels, underscoring the durability of investor interest despite volatility. The stock is up 84.78% year-to-date (YTD).

What stands out most is the stock’s extreme intraday and short-term volatility. CoreWeave has repeatedly posted double-digit single-day and multi-day jumps, following major announcements such as financing deals, Nvidia (NVDA) related developments, or large-scale contracts. Even in more recent trading, the stock continues to register wide daily jumps with 6.6% rise on May 1 and 5.4% climb on the next session, likely bolstered by the strengthening analysts’ optimism and price hikes.

The stock is currently trading at 5.56 times forward sales, which is a premium compared to its peers.

Steady Top Line Growth but Continued Bottom-Line Weakness

CoreWeave reported its fourth-quarter and full-year 2025 results on Feb. 26, marking its first full year as a public company and underscoring both the scale of AI-driven demand and the financial strain of rapid capacity expansion.

In the fourth quarter, revenue reached $1.6 billion, up 110.4% year-over-year (YOY), reflecting continued demand for AI compute infrastructure. However, this top line strength was offset by a significant deterioration in profitability. The company reported a loss per share of $0.89, compared with $0.34 a year earlier and below the consensus estimate. Adjusted EBITDA grew strongly, up roughly 84.7% YOY to about $898 million.

For the full year, CoreWeave delivered $5.13 billion in revenue, representing about 167.9% YOY growth, positioning it among the fastest-growing companies in the AI infrastructure space. Despite this, profitability moved in the opposite direction. Full-year loss per share came in around $2.81, compared to $4.30 in the prior year.

One of the most important structural metrics was backlog, which expanded dramatically to $66.8 billion, more than four times from the beginning of the fiscal year and provided strong forward revenue visibility.

Moreover, Q1 2026 revenue guidance stood at $1.9 billion to $2.0 billion, while the company is targeting $12 billion to $13 billion in full-year 2026 revenue. Also, CoreWeave outlined a plan of $30 billion to $35 billion in 2026 capital expenditures.

However, analysts anticipate losses to deepen in fiscal 2026, with loss per share expected to rise 54.3% YOY to $4.15, before improving 14.7% to $3.54 in fiscal 2027.

The consensus loss per share for the soon-to-be reported quarter (ended March 2026) is at 1.17, which is a 95% deterioration.

What Do Analysts Expect for CoreWeave Stock?

Recently, Jefferies raised its price target on CoreWeave to $160 from $120 and maintained a “Buy” rating, citing a series of major April deals, including agreements with Meta, Anthropic, and Jane Street. The firm sees strong ongoing demand for AI compute and views CoreWeave as well-positioned.

Also, last month, Cantor Fitzgerald raised its price target on CoreWeave to $156 from $149 and reiterated an “Overweight” rating after the $6 billion deal with Jane Street.

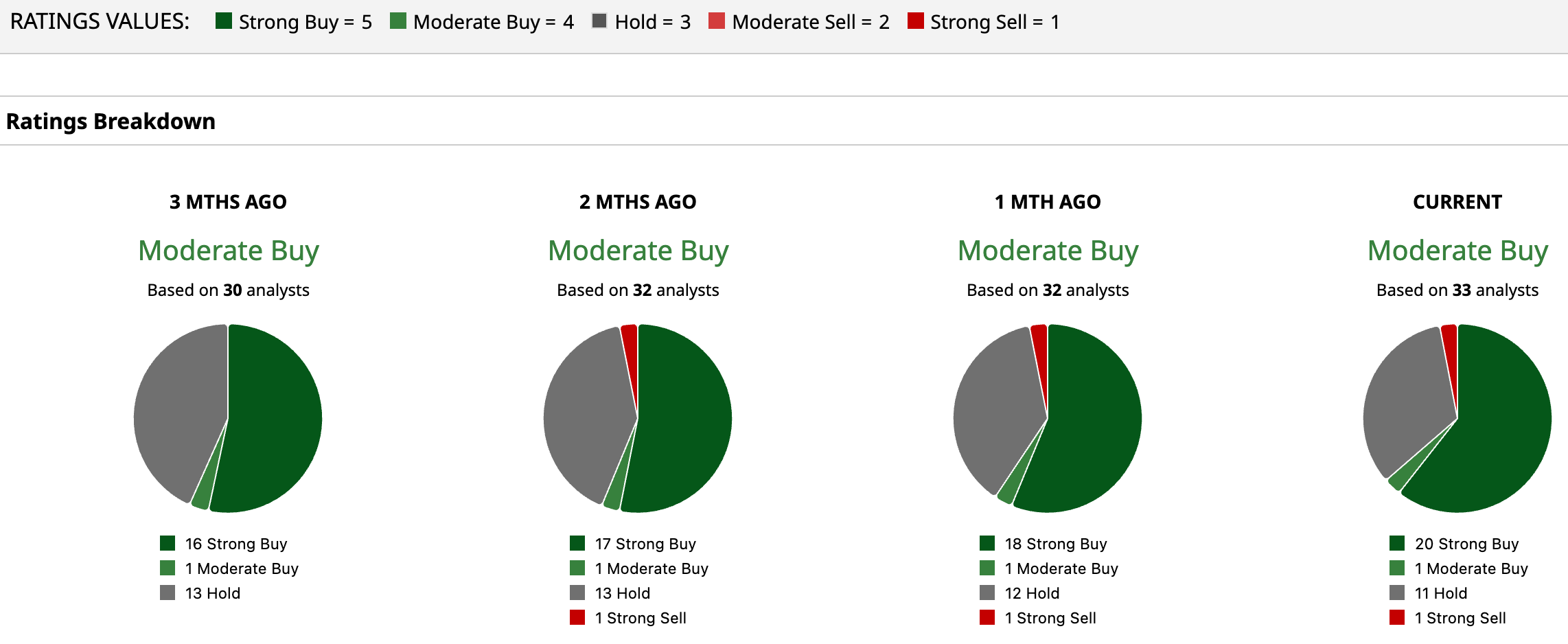

CoreWeave stock has a consensus “Moderate Buy” rating overall. Out of 33 analysts covering the stock, 20 recommend a “Strong Buy,” one gives a “Moderate Buy,” 11 analysts stay cautious with a “Hold” rating, and one advises a “Strong Sell.”

CRWV has already surged past the average analyst price target of $126.64, while the Street-high target price of $180 suggests 32% upside ahead.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.