Believes Change is Needed in the Boardroom in Order For US Foods to Fulfill Its Significant Potential and Finally Deliver For Stockholders

Visit www.makeUSFDdeliver.com for Additional Information and Resources, Including New Investor Presentation

Encourages Stockholders to Vote on the GOLD Card to Elect Sachem Head’s Five Highly Qualified Nominees

Sachem Head Capital Management LP (“Sachem Head”), a beneficial owner of approximately 8.7% of the outstanding common stock of US Foods Holding Corp. (NYSE: USFD) (“US Foods”, “USFD” or the “Company”), today sent a letter to its fellow stockholders outlining why it believes significant change is needed in the boardroom of US Foods in order for the Company to fulfill its long-term potential. In the letter, Sachem Head discusses the track record of underperformance at the Company under the current directors and management team and makes the case for why stockholders should help deliver a new culture of accountability at US Foods by voting on the GOLD proxy card to elect Sachem Head’s five director nominees to the US Foods Board of Directors (the “Board”) at the May 18, 2022, Annual Meeting of Stockholders (the “2022 Annual Meeting”).

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20220426006069/en/

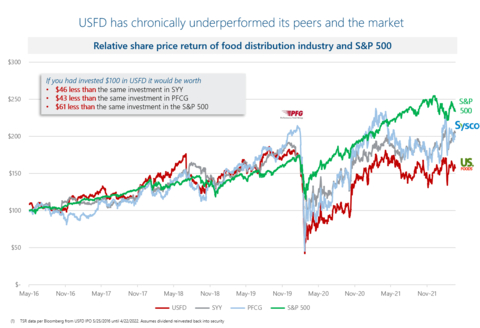

Image 1 (Graphic: Business Wire)

Sachem Head also released a new investor presentation, which is available at www.makeUSFDdeliver.com.

The full text of the letter is below:

Dear Fellow US Foods Stockholders:

We beneficially own approximately 8.7% of US Foods common stock, a roughly $750 million investment that makes us one of the Company’s largest common stockholders. We have been invested in the Company since 2018, mostly as a passive stockholder. Over that time, it has become clear to us that significant change is needed for the Company to fulfill its long-term potential. This is why we have nominated five highly qualified individuals who have the skills, experience and alignment necessary to help instill a fresh culture where management is held accountable and mediocrity is no longer the norm.

USFD has underperformed since its IPO

The Company’s underperformance relative to its peers and the broader market with respect to total stockholder return is evident over nearly every relevant time period.

Relative Cumulative Total Shareholder Return as of 4/22/2022 |

||||

Time Period |

USFD |

SYY |

PFGC |

S&P 500 |

1 Year |

(3%) |

10% |

(6%) |

5% |

3 Year |

9% |

36% |

30% |

54% |

5 Year |

39% |

93% |

117% |

98% |

Since IPO |

66% |

112% |

109% |

127% |

Note: Total shareholder return with dividends re-invested in security. Source: Bloomberg |

||||

This disappointing performance cannot be explained away by blaming COVID-19. Ever since the Company missed its guidance in July 2018, US Foods has traded at a significant discount to its closest peer Sysco Corporation (NYSE: SYY) (“Sysco”). In fact, despite highly similar business models and leverage levels on fully recovered market consensus CY2024 estimates, US Foods currently trades at ~11x earnings per share, while Sysco trades at ~17x earnings per share, which implies Sysco trades at a ~50% multiple premium to USFD. This multiple disparity has only increased post-COVID, which in our view reflects a lack of investor conviction in the Company’s ability to achieve its long-term objectives.

The Company is trying to mislead and distract stockholders by cherry-picking time spans that show a favorable 1-year total shareholder return. We think stockholders are tired of the Company trying to hide the facts. The reality of being a long-term US Foods stockholder is clear, as of Friday, April 22, 2022, over time periods spanning one year, three years, five years, and since the Company’s IPO, the Company’s total shareholder return has materially underperformed all of its peers and the market as a whole. (See Image 1).

The Company has lower margins than Sysco – and continues to lose ground

At its analyst day in 2018, US Foods emphasized its focus on improving operational execution, and as a result margins. Since then, management has repeatedly indicated that the Company has a 200-basis point margin gap versus Sysco’s domestic business and has suggested that approximately 75% of that gap can be closed over time.1 We believe management’s historical view implies an opportunity to increase adjusted EBITDA by approximately $450 million, or approximately 30%.

Since our public engagement with the Company began, management has departed from its previous frankness regarding this topic and will no longer address the margin gap with Sysco in public. To us, this suggests that the current management team lacks the operational confidence in its ability to narrow the margin gap and would prefer it if the topic simply went away.

Any incremental improvements in the Company’s margins over time have been met or exceeded by Sysco. Without a significant cultural change at the Company, there is no reason to expect that the future will be different than the past – market consensus estimates expect the margin gap to widen from calendar year 2019 to calendar year 2023.

Although we are focused on the Company’s network inefficiencies, we understand and agree that the customer experience is a vital aspect of the Company’s business and can’t be ignored. Based on customer feedback, we believe the most important drivers of customer satisfaction are receiving everything they ordered, on time, and at a reasonable price. Anecdotally, our research suggests that the Company’s supply chain issues drive weak relative fill rates and on-time deliveries for customers. We believe that better leadership on distribution efficiency will result in happier customers and enhanced profitability.

We believe that with proper oversight from a refreshed Board with the right expertise, the Company can succeed in closing a significant portion of the addressable margin gap, leading to a clear path to achieving over $4.00 in earnings per share.

Oversight failures

Ultimately, we believe that the Company’s failure to achieve its potential is the result of a Board that has not held management accountable.

Supply chain turnover

One clear area where leadership has come up short is in creating a culture that effectively balances operational and supply chain excellence and an effective sales organization. The most glaring consequence is that since its initial public offering in 2016, the Company has had four different Chief Supply Chain Officers, including a year-long period during the depths of the COVID-19 pandemic when there was no full-time supply chain executive serving in this critical role.

Based on our research, we believe that much of the turnover in the Company’s supply chain organization has been driven by management’s unwillingness to give the supply chain team the authority to implement best practices in response to pushback from the sales organization. We believe this leads to frustration within the executive ranks and explains the frequent departures in this position.

Capital allocation missteps

US Foods has been plagued by value-destructive capital allocation under its current leadership. In 2018, the Company announced the purchase of Services Group of America (“SGA”). Despite reasonable strategic logic behind the deal, the Company mismanaged the integration and divestiture process leading to what we believe was a purchase price of ~19x pre-synergy EBITDA.

The Smart Foodservice deal, announced in March 2020 and closed a month later, has been perhaps the most harmful capital allocation decision for common stockholders. When the deal was agreed, the world was already experiencing the early stages of the COVID-19 pandemic, with restaurant sales seeing large declines in Europe and early declines in the United States. A disciplined leadership team and Board would have known that it was not the right time to engage in a large-scale acquisition, much less financing the deal with uncommitted debt financing. Alongside several other large stockholders, we implored management to walk away from the deal if at all possible because we feared equity financing for the deal might be required. Less than two months after the deal was announced, the Company chose to fund a portion of the transaction in a dilutive preferred equity transaction with KKR. We believe that this dilution, which common stockholders are still paying for today, also resulted in adding a misaligned preferred stockholder to the Board that we believe could be an impediment to change.

History of missed expectations and weak relative performance exiting COVID

Management has chronically reduced and missed guidance – which we believe has destroyed the Company’s credibility with the investment community.

In March 2018, the Company released its initial guidance with respect to long-term key performance metrics. On its July 2018 earnings call only a few months later, the Company reduced its guidance and the common stock lost approximately 17% of its value, or ~$1.5bn of market cap, in a single day. Accounting for 2019 actual performance and assuming the Company had achieved its pre-pandemic 2020 guidance issued in February 2020, we believe that the Company would have underperformed its 2018 three-year EBITDA and EPS target by approximately 10% and 25%, respectively.

In order to determine relative operational execution as we exit the impact of COVID, it is important to look at calendar 2022 performance. Based on comparing calendar 2022 estimates vs. 2019 PF EBITDA, US Foods’ is expected to underperform Sysco by ~20%. It is important to understand that both of the Company’s public peers will surpass their pre-COVID performance in 2022 and are talking about the lessons learned and efficiencies put in place over the past few years. US Foods is the only company among its peers that is still looking backward instead of forward and focusing on the pandemic as the reason for weak results.

Bad-faith engagement has further demonstrated the need for change

Sachem Head has consistently sought to reach a constructive resolution with US Foods – but the Board’s unwillingness to engage with us and make serious counteroffers have led us to this point.

As the Company recently noted, it is true that we have proposed a variety of potential settlement structures in the seven months we have been engaging with them. We don’t think this is “erratic” – our numerous offers reflect our attempt to be open-minded, adapt to a dynamic situation and potentially reach a settlement that works for all parties – always with the best interests of USFD stockholders in mind. A negotiation is supposed to be built on both sides trying to find ways to reach common ground. In contrast, the US Foods Board has effectively made only one offer throughout all of our discussions, two directors on a twelve-person Board with a “multi-year” standstill. To us, this is not good-faith negotiation and demonstrates a failure to understand the frustration that stockholders have felt for some time.

We believe that the choice for stockholders is clear – a vote for Sachem Head’s nominees is a vote for a refreshed Board of Directors and a cultural reset that will benefit all of the Company’s stakeholders. A vote for the Company’s nominees will reward an entrenched Board of Directors that has tolerated years of broken promises, lackluster performance, and is more concerned with keeping new perspectives out of the boardroom than serving the stockholders.

The key question for stockholders is this: Who do you believe will make US Foods deliver?

The Board recently released a new “long-range plan” that it claims is already working based on the pre-announcement of first quarter 2022 earnings on April 21, 2022. We find it difficult to believe that a plan, which was only announced after we delivered our director nominations in mid-February – or halfway through the announced quarter – could have a material impact this soon. Tellingly, the Company did not feel comfortable raising 2022 guidance, which may signal a lack of conviction in its future results.

USFD clearly thought these results would be well received by investors, as the Company rarely preannounces earnings, but the share price reaction was muted. During the two days after the pre-announcement, the Company’s share price only increased +1% and only marginally outperformed its closest peer. We believe this reflects investor skepticism in management’s ability to achieve its public targets.

As investors assess the Company’s ability to achieve its long-term plan, it’s worth considering its recent public letter, dated April 18, 2022, where the Company admitted that “we recognize that we did not deliver on expectations we set in the past.”

In our view, we believe stockholders should ask themselves two key questions:

- Would this new plan have ever existed or seen the light of day if the Company wasn’t facing a proxy contest?

- Why should stockholders trust this Board to deliver on a new plan – which looks highly similar to its 2018 predecessor – when last time by their own admission they fell short?

If elected, our nominees will finally give stockholders a Board you can trust. Our nominees will work collaboratively with the other Board members to enhance operational efficiency, restore credibility with the investment community and reverse the deep-seated aversion to change that has been allowed to permeate the Company’s culture.

The value opportunity: improved oversight and execution can deliver 100% upside

We see an incredible opportunity for US Foods to become a great company. This starts with refreshing the Board to ensure directors with the right skill sets and who acknowledge the need for change. While ultimately these decisions will be up to the reconstituted Board as a whole, if elected our nominees would focus on:

- A cultural reset – we believe that the Company needs to give equal weight to its distribution network and its sales organization. The head of supply chain needs a seat at the table – which clearly has not been a priority based on the level of turnover at that position. This cultural shift needs to be driven throughout the Company and led from the boardroom and by the C-suite.

- Closing the margin gap – we believe that approximately 50% of the margin gap versus Sysco can be closed with minimal disruption to the business, and that there is likely additional opportunity once basic supply chain best practices have been implemented. This can be driven by focusing on areas including improving warehouse labor productivity, better network optimization and greater private label penetration. Ultimately, better execution will improve the Company’s relationships with customers and suppliers and may even enhance revenue as operations run more smoothly. Once the core operations have been fixed, the Company could look to reinvest proceeds into revenue-generating activities and integrate tuck-in M&A into an efficient organization.

- Restoring credibility with stockholders – US Foods needs to regain the trust of the investment community by setting achievable and clear targets, stopping the capital allocation missteps and communicating consistently and honestly with investors. And of course, the Company needs to execute. But if these things can be achieved, we believe the credibility deficit will shrink, as will the valuation discount versus peers.

- Reviewing management performance and setting goals for the future – our nominees would help oversee a full and fair performance review of the current management team and set challenging but achievable performance goals to ensure the status quo is not the future for US Foods.

We believe that if our nominees are elected they can help oversee the execution of this plan and the Company can realize $300 million in profit upside over consensus EBITDA estimates, leading to a clear path to achieving $4.00 or more in earnings per share in the coming years. As the Company improves execution and regains the trust of investors, we believe the stock can return to the valuation levels the Company experienced prior to its numerous missteps that began in the summer of 2018, which were close to in-line with peers. At these levels, we believe there could be 100% upside from current stock price levels.

We encourage stockholders to immediately vote on the GOLD proxy card for our nominees and to end the status quo at US Foods.

Sincerely,

Scott Ferguson

Sachem Head Capital Management LP

Biographies of Sachem Head’s Nominees

James J. Barber, Jr.

We believe Mr. Barber’s substantial supply chain expertise, honed as an executive over more than three decades, would be an extremely valuable addition to the US Foods Board. Mr. Barber is the former Chief Operating Officer of United Parcel Service, Inc. (“UPS”) (NYSE: UPS), one of the world’s largest package delivery companies. Mr. Barber began his career in 1985 as a package delivery driver for UPS in Atlanta Georgia after obtaining his Finance degree from Auburn University. He then spent 30+ years at UPS holding roles of increasing responsibility within the US, followed by relocating to Europe and becoming President of UPS Europe. Mr. Barber then relocated back to the US to become President of UPS International and join the UPS Management Committee. Mr. Barber previously served as a trustee for The UPS Foundation, on the boards of UNICEF and the Folks Center for International Business at the University of South Carolina.

Scott D. Ferguson

We believe Mr. Ferguson’s position as a significant investor in the Company and his extensive strategic, financial, entrepreneurial and corporate governance experience make him an ideal director candidate for the US Foods Board. Mr. Ferguson is the founder and managing partner of Sachem Head Capital Management LP, a value-oriented investment management firm based in New York. Prior to founding Sachem Head, he spent nine years at Pershing Square Capital Management, L.P., which he joined pre-launch as the firm’s first investment professional. Prior to Pershing Square, Mr. Ferguson served as a vice president at American Industrial Partners LLC, an operations focused private equity firm, from 1999 to 2001. Mr. Ferguson was also a business analyst at McKinsey & Company from 1996 to 1999. He currently serves on the boards of directors of Olin Corporation (NYSE: OLN), Elanco Animal Health Incorporated (NYSE: ELAN), and the Henry Street Settlement, and he is also a member of the Robin Hood Leadership Council. He previously served on the board of directors of Episcopal Charities of the Diocese of New York and is a former director of Autodesk, Inc. (NASDAQ: ADSK), a leading design & engineering software company.

Jeri B. Finard

We believe Ms. Finard’s food and consumer goods executive leadership experience as well as marketing and operational background would be a valuable asset to the Board. Ms. Finard has spent more than two decades in food and consumer goods-related executive roles. She has served as President and Chief Executive Officer, North America of Godiva Chocolatier, Inc., and in senior roles at Kraft Foods, Inc. (n/k/a Mondelēz International, Inc. (NASDAQ: MDLZ)), including as the former President of multiple multi-billion dollar divisions, and at Avon Products, Inc. (n/k/a Avon International). Her current and prior board experience includes Serta Simmons Bedding, LLC, OLLY Public Benefit Corporation, Seventh Generation, Inc., Frontier Communications Corporation (n/k/a Frontier Communications Parent, Inc. (NASDAQ: FYBR)), RevAir, HEX Performance, LLC, Raymundos Food Group, LLC and WeAre8.

John J. Harris

We believe Mr. Harris’ more than three decades of experience in operational and executive roles at the world’s largest food and beverage company would be extremely additive to the US Foods Board. Mr. Harris served in a number of senior roles at Nestlé S.A. (OTC: NSRGY), the world's largest food and beverage company, including as Chairman and Chief Executive Officer of Nestlé Waters, S.A., and Chief Executive Officer Nestlé Petcare Europe. He is a former Chairman of the board of directors of the North American Pet Food Institute. Mr. Harris joined Carnation Company in 1974 and joined Nestle in 1984 after it acquired Carnation, retiring after a 39-year career at the combined company. Mr. Harris serves on the boards of directors of the California State University, Northridge Foundation and the Advocates Pro Golf Association Tour.

David A. Toy

We believe Mr. Toy’s extensive food industry leadership experience and multi-functional corporate and financial background make him an ideal director candidate for the US Foods Board. Mr. Toy currently serves as the Chief Executive Officer of Heartisan Foods Inc., an omni-channel market leader in smoked, flavored, and kosher all-natural cheese. Previously, he served in numerous positions for Sauer Brands, Inc., a manufacturer of food products, and as Chief Financial Officer for Diversey Inc., a provider of cleaning and hygiene products. Prior to that, he held a variety of positions at The Kraft Heinz Company (NASDAQ: KHC), one of the largest food and beverage companies in the world, including as President, US Foodservice. His other experience includes corporate planning and financial roles at Lexmark International, Inc. and Eastman Chemical Company (NYSE: EMN). Mr. Toy has served as a member of the board of directors of QBD & Minus Forty Technologies Corp., a North American designer and manufacturer of refrigerated marketing solutions.

About Sachem Head Capital Management

Sachem Head is an investment manager founded in 2012 by Scott D. Ferguson. The firm employs a concentrated, value-oriented investment strategy and is primarily focused on equity investments in North America and Europe.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

The information herein contains “forward-looking statements.” Specific forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts and include, without limitation, words such as “may,” “will,” “expects,” “believes,” “anticipates,” “plans,” “estimates,” “projects,” “targets,” “forecasts,” “seeks,” “could,” “should” or the negative of such terms or other variations on such terms or comparable terminology. Similarly, statements that describe our objectives, plans or goals are forward-looking. Forward-looking statements are subject to various risks and uncertainties and assumptions. There can be no assurance that any idea or assumption herein is, or will be proven, correct. If one or more of the risks or uncertainties materialize, or if Sachem Head’s underlying assumptions prove to be incorrect, the actual results may vary materially from outcomes indicated by these statements. Accordingly, forward-looking statements should not be regarded as a representation by Sachem Head that the future plans, estimates or expectations contemplated will ever be achieved.

Certain statements and information included herein have been sourced from third parties. Sachem Head does not make any representations regarding the accuracy, completeness or timeliness of such third party statements or information. Except as may be expressly set forth herein, permission to cite such statements or information has neither been sought nor obtained from such third parties. Any such statements or information should not be viewed as an indication of support from such third parties for the views expressed herein.

1 Sysco’s domestic business includes US Foodservice Operations, SYGMA and Other divisions with a corporate overhead allocation based on percent of revenue. See our recently released presentation where we quote several instances from 2017-2021 where the Company’s management has made this statement.

View source version on businesswire.com: https://www.businesswire.com/news/home/20220426006069/en/

Contacts

Investor Contact:

Innisfree M&A Incorporated

Scott Winter / Jonathan Salzberger

(212) 750-5833

Media Contact:

Longacre Square Partners

Dan Zacchei / Joe Germani

DZacchei@longacresquare.com / JGermani@longacresquare.com