As the global financial markets navigate the opening weeks of 2026, a massive structural shift has taken hold of the commodities sector. Industrial and precious metals are currently undergoing a historic price surge, with gold, silver, and copper all testing psychological and technical ceilings that were once thought unreachable. This rally is not merely a speculative bubble; it is the culmination of years of underinvestment in mining infrastructure, an accelerated global energy transition, and a profound shift in how central banks manage their reserves in an increasingly fragmented geopolitical landscape.

For investors and industrial consumers alike, the implications are immediate and stark. The "everything rally" in metals is driving up the cost of technology, infrastructure, and green energy projects, while simultaneously offering a lucrative windfall for mining giants that have spent years streamlining their operations. As of January 20, 2026, the market is bracing for what many analysts call a "super-cycle," where supply-side constraints have finally collided with an insatiable demand for the building blocks of the future.

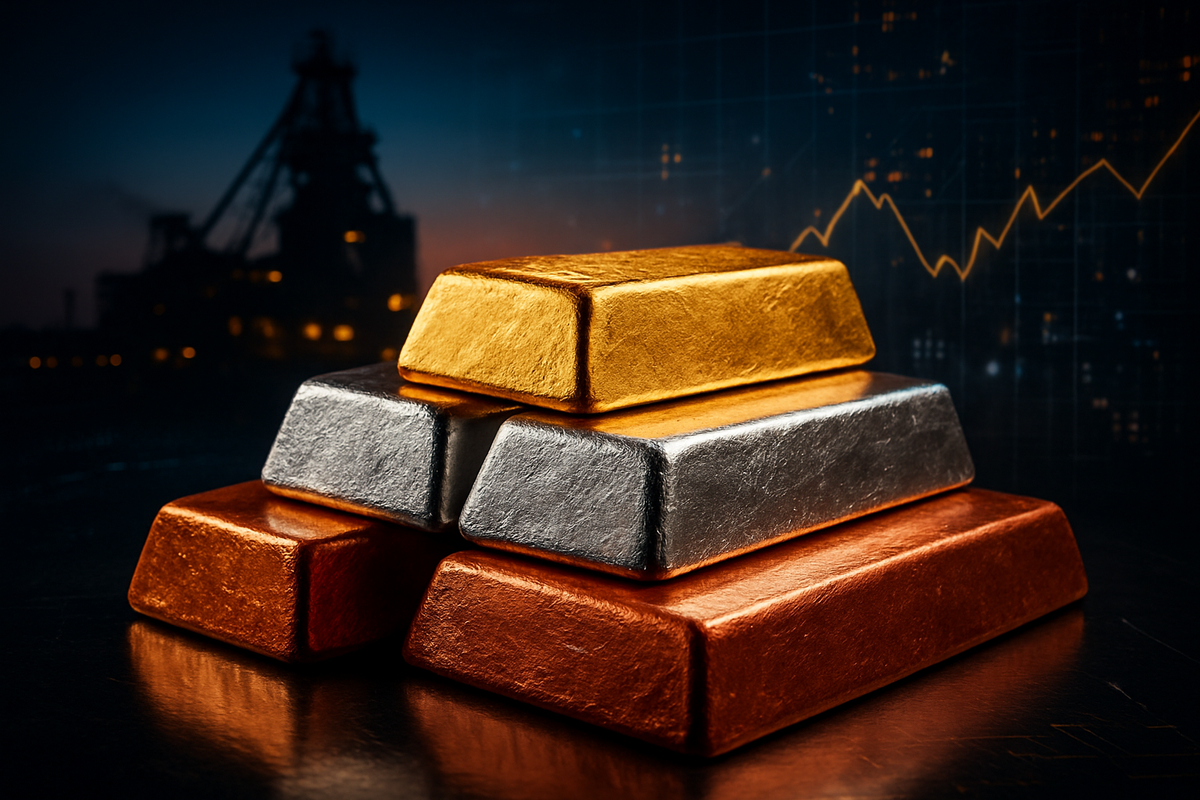

The current surge reached a fever pitch in late 2025 and has accelerated into the first weeks of 2026. Gold is currently trading near a staggering $4,734 per ounce, while silver has breached $95 per ounce, marking its highest levels in decades. Copper, the "red metal" often seen as a bellwether for global economic health, has climbed to $5.84 per pound ($13,500 per ton). This coordinated rally stems from a series of events over the past 18 months, including a significant "de-dollarization" trend where central banks in Asia and the Middle East have aggressively swapped U.S. Treasury holdings for physical gold.

Furthermore, the copper market has been rocked by a series of operational setbacks at some of the world’s largest mines. A major mudslide at the Grasberg Block Cave in Indonesia, operated by Freeport-McMoRan (NYSE: FCX), severely hampered production throughout late 2025, removing hundreds of thousands of tons of supply from the global market. Combined with continued permit delays for new projects in North America and Chile, the refined copper deficit is projected to reach as much as 330,000 tons by the end of this year. Initial market reactions have been intense, with commodities futures exchanges seeing record-high trading volumes and several "silver squeeze" events as retail and institutional buyers scramble for physical bullion.

The primary winners in this environment are the large-cap producers with high-quality assets and low operational costs. Newmont (NYSE: NEM) has seen its stock hit a new 52-week high of $118.49, as it benefits from its tier-one asset focus and the successful start-up of the Ahafo North project. Similarly, Barrick Gold (NYSE: GOLD) has leveraged its massive copper-gold joint ventures in Nevada to maintain industry-leading margins, seeing its share price climb over 200% in the last 12 months. These companies are now flush with cash, leading to increased dividends and share buyback programs that have attracted institutional value seekers.

On the industrial side, Freeport-McMoRan (NYSE: FCX) remains a critical player. While the Grasberg disruption was a temporary setback, the company is positioned for a massive earnings surge in the second half of 2026 as it returns to full production capacity just as prices are expected to peak. Southern Copper (NYSE: SCCO) and BHP Group (NYSE: BHP) are also seeing significant gains, though they face challenges in managing local labor disputes and rising ESG (Environmental, Social, and Governance) compliance costs. Conversely, companies heavily reliant on these metals as inputs—such as EV manufacturers like Tesla (NASDAQ: TSLA) and electronics firms—are facing severe margin compression as their raw material costs skyrocket.

This event fits into a broader industry trend where commodities are no longer viewed merely as cyclical trades but as strategic national assets. The expansion of AI data centers has created a massive, unforeseen demand for copper in high-capacity wiring and cooling systems, competing directly with the copper needs of the electric vehicle and renewable energy sectors. Historically, we can compare this to the commodities boom of the early 2000s, but with an added layer of regulatory complexity. Governments are now more involved than ever, with many nations moving to secure "strategic reserves" of copper and silver to protect their domestic technology industries.

The ripple effects extend beyond just mining. This surge is forcing a re-evaluation of global trade policies, particularly regarding Greenland tariffs and escalating trade tensions between the U.S. and Europe. As silver enters its fifth consecutive year of physical deficit, its dual role as an industrial metal—critical for photovoltaics and solar energy—and a monetary hedge has led to a "price-discovery" phase that is upending traditional market models. The precedent being set today suggests that the era of "cheap" industrial inputs is over, replaced by a era of resource nationalism.

In the short term, market participants should expect heightened volatility as index rebalancing in late January may lead to temporary selling in silver and gold futures. However, the long-term trajectory remains bullish. Many analysts, including those at Citi and J.P. Morgan, see gold potentially touching $5,000 and silver reaching $100 before the end of the first quarter. For mining companies, the strategic pivot will involve more aggressive exploration and faster-paced mergers and acquisitions to secure dwindling reserves.

Strategic adaptations will be required for the public. We may see more "urban mining" initiatives—recycling existing electronics for their metal content—and a shift in manufacturing toward materials that can substitute for silver or copper, though such alternatives are currently limited in efficiency. The market opportunities are vast for those who can solve the supply-side puzzle, but the challenge of bringing new mines online in an environment of strict environmental regulation remains the primary hurdle for the next decade.

The key takeaway for 2026 is that the metals market has entered a new paradigm. The combination of structural supply deficits, the technological demands of AI, and the global flight to safety has created a sustained upward pressure on prices. While the current highs may feel extreme, they reflect a world that is fundamentally short on the materials required for the 21st-century economy. Investors should maintain a close eye on central bank activities and any signs of easing in geopolitical tensions, as these will be the primary triggers for any potential cooling of the market.

Moving forward, the mining sector will likely remain the "darling" of the equity markets as long as inflation concerns and supply constraints persist. The lasting impact of this surge will be felt in the cost of everything from solar panels to smartphones, marking a definitive end to the low-inflation environment of the previous decade. For the next several months, the focus should remain on production reports from the majors and any movement in global inventories, which currently sit at dangerously low levels.

This content is intended for informational purposes only and is not financial advice