In a move that sends shockwaves through the American energy landscape, Devon Energy (NYSE: DVN) and Coterra Energy (NYSE: CTRA) announced a definitive merger agreement today, February 2, 2026. The $58 billion all-stock transaction represents one of the most significant consolidations in the history of the U.S. shale industry, effectively creating a "Super Independent" operator with a dominant footprint in the Delaware Basin. This merger aims to capitalize on massive operational scale, combining Devon’s extensive Permian operations with Coterra’s diversified portfolio across the Permian, Anadarko, and Marcellus basins.

The deal, which has an implied enterprise value of approximately $58 billion, marks the latest chapter in a relentless wave of consolidation that has reshaped the oil and gas sector over the past three years. By joining forces, the two companies are betting that size and inventory depth will be the ultimate differentiators in an era where prime drilling locations are becoming increasingly scarce. The combined entity is expected to produce over 1.6 million barrels of oil equivalent per day (boe/d), positioning it as a top-tier producer capable of rivaling the integrated majors in terms of efficiency and capital return potential.

Anatomy of a Mega-Merger: Terms and Strategy

The merger, structured as an all-stock transaction, will see Coterra shareholders receive 0.70 shares of Devon common stock for each Coterra share they hold. Upon the anticipated closing in the second quarter of 2026, Devon shareholders will own roughly 54% of the combined company, while Coterra shareholders will hold the remaining 46%. In a strategic shift, the new company will operate under the Devon Energy name and relocate its corporate headquarters to Houston, Texas—the epicenter of the global energy industry—while maintaining a substantial operational hub in Oklahoma City.

The leadership team reflects a "merger of equals" philosophy. Clay Gaspar, the current President and CEO of Devon, will serve as President and CEO of the combined firm, tasked with driving the integration of the two massive organizations. Tom Jorden, Chairman and CEO of Coterra, will transition to the role of Non-Executive Chairman of the Board. This leadership structure is designed to blend Devon’s operational prowess with Coterra’s reputation for technical excellence and capital discipline.

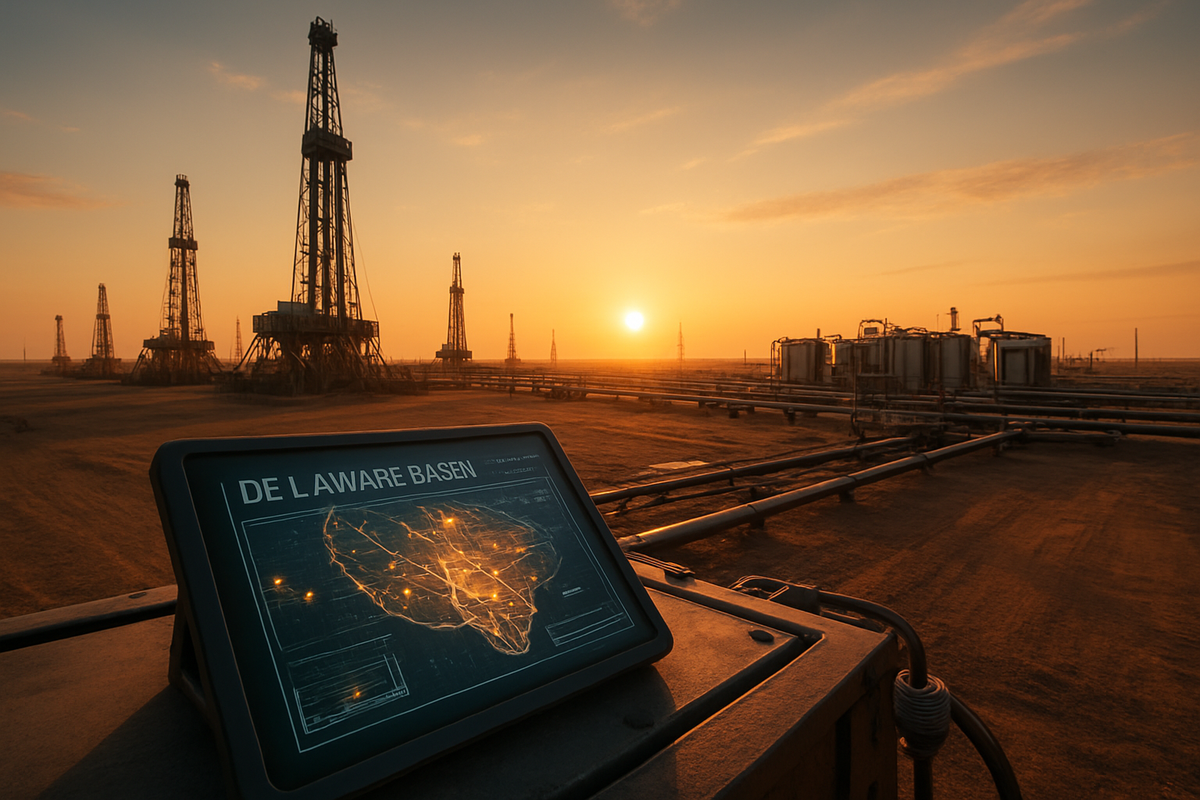

The heart of the deal lies in the Delaware Basin, a sub-basin of the Permian that remains the most prolific oil-producing region in the United States. The combined company will control nearly 750,000 net acres in the Delaware, with a pro forma production of 863,000 boe/d from that region alone. Management has already identified $1 billion in annual pre-tax synergies, which they expect to fully realize by late 2027. These savings will come from optimized drilling programs, shared infrastructure, and a unified technology platform that leverages artificial intelligence for subsurface modeling.

Winners and Losers: A Shift in Market Power

The immediate winners of this transaction are undoubtedly the shareholders of both Devon Energy and Coterra Energy. By merging, the two companies have created a more resilient cash-flow engine; Coterra’s low-cost natural gas assets in the Marcellus Shale provide a strategic hedge against oil price volatility, while Devon’s high-margin Permian oil production remains the primary growth driver. Large-cap peers like EOG Resources (NYSE: EOG) and Occidental Petroleum (NYSE: OXY) may also see a "valuation re-rating," as the market places a higher premium on companies with a decade or more of high-quality drilling inventory.

However, the merger creates a challenging environment for oilfield service giants like Halliburton (NYSE: HAL) and SLB (NYSE: SLB). As the number of major customers in the Delaware Basin shrinks, the bargaining power shifts heavily toward the producers. The new Devon Energy will be one of the top three service consumers in the basin, giving it significant leverage to negotiate lower day rates for drilling rigs and more favorable terms on high-end electric fracking fleets. Smaller, regional service providers may find themselves squeezed out entirely as the combined entity prioritizes large-scale "factory-mode" drilling projects.

Mid-cap producers such as Permian Resources (NYSE: PR) and Matador Resources (NYSE: MTDR) also face a daunting new reality. These companies are now competing for talent and remaining "Tier 1" acreage against a titan that possesses a significantly lower cost of capital. This merger likely marks the end of the "independent mid-cap" era in the Permian, as these firms may now feel compelled to find their own partners or risk becoming acquisition targets for the super-independents and majors.

The Consolidation Wave and Industry Implications

The Devon-Coterra merger is the logical conclusion of a trend that began in earnest in 2024. Following ExxonMobil (NYSE: XOM) and its acquisition of Pioneer Natural Resources, and the subsequent merger of Diamondback Energy (NASDAQ: FANG) and Endeavor Energy Resources, the industry has shifted from a "growth at all costs" mindset to one of "industrial scale and capital discipline." In 2025, the market saw a series of smaller "bolt-on" acquisitions, but the 2026 Devon-Coterra deal signals that the appetite for massive, transformative mergers has returned.

This event highlights a broader industry pivot toward the "manufacturing" phase of shale. Producers are no longer exploring for new fields; they are industrializing the ones they already own. By consolidating adjacent acreage, the new Devon can drill longer lateral wells—some exceeding 15,000 feet—which significantly lowers the per-barrel cost of production. This operational efficiency is critical as the global energy transition looms, requiring U.S. producers to be the low-cost providers in a competitive global market.

From a regulatory standpoint, the $58 billion price tag is certain to draw scrutiny from the Federal Trade Commission (FTC). While the upstream oil and gas market remains relatively fragmented compared to other sectors, the concentration of production in the Delaware Basin could raise concerns about regional infrastructure and midstream access. However, historical precedents suggest that as long as the merger does not impede consumer fuel prices, it is likely to proceed, albeit perhaps with minor asset divestitures required in overlapping areas.

The Road Ahead: Integration and Evolution

In the short term, the focus for Devon will be the seamless integration of Coterra’s technical teams and diverse asset base. The "cultural fit" between the two companies—both known for their conservative balance sheets and technical focus—is expected to be smoother than past industry mergers. However, the move of the headquarters to Houston will be a significant logistical undertaking and could lead to some talent attrition in the transition from Oklahoma City.

Looking further ahead, the market will be watching to see how the combined company utilizes its massive free cash flow. With the era of aggressive production growth largely over, investors expect the "New Devon" to lead the way in shareholder returns, likely through a combination of base-and-variable dividends and aggressive share buybacks. The company’s increased scale also makes it a more formidable player in the emerging Carbon Capture and Sequestration (CCS) market, as it now has the capital and the subsurface expertise to lead large-scale environmental initiatives.

The biggest challenge will be maintaining the quality of the drilling inventory. While the merger secures over a decade of high-quality locations, the "inventory treadmill" never stops. The combined company will eventually need to look outside the Permian or invest heavily in enhanced oil recovery (EOR) technologies to sustain its production levels into the 2030s.

Final Assessment: A Landmark Day for US Energy

The $58 billion merger of Devon and Coterra is a defining moment for the U.S. shale industry in 2026. It confirms that scale is the only remaining competitive advantage in a mature basin and sets a new benchmark for what a "Super Independent" should look like. The deal successfully marries oil-weighted growth with gas-weighted stability, creating a diversified powerhouse that is well-equipped to navigate the volatile energy markets of the late 2020s.

For investors, the key takeaway is the continued "bifurcation" of the energy sector. The gap between the large-cap, diversified giants and the smaller, single-basin players is widening. Those who hold the best rocks and the most scale will continue to attract the lion's share of institutional capital. In the coming months, the market will closely monitor the regulatory approval process and any signs of further consolidation among the remaining mid-cap players in the Permian.

As the industry gathers its breath following this massive announcement, one thing is clear: the U.S. shale patch is now a land of giants, and the Devon-Coterra merger has just created one of its most powerful residents.

This content is intended for informational purposes only and is not financial advice