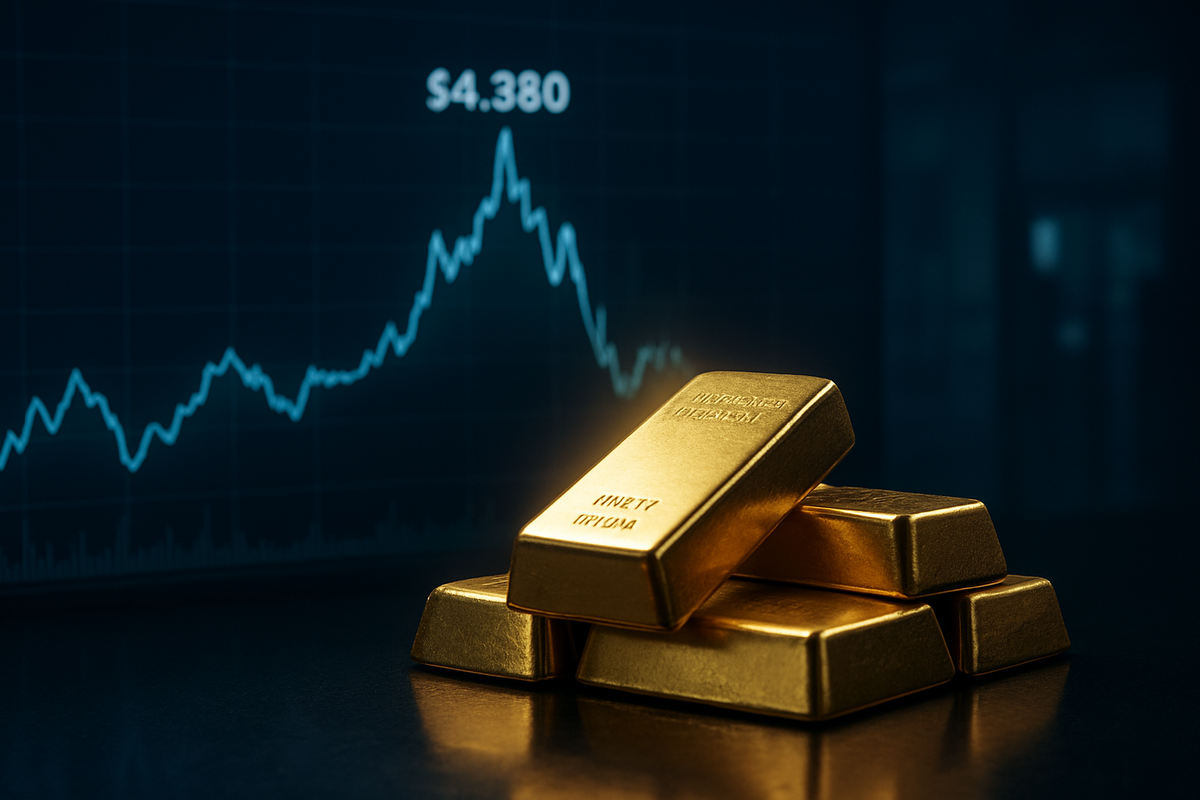

The global gold market has entered a period of unprecedented turbulence, punctuated by a historic climb to an all-time high of $4,380 per ounce earlier this year. This milestone, which shattered previous resistance levels, was driven by a perfect storm of geopolitical instability, aggressive central bank accumulation, and a shifting macroeconomic landscape. However, the celebration was short-lived as the precious metal faced a sharp correction in March 2026, pulling back as investors grappled with a surging U.S. dollar and a sudden shift in liquidity needs.

The recent volatility highlights a fascinating paradox in modern finance: while gold prices have reached nominal records, domestic ownership through Western financial instruments remains remarkably low. This "participation gap" suggests that while the price action is being driven by global institutional forces and sovereign actors, the average American investor is only just beginning to wake up to the potential of the yellow metal as a core portfolio stabilizer.

The Path to $4,380: A Geopolitical Supercycle

The journey to the $4,380 mark was paved by a series of escalating global tensions that solidified gold’s status as the ultimate safe haven. Throughout late 2025 and into the first quarter of 2026, intensified conflicts in the Middle East and ongoing friction in Eastern Europe created a "geopolitical risk premium" that analysts say has become a permanent feature of the market. This environment was further complicated by the nomination of a new, more hawkish leadership at the Federal Reserve, which initially introduced a wave of uncertainty regarding the future of interest rates and the stability of the dollar.

By late January 2026, gold surged past the $4,000 threshold, fueled by a massive "flight to quality" as equity markets experienced a mid-winter wobble. The momentum reached its zenith in mid-February when spot gold touched $4,380. However, as the U.S. dollar hit its strongest weekly gain in years during early March, the "liquidity-driven" correction began. Investors, facing margin calls in other asset classes and a sudden premium on cash, began to liquidate profitable gold positions. This triggered a retreat toward the $4,100 level, marking one of the most volatile months in the history of the London Bullion Market.

Mining Giants and the Profitability Trap

The record-breaking price action has had a profound impact on the major players in the gold mining sector. Newmont Corporation (NYSE: NEM), the world’s largest gold miner, reported record-breaking free cash flow in its most recent quarterly filings, benefiting from a realized gold price that averaged well above $4,000. Similarly, Barrick Gold Corporation (NYSE: GOLD) saw its stock price climb significantly during the rally, as the company moved forward with plans to spin off its North American assets into a separate entity to unlock shareholder value.

However, the "winners" in this scenario face a double-edged sword. While revenue is at an all-time high, so are the costs of extraction. Agnico Eagle Mines Limited (NYSE: AEM) has cautioned investors about rising All-In Sustaining Costs (AISC), which have climbed due to inflationary pressures on labor, energy, and equipment. For many miners, the high price of gold is a necessary buffer against an increasingly expensive operational environment. If the correction deepens, the thinner margins of high-cost producers could lead to a swift reversal in stock performance, despite the historically high price of the underlying commodity.

The Paradox of Ownership: ETFs and the Safe Haven Demand

Perhaps the most significant aspect of the current gold market is the remarkably low ownership rate among U.S. retail and institutional investors. Despite the record price of $4,380, gold-backed exchange-traded funds like SPDR Gold Shares (NYSE Arca: GLD) and iShares Gold Trust (NYSE Arca: IAU) still represent less than 1% of total global financial assets. Historically, during periods of extreme inflation or geopolitical risk, this figure has been closer to 3% or 5%.

This low participation rate suggests that the recent rally was driven more by "Eastern" demand—specifically central banks in nations like Poland, China, and Kazakhstan—than by "Western" retail investors. The "de-dollarization" trend has seen sovereign entities move away from U.S. Treasuries in favor of physical bullion, creating a high floor for prices that is independent of Wall Street sentiment. The current correction is seen by some analysts as a "healthy consolidation" that may finally entice U.S. investors to re-enter the market through ETFs, as the realization sets in that the $4,000 floor may be the new permanent reality.

Looking Ahead: Consolidation or Collapse?

In the short term, the market is expected to remain in a period of high-floor consolidation. Most technical analysts see the $4,000 to $4,100 range as a critical support level that must hold to maintain the long-term bullish narrative. If the U.S. dollar continues its aggressive climb, a temporary dip below $4,000 cannot be ruled out, though safe-haven demand is expected to trigger "buy-the-dip" behavior from central banks and institutional opportunists.

Long-term, the outlook remains skewed to the upside. With global debt levels reaching staggering new heights and fiscal instability becoming a recurring theme in major economies, the strategic pivot toward hard assets appears to be in its early stages. Many investment banks are already revising their year-end 2026 targets, with some suggesting that a return to $4,380 is not just possible, but a stepping stone toward $5,000 if the "participation gap" in Western ETFs begins to close.

Conclusion: A New Era for the Yellow Metal

The ride to $4,380 and the subsequent correction serve as a stark reminder of gold's enduring role as a barometer for global anxiety. The key takeaway for the market is that the drivers of this rally are structural rather than speculative. Between central bank de-dollarization and the persistent geopolitical supercycle, the fundamentals supporting gold are stronger than they have been in decades.

Moving forward, investors should keep a close eye on gold ETF flows in the U.S. and the upcoming guidance from mining majors like Newmont and Barrick. If retail participation begins to catch up with institutional demand, the "record" price of $4,380 may soon look like a bargain. For now, the market is catching its breath, but the underlying forces suggest the golden era is far from over.

This content is intended for informational purposes only and is not financial advice.