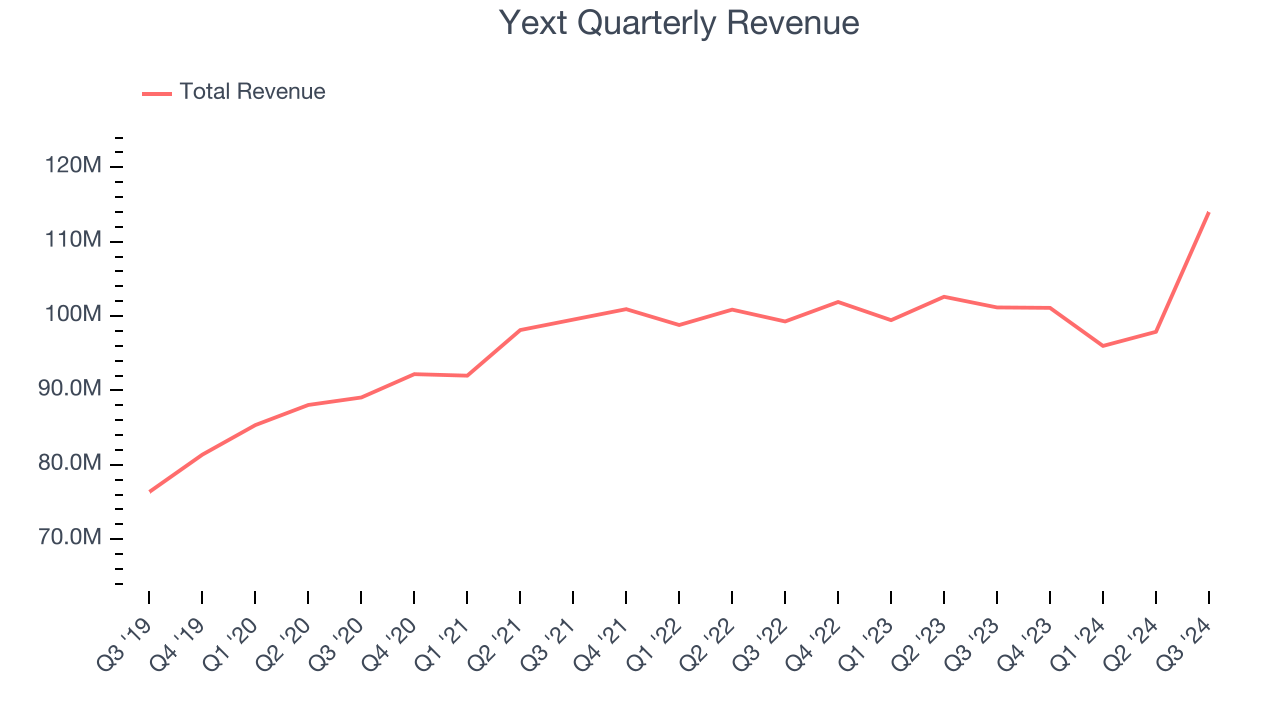

Online reputation and search platform Yext (NYSE: YEXT) beat Wall Street’s revenue expectations in Q3 CY2024, with sales up 12.7% year on year to $114 million. The company expects the full year’s revenue to be around $420.6 million, close to analysts’ estimates. Its non-GAAP profit of $0.12 per share was in line with analysts’ consensus estimates.

Is now the time to buy Yext? Find out by accessing our full research report, it’s free.

Yext (YEXT) Q3 CY2024 Highlights:

- Revenue: $114 million vs analyst estimates of $113.2 million (12.7% year-on-year growth, 0.7% beat)

- Adjusted EPS: $0.12 vs analyst estimates of $0.12 (in line)

- Adjusted EBITDA: $23.09 million vs analyst estimates of $21.65 million (20.3% margin, 6.7% beat)

- The company slightly lifted its revenue guidance for the full year to $420.6 million at the midpoint from $420.5 million

- EBITDA guidance for the full year is $67.25 million at the midpoint, above analyst estimates of $66.12 million

- Operating Margin: -9.1%, down from -1.8% in the same quarter last year

- Free Cash Flow was -$16.37 million compared to -$11.19 million in the previous quarter

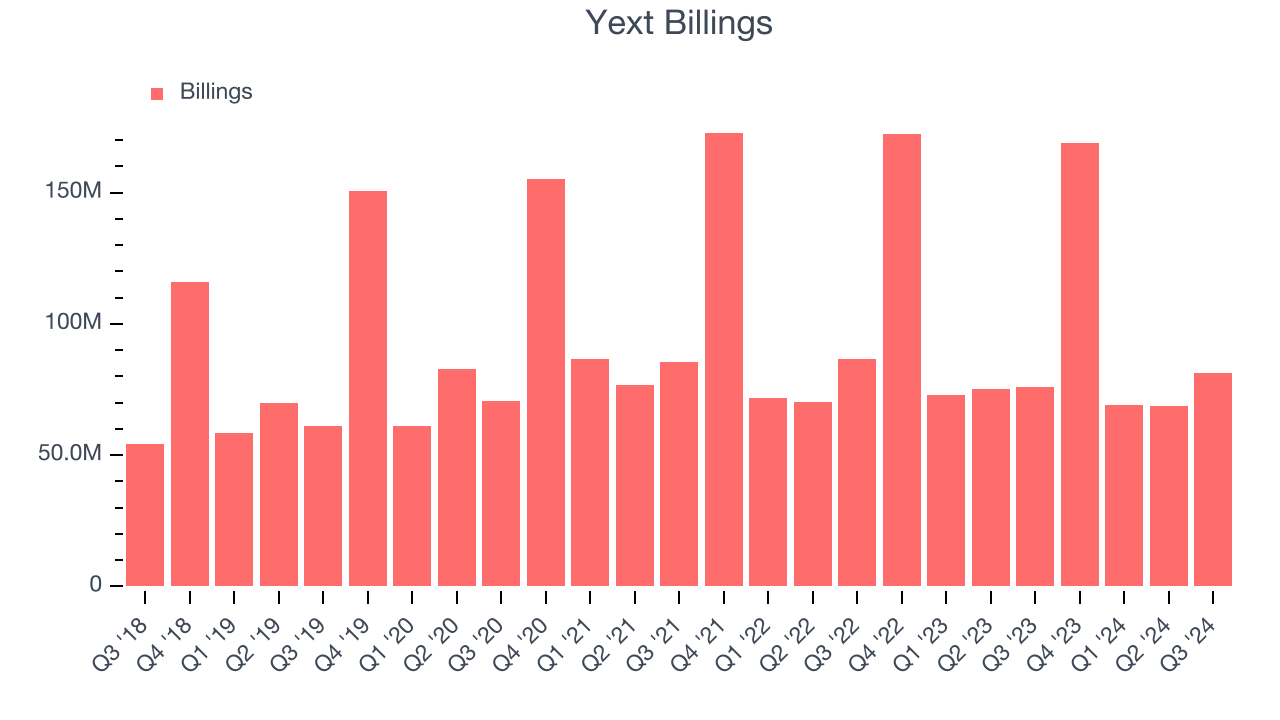

- Billings: $81.24 million at quarter end, up 6.7% year on year

- Market Capitalization: $1.09 billion

“Our fiscal third quarter results demonstrate our continued ability to drive operating efficiencies, make significant margin improvements and generate bottom-line growth,” said Mike Walrath, Yext Chairman and CEO.

Company Overview

Founded in 2006 by Howard Lerman, Yext (NYSE: YEXT) offers software as a service that helps their clients manage and monitor their online listings and customer reviews across all relevant databases, from Google Maps to Alexa or Siri.

Listing Management Software

As the number of places that keep business listings (such as addresses, opening hours and contact details) increases, the task of keeping all listings up-to-date becomes more difficult and that drives demand for centralized solutions that update all touchpoints.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Yext’s 2.3% annualized revenue growth over the last three years was weak. This fell short of our benchmarks and is a poor baseline for our analysis.

This quarter, Yext reported year-on-year revenue growth of 12.7%, and its $114 million of revenue exceeded Wall Street’s estimates by 0.7%.

Looking ahead, sell-side analysts expect revenue to grow 12.2% over the next 12 months, an acceleration versus the last three years. This projection is above the sector average and suggests its newer products and services will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Yext’s billings came in at $81.24 million in Q3, and it averaged 2.2% year-on-year declines over the last four quarters. This alternate topline metric underperformed its total sales, meaning the company recognizes revenue faster than it collects cash - a headwind for its liquidity that could also signal a slowdown in future revenue growth.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Yext’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Yext’s products and its peers.

Key Takeaways from Yext’s Q3 Results

We were impressed by how significantly Yext blew past analysts’ billings expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. However, it seems that the company did not raise full year guidance in line with the beats. This implies that the company's expectations for Q4 are below Wall Street's estimates. Zooming out, we think this was a good quarter with some questions about guidance mechanics. The areas below expectations seem to be driving the move, and shares traded down 10.7% to $7.60 immediately after reporting.

Is Yext an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.