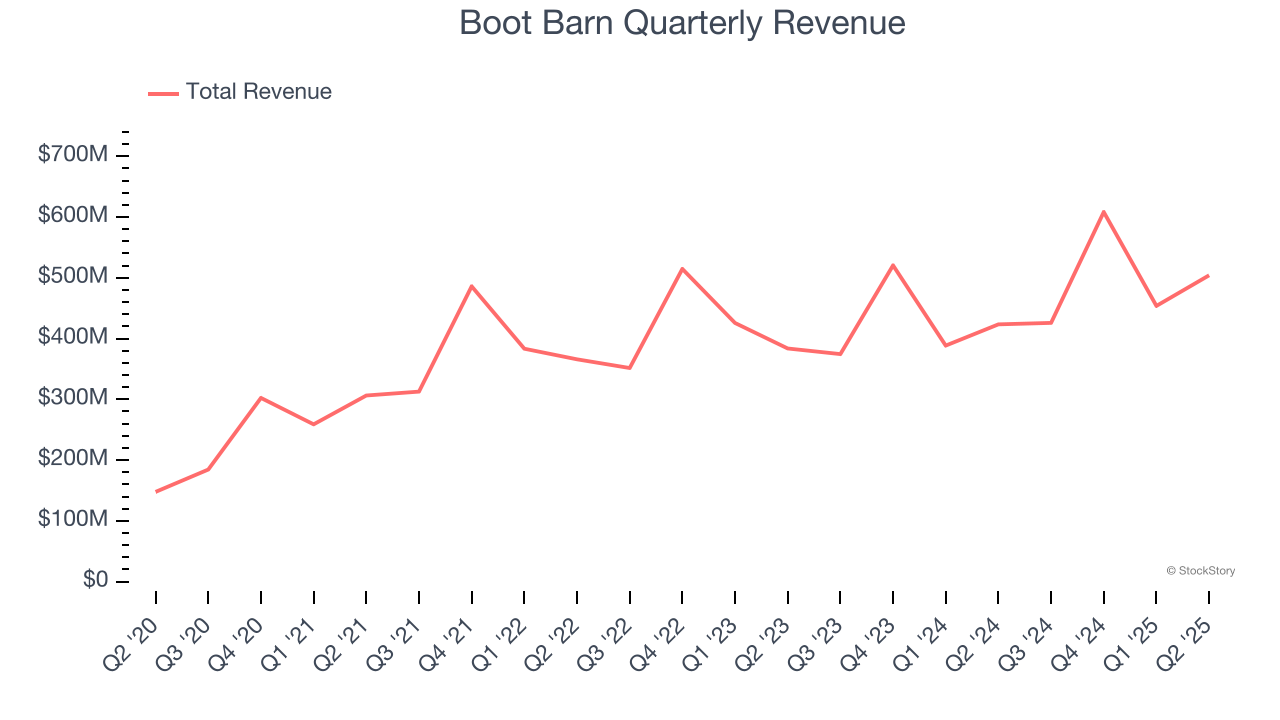

Clothing and footwear retailer Boot Barn (NYSE: BOOT) reported Q2 CY2025 results topping the market’s revenue expectations, with sales up 19.1% year on year to $504.1 million. Guidance for next quarter’s revenue was better than expected at $491 million at the midpoint, 1.8% above analysts’ estimates. Its GAAP profit of $1.74 per share was 13.3% above analysts’ consensus estimates.

Is now the time to buy Boot Barn? Find out by accessing our full research report, it’s free.

Boot Barn (BOOT) Q2 CY2025 Highlights:

- Revenue: $504.1 million vs analyst estimates of $496.4 million (19.1% year-on-year growth, 1.5% beat)

- EPS (GAAP): $1.74 vs analyst estimates of $1.54 (13.3% beat)

- Adjusted EBITDA: $88.24 million vs analyst estimates of $84.42 million (17.5% margin, 4.5% beat)

- The company lifted its revenue guidance for the full year to $2.14 billion at the midpoint from $2.11 billion, a 1.4% increase

- EPS (GAAP) guidance for the full year is $6.25 at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 14%, up from 11.9% in the same quarter last year

- Free Cash Flow Margin: 8.4%, up from 3.4% in the same quarter last year

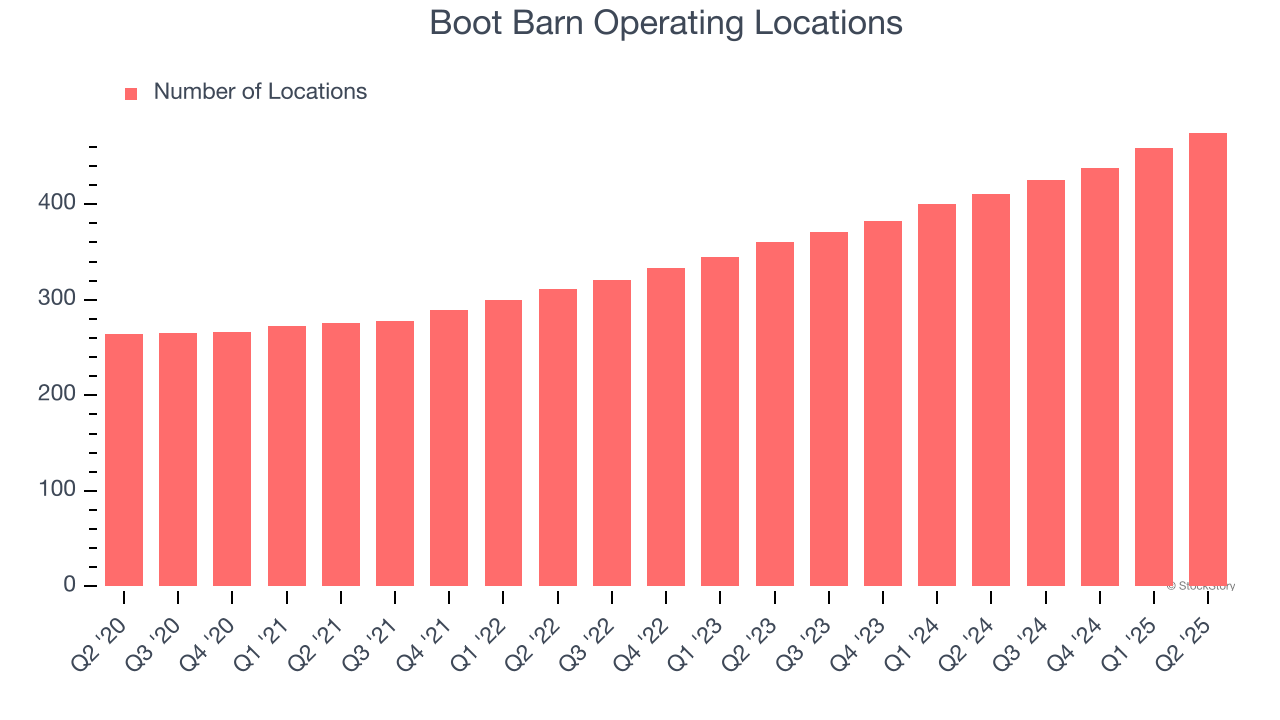

- Locations: 475 at quarter end, up from 411 in the same quarter last year

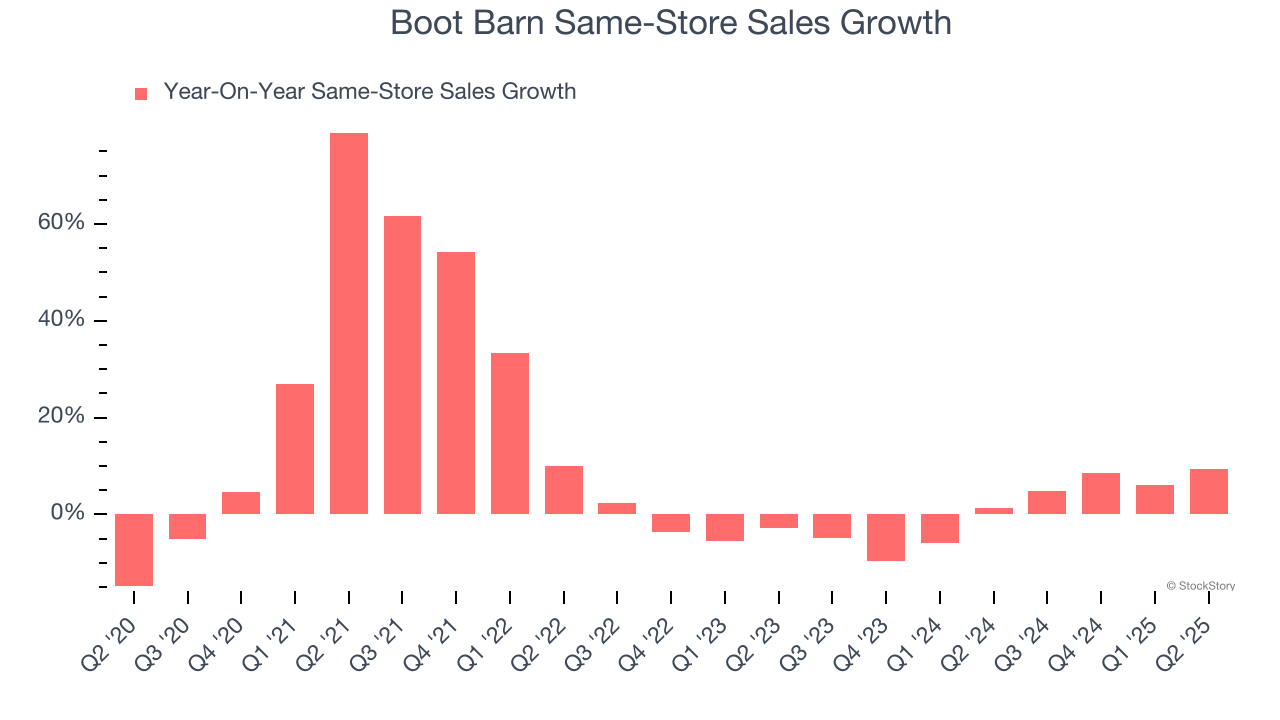

- Same-Store Sales rose 9.4% year on year (1.4% in the same quarter last year)

- Market Capitalization: $5.26 billion

John Hazen, Chief Executive Officer, commented, “We are pleased with our strong start to fiscal 2026, highlighted by high-single digit consolidated same-store sales growth and successful new store openings, which drove 19% overall revenue growth. Demand was broad-based, with strength across all major merchandise categories and geographies. At the same time, we improved gross profit 210 basis points, led by robust merchandise margin expansion which, along with solid expense control, fueled a 38% increase in earnings per diluted share. As a result of our better than expected first quarter performance and the continued strength we have seen as we moved into our second quarter, we are raising our full-year outlook while maintaining our prior guidance for the second half of the year. With our four strategic initiatives delivering consistent results and the opportunity we have to double our store count, we remain confident in our ability to continue generating value for our shareholders over the long term.”

Company Overview

With a strong store presence in Texas, California, Florida, and Oklahoma, Boot Barn (NYSE: BOOT) is a western-inspired apparel and footwear retailer.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $1.99 billion in revenue over the past 12 months, Boot Barn is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers. On the bright side, it can grow faster because it has more white space to build new stores.

As you can see below, Boot Barn’s sales grew at an impressive 16.4% compounded annual growth rate over the last six years (we compare to 2019 to normalize for COVID-19 impacts) as it opened new stores and increased sales at existing, established locations.

This quarter, Boot Barn reported year-on-year revenue growth of 19.1%, and its $504.1 million of revenue exceeded Wall Street’s estimates by 1.5%. Company management is currently guiding for a 15.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.8% over the next 12 months, a deceleration versus the last six years. Despite the slowdown, this projection is commendable and suggests the market is forecasting success for its products.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Store Performance

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Boot Barn operated 475 locations in the latest quarter. It has opened new stores at a rapid clip over the last two years, averaging 15% annual growth, much faster than the broader consumer retail sector. This gives it a chance to scale into a mid-sized business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Boot Barn’s demand within its existing locations has been relatively stable over the last two years but was below most retailers. On average, the company’s same-store sales have grown by 1.2% per year. This performance suggests it should consider improving its foot traffic and efficiency before expanding its store base.

In the latest quarter, Boot Barn’s same-store sales rose 9.4% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from Boot Barn’s Q2 Results

It was great to see Boot Barn lift its full-year revenue guidance. We were also glad its revenue, EPS, and EBITDA outperformed Wall Street’s estimates. Overall, we think this was a good quarter with some key metrics above expectations. The stock traded up 8.9% to $187 immediately following the results.

Boot Barn had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.