Since August 2025, Karat Packaging has been in a holding pattern, posting a small return of 3% while floating around $25.75.

Is now the time to buy Karat Packaging, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Karat Packaging Not Exciting?

We're swiping left on Karat Packaging for now. Here are three reasons there are better opportunities than KRT and a stock we'd rather own.

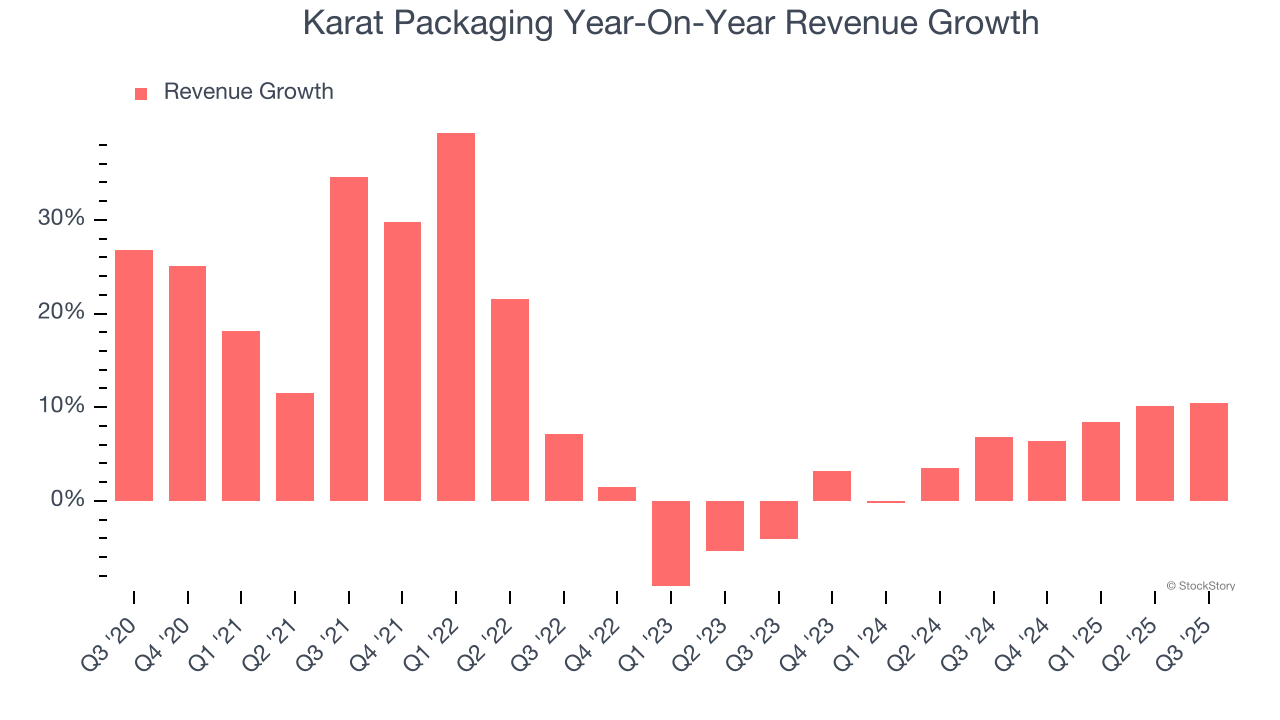

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Karat Packaging’s recent performance shows its demand has slowed as its annualized revenue growth of 6.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

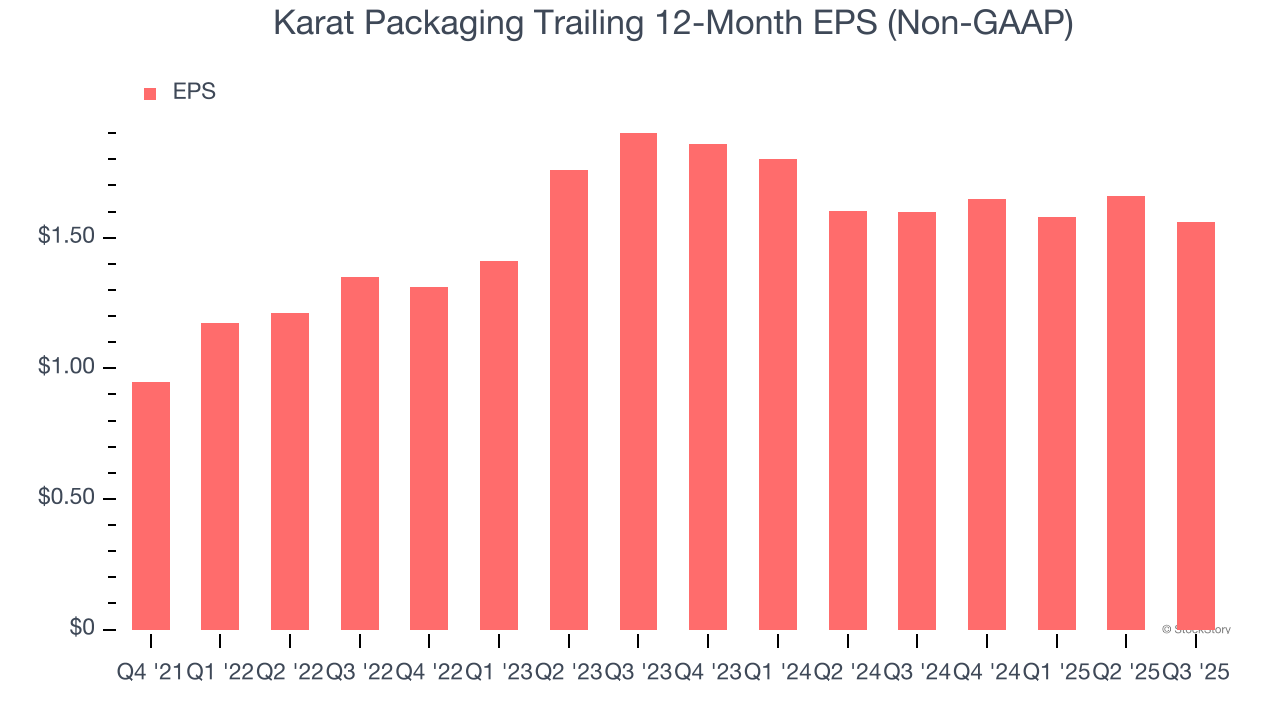

2. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Karat Packaging, its EPS declined by 9.4% annually over the last two years while its revenue grew by 6.1%. This tells us the company became less profitable on a per-share basis as it expanded.

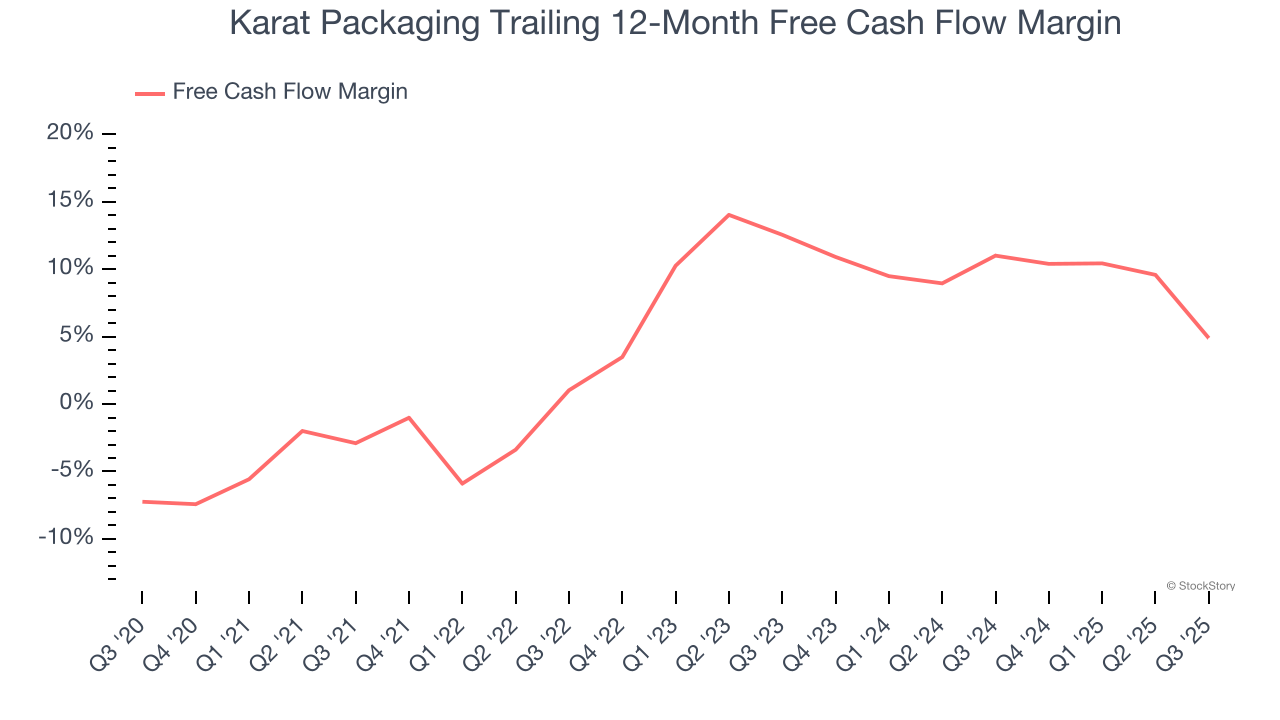

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Karat Packaging has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 5.5%, subpar for an industrials business.

Final Judgment

Karat Packaging isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 16.7× forward P/E (or $25.75 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Karat Packaging

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.