Earnings results often indicate what direction a company will take in the months ahead. With Q4 behind us, let’s have a look at Illumina (NASDAQ: ILMN) and its peers.

The life sciences tools and services sector supports biotech and pharmaceutical R&D and commercialization by providing lab equipment, data analytics, and clinical trial services. These companies benefit from recurring revenue and high margins on specialized products. Looking ahead, the sector is supported by tailwinds like advancements in genomics, personalized medicine, and the use of AI in drug discovery. However, the persistent challenge is dependence on the R&D budgets of large pharmaceutical companies and the volatility of smaller biotech firms. Future headwinds include uncertain research funding and pricing pressures from cost-conscious customers.

The 21 life sciences tools & services stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 1.7% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 16% since the latest earnings results.

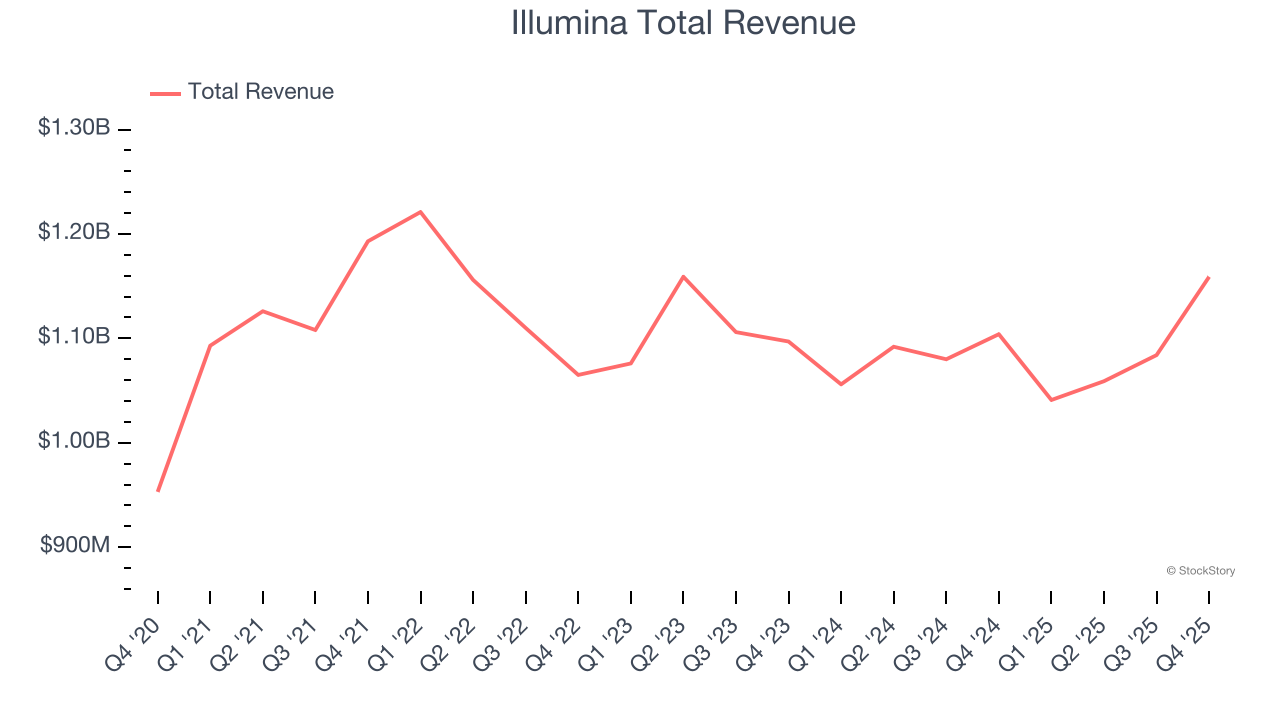

Best Q4: Illumina (NASDAQ: ILMN)

Pioneering the ability to read the human genome at unprecedented speed and affordability, Illumina (NASDAQ: ILMN) develops and sells advanced DNA sequencing and microarray technologies that allow researchers and clinicians to analyze genetic variations and functions.

Illumina reported revenues of $1.16 billion, up 5% year on year. This print exceeded analysts’ expectations by 3.2%. Overall, it was an exceptional quarter for the company with full-year revenue guidance exceeding analysts’ expectations and a solid beat of analysts’ organic revenue estimates.

"The Illumina team delivered a strong finish to 2025, marking a return to growth through disciplined execution against our strategy," said Jacob Thaysen, Chief Executive Officer of Illumina.

Illumina pulled off the highest full-year guidance raise of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 9.6% since reporting and currently trades at $120.75.

Is now the time to buy Illumina? Access our full analysis of the earnings results here, it’s free.

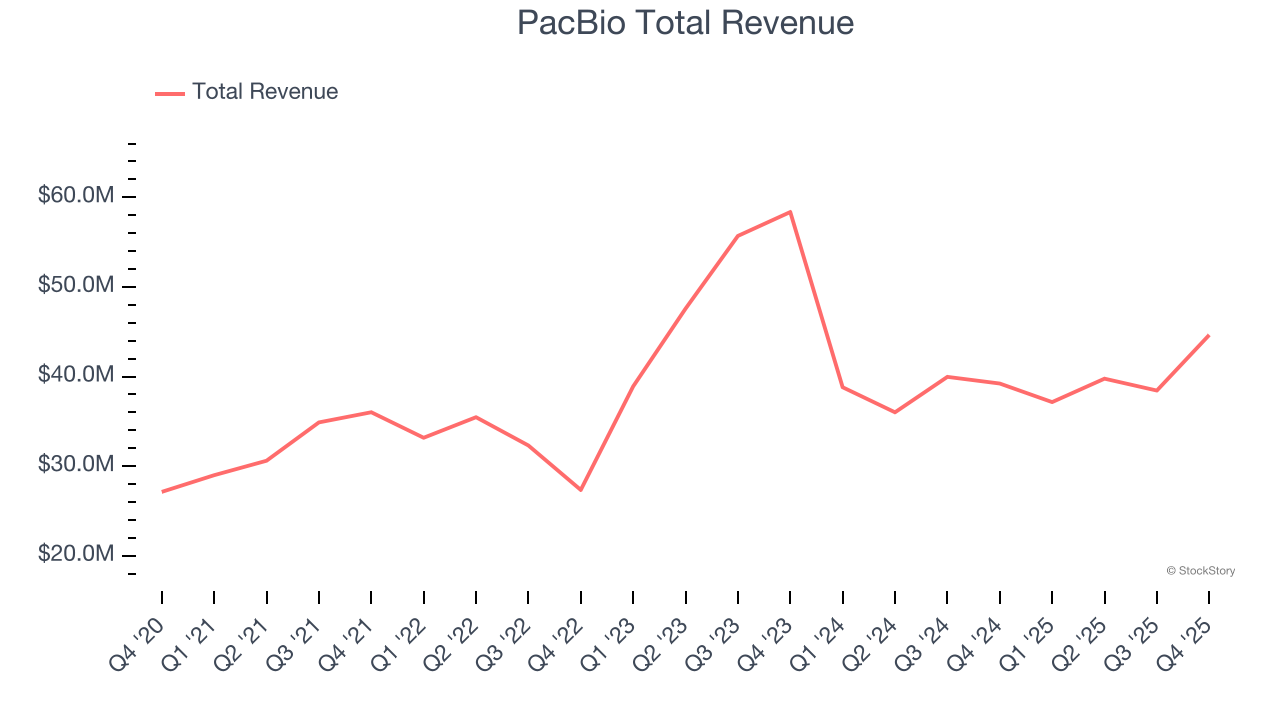

PacBio (NASDAQ: PACB)

Pioneering what scientists call "HiFi long-read sequencing," recognized as Nature Methods' method of the year for 2022, Pacific Biosciences (NASDAQ: PACB) develops advanced DNA sequencing systems that enable scientists and researchers to analyze genomes with unprecedented accuracy and completeness.

PacBio reported revenues of $44.65 million, up 13.8% year on year, outperforming analysts’ expectations by 3.7%. The business had an exceptional quarter with a solid beat of analysts’ revenue estimates and a beat of analysts’ EPS estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 25% since reporting. It currently trades at $1.38.

Is now the time to buy PacBio? Access our full analysis of the earnings results here, it’s free.

Slowest Q4: Fortrea (NASDAQ: FTRE)

Spun off from Labcorp in 2023 to focus exclusively on clinical research services, Fortrea (NASDAQ: FTRE) is a contract research organization that helps pharmaceutical, biotech, and medical device companies develop and bring their products to market through clinical trials and support services.

Fortrea reported revenues of $660.5 million, down 5.2% year on year, falling short of analysts’ expectations by 0.9%. It was a softer quarter as it posted full-year revenue guidance missing analysts’ expectations significantly and a significant miss of analysts’ EPS estimates.

Fortrea delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 6.2% since the results and currently trades at $9.70.

Read our full analysis of Fortrea’s results here.

Agilent (NYSE: A)

Originally spun off from Hewlett-Packard in 1999 as its measurement and analytical division, Agilent Technologies (NYSE: A) provides analytical instruments, software, services, and consumables for laboratory workflows in life sciences, diagnostics, and applied chemical markets.

Agilent reported revenues of $1.80 billion, up 7% year on year. This result was in line with analysts’ expectations. More broadly, it was a mixed quarter as it also produced revenue guidance for next quarter beating analysts’ expectations but revenue in line with analysts’ estimates.

The stock is down 9.4% since reporting and currently trades at $113.00.

Read our full, actionable report on Agilent here, it’s free.

10x Genomics (NASDAQ: TXG)

Founded in 2012 by scientists seeking to overcome limitations in traditional biological research methods, 10x Genomics (NASDAQ: TXG) develops instruments, consumables, and software that enable researchers to analyze biological systems at single-cell resolution and spatial context.

10x Genomics reported revenues of $166 million, flat year on year. This number beat analysts’ expectations by 4.3%. Overall, it was a very strong quarter as it also put up a beat of analysts’ EPS estimates and an impressive beat of analysts’ revenue estimates.

10x Genomics achieved the biggest analyst estimates beat among its peers. The stock is up 2.8% since reporting and currently trades at $18.00.

Read our full, actionable report on 10x Genomics here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.