Walker & Dunlop’s stock price has taken a beating over the past six months, shedding 45.9% of its value and falling to $44.96 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Walker & Dunlop, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Walker & Dunlop Will Underperform?

Even with the cheaper entry price, we're swiping left on Walker & Dunlop for now. Here are three reasons there are better opportunities than WD and a stock we'd rather own.

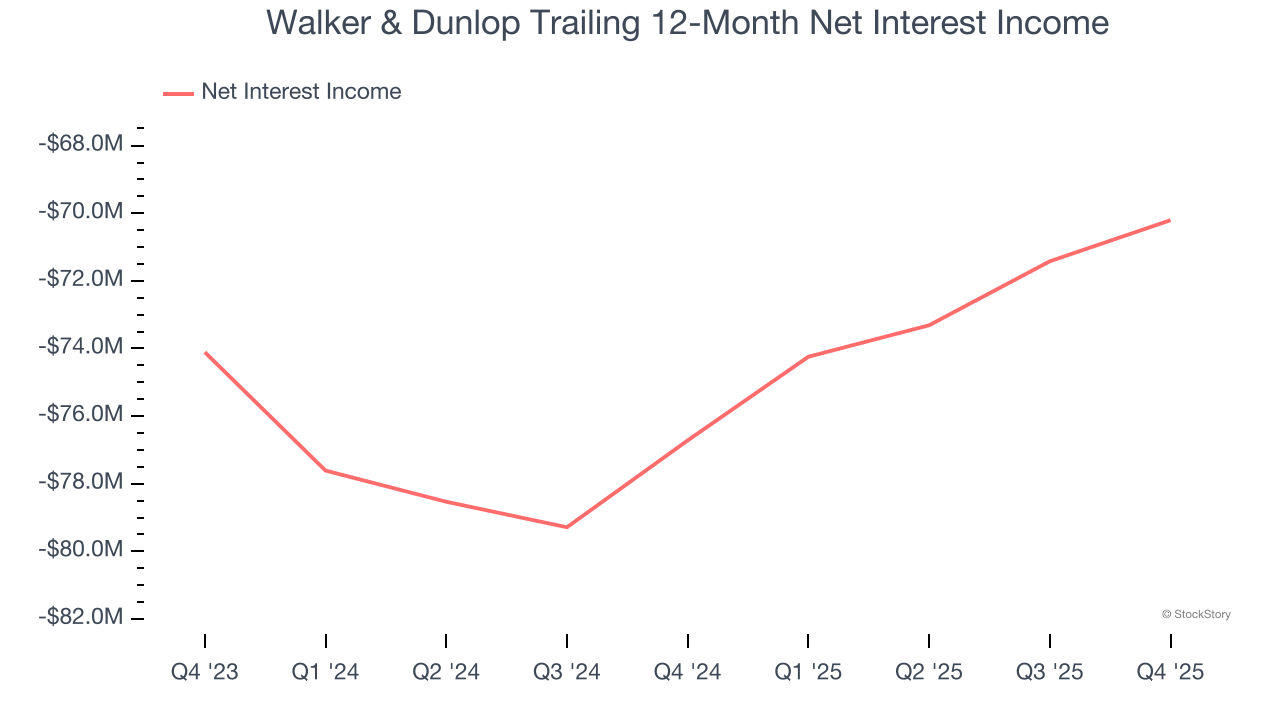

1. Declining Net Interest Income Reflects Weakness

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Walker & Dunlop’s net interest income has declined by 40.1% annually over the last five years, much worse than the broader banking industry. This shows that lending underperformed its other business lines.

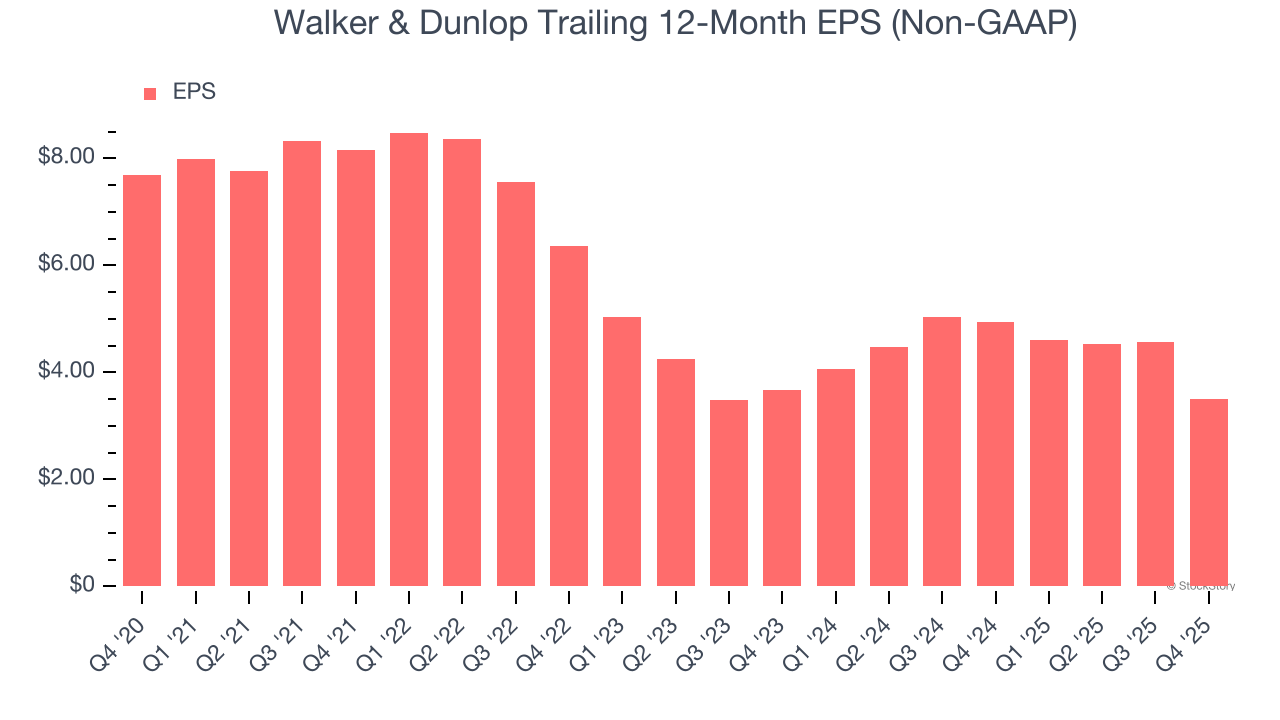

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Walker & Dunlop, its EPS declined by 14.6% annually over the last five years while its revenue grew by 2.6%. This tells us the company became less profitable on a per-share basis as it expanded.

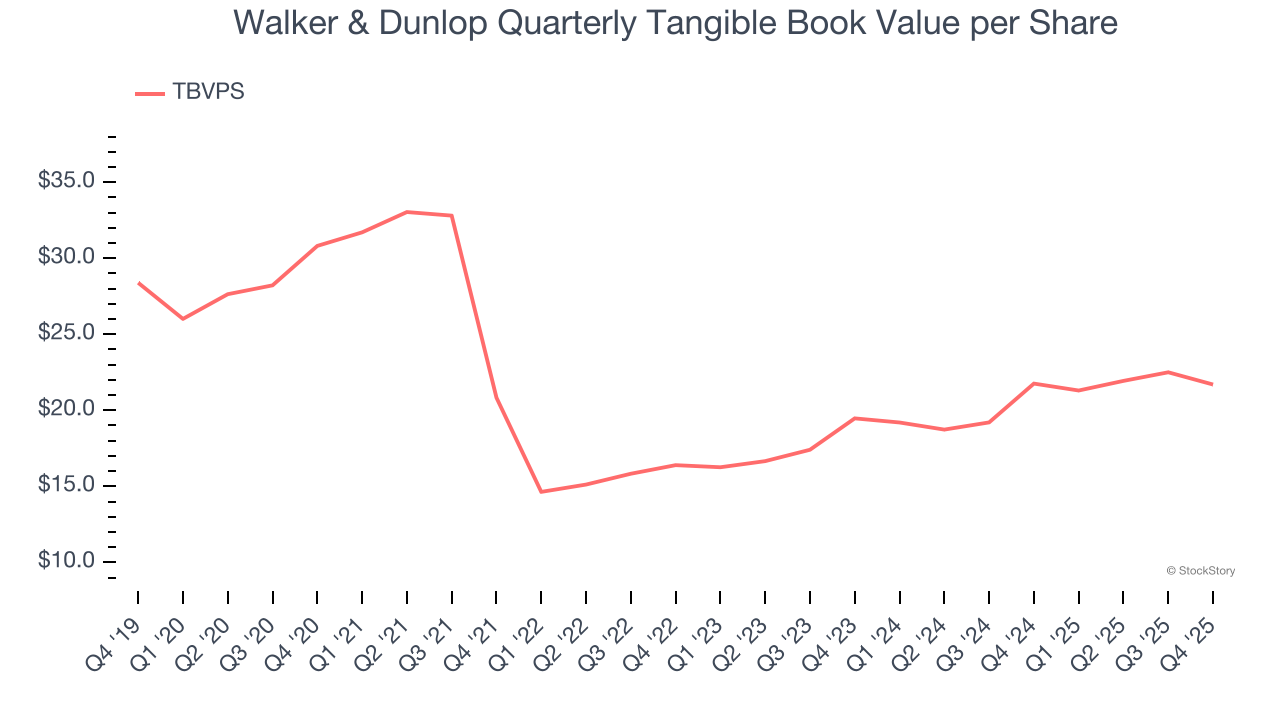

3. Substandard TBVPS Growth Indicates Limited Asset Expansion

For banks, tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

To the detriment of investors, Walker & Dunlop’s TBVPS grew at a sluggish 5.6% annual clip over the last two years.

Final Judgment

We see the value of companies driving economic growth, but in the case of Walker & Dunlop, we’re out. After the recent drawdown, the stock trades at 0.9× forward P/B (or $44.96 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are better stocks to buy right now. We’d recommend looking at one of our top software and edge computing picks.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.