The past six months have been a windfall for Amalgamated Financial’s shareholders. The company’s stock price has jumped 46.6%, hitting $39.09 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Following the strength, is AMAL a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Does Amalgamated Financial Spark Debate?

Founded in 1923 by labor unions seeking a financial institution aligned with worker values, Amalgamated Financial (NASDAQGM:AMAL) operates a values-oriented bank that provides commercial banking, trust services, and investment management to socially responsible organizations and individuals.

Two Positive Attributes:

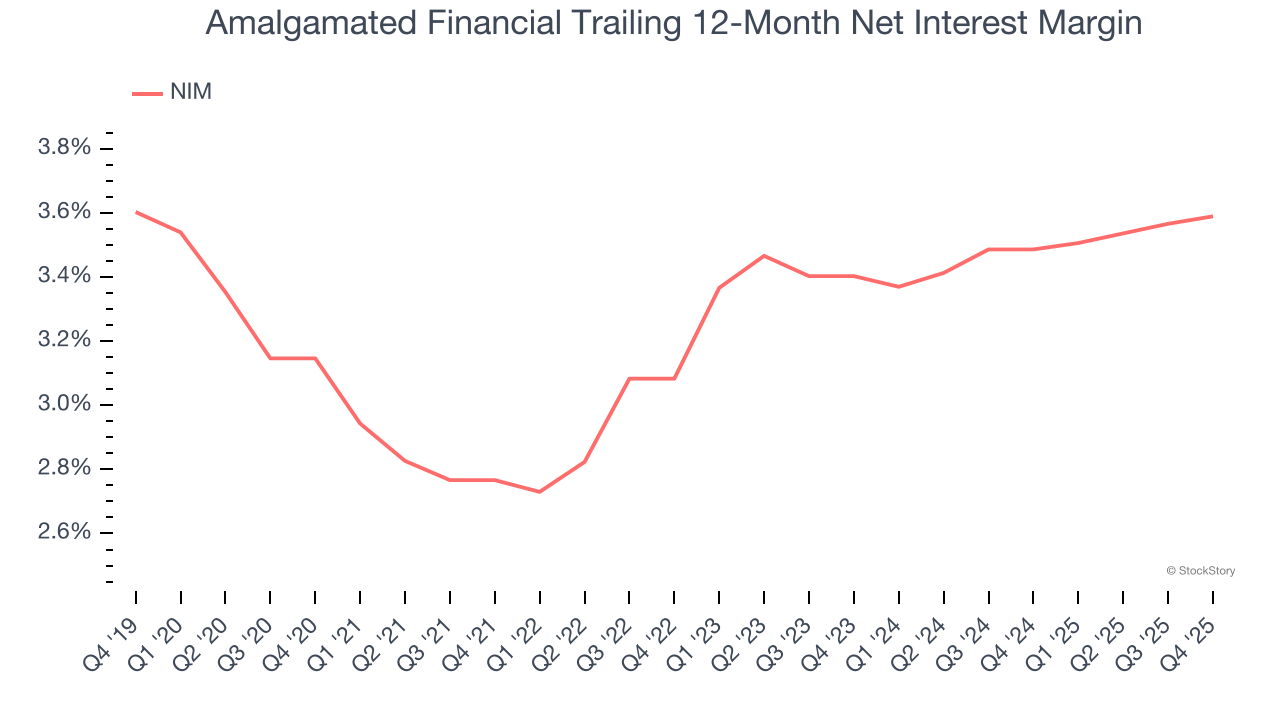

1. Increasing Net Interest Margin Juices Financials

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a bank earns on its loans and what it pays on its deposits. This metric measures how efficiently one can generate income from its core lending activities.

Over the past two years, Amalgamated Financial’s net interest margin averaged 3.5%, climbing by 18.7 basis points (100 basis points = 1 percentage point) over that period.

This expansion was a tailwind for its net interest income, and while prevailing interest rates matter the most for industry net interest margins, banks that consistently increase this figure generally boast higher-earning loan books (all else equal such as the risk of those loans) or provide differentiated services that give them the ability to charge higher rates (pricing power).

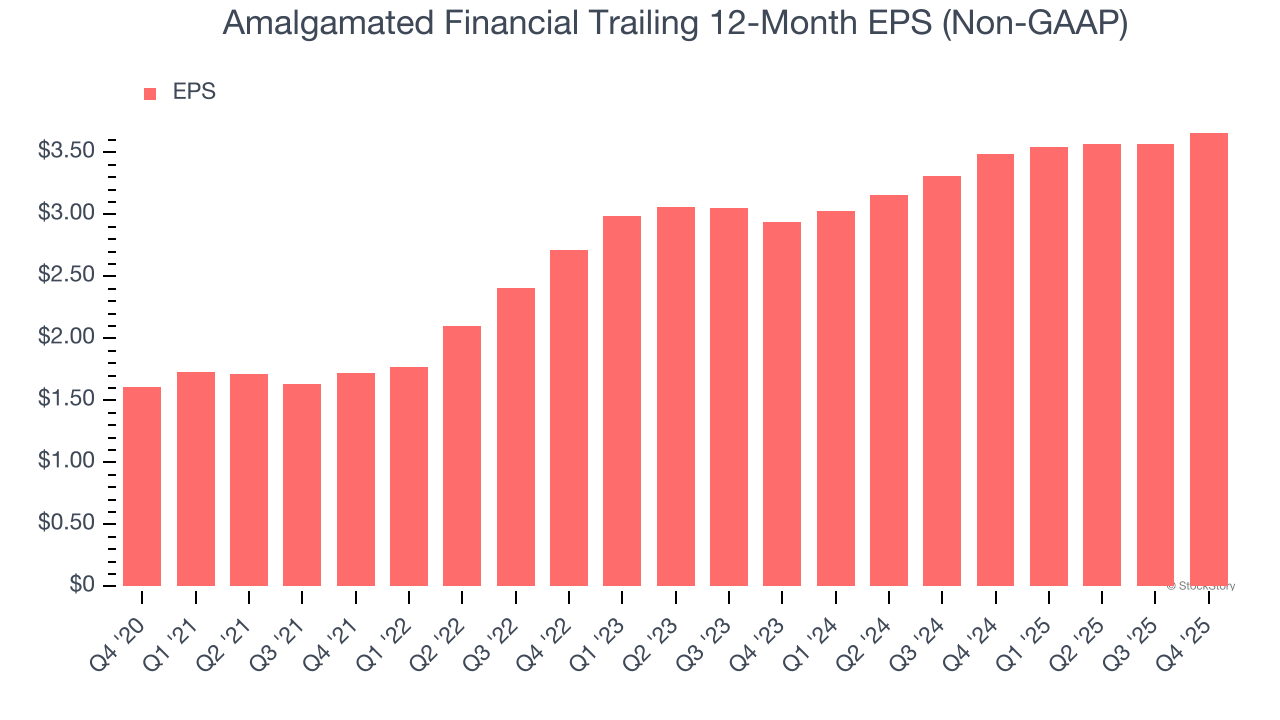

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Amalgamated Financial’s EPS grew at 17.9% compounded annual growth rate over the last five years, higher than its 10.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

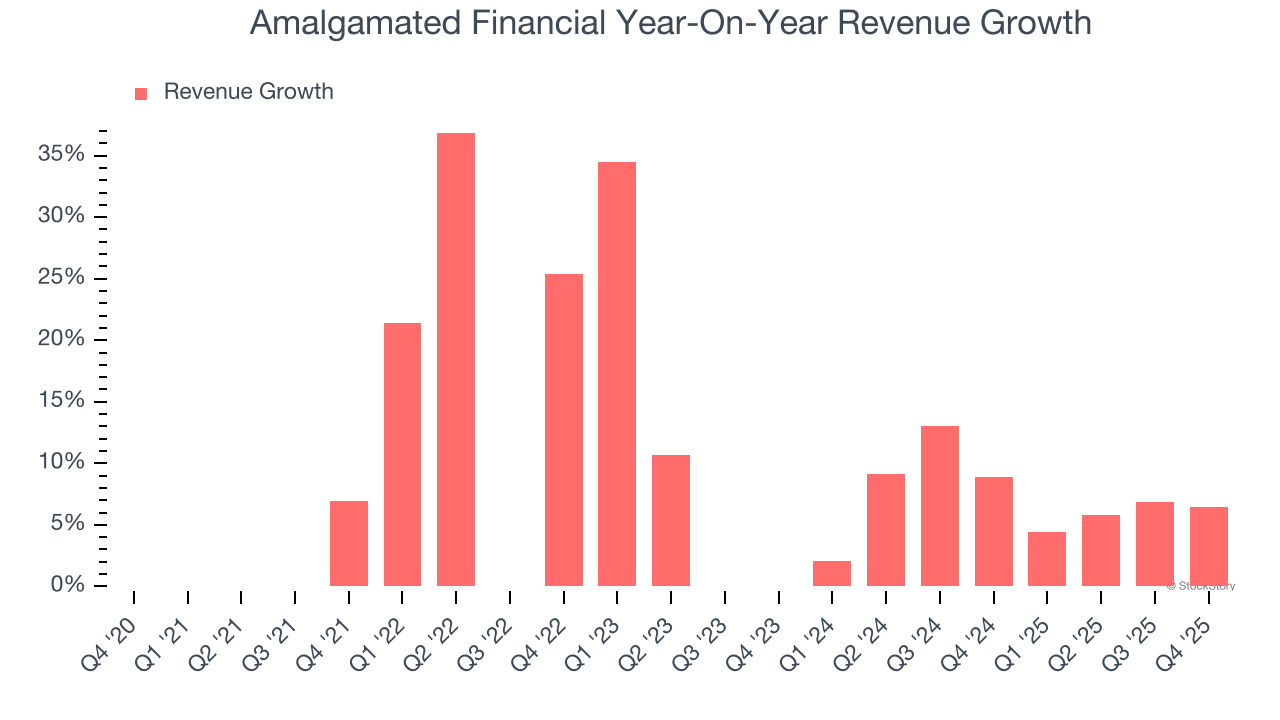

Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Amalgamated Financial’s recent performance shows its demand has slowed as its annualized revenue growth of 7% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Final Judgment

Amalgamated Financial has huge potential even though it has some open questions, and with the recent rally, the stock trades at 1.3× forward P/B (or $39.09 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Amalgamated Financial

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.