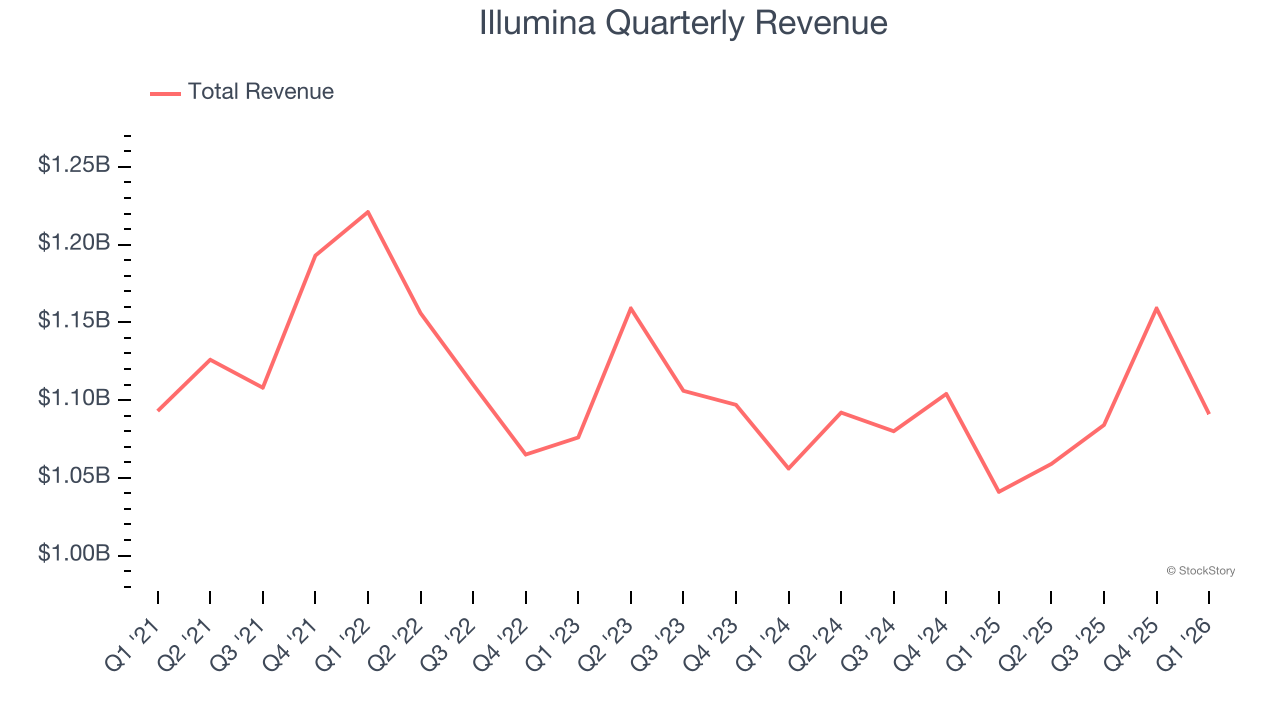

Genomics company Illumina (NASDAQ: ILMN) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 4.8% year on year to $1.09 billion. The company’s full-year revenue guidance of $4.57 billion at the midpoint came in 0.8% above analysts’ estimates. Its non-GAAP profit of $1.15 per share was 9% above analysts’ consensus estimates.

Is now the time to buy Illumina? Find out by accessing our full research report, it’s free.

Illumina (ILMN) Q1 CY2026 Highlights:

- Revenue: $1.09 billion vs analyst estimates of $1.07 billion (4.8% year-on-year growth, 1.8% beat)

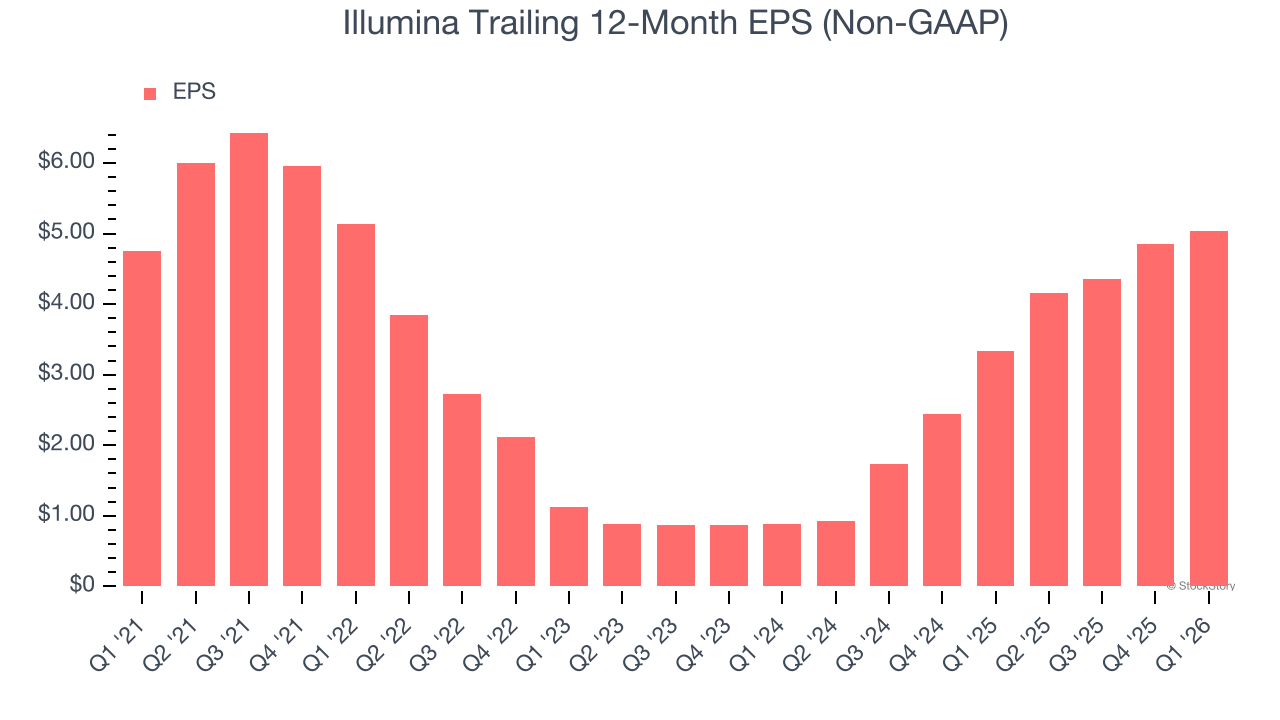

- Adjusted EPS: $1.15 vs analyst estimates of $1.05 (9% beat)

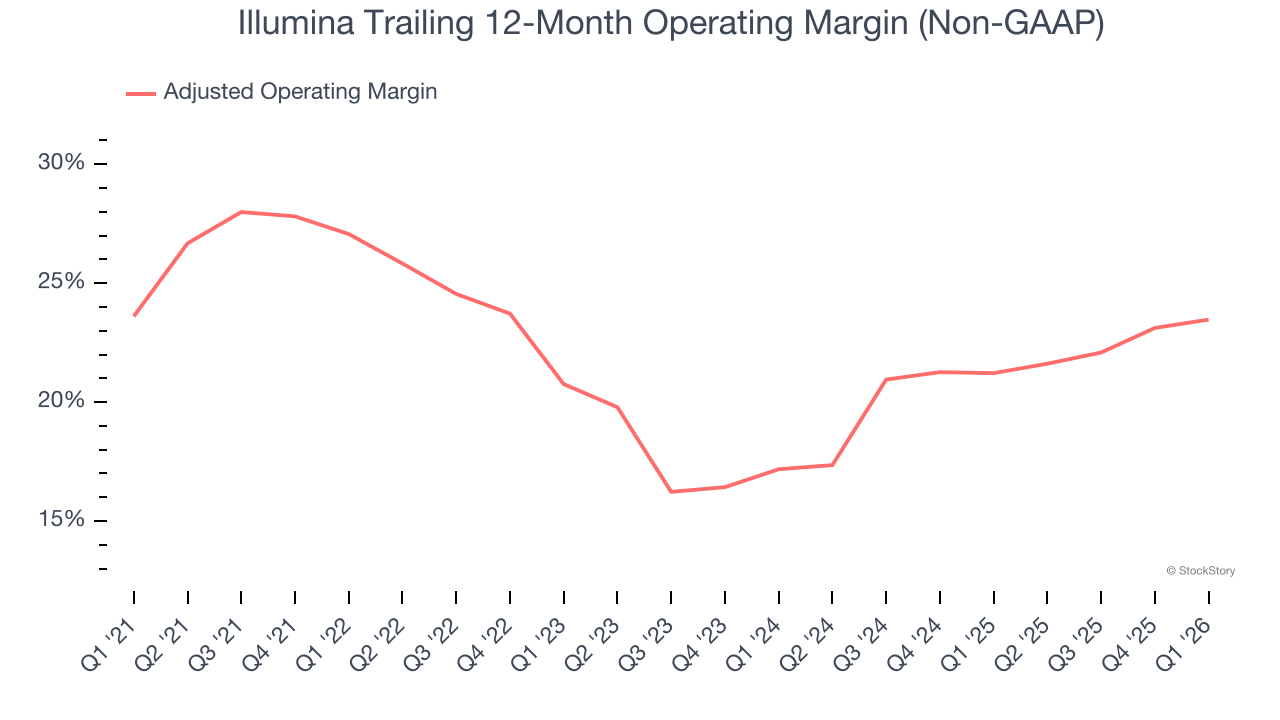

- Adjusted Operating Income: $239 million vs analyst estimates of $219.4 million (21.9% margin, 8.9% beat)

- The company slightly lifted its revenue guidance for the full year to $4.57 billion at the midpoint from $4.55 billion

- Management raised its full-year Adjusted EPS guidance to $5.23 at the midpoint, a 2% increase

- Operating Margin: 19.2%, up from 15.8% in the same quarter last year

- Free Cash Flow Margin: 23%, up from 20% in the same quarter last year

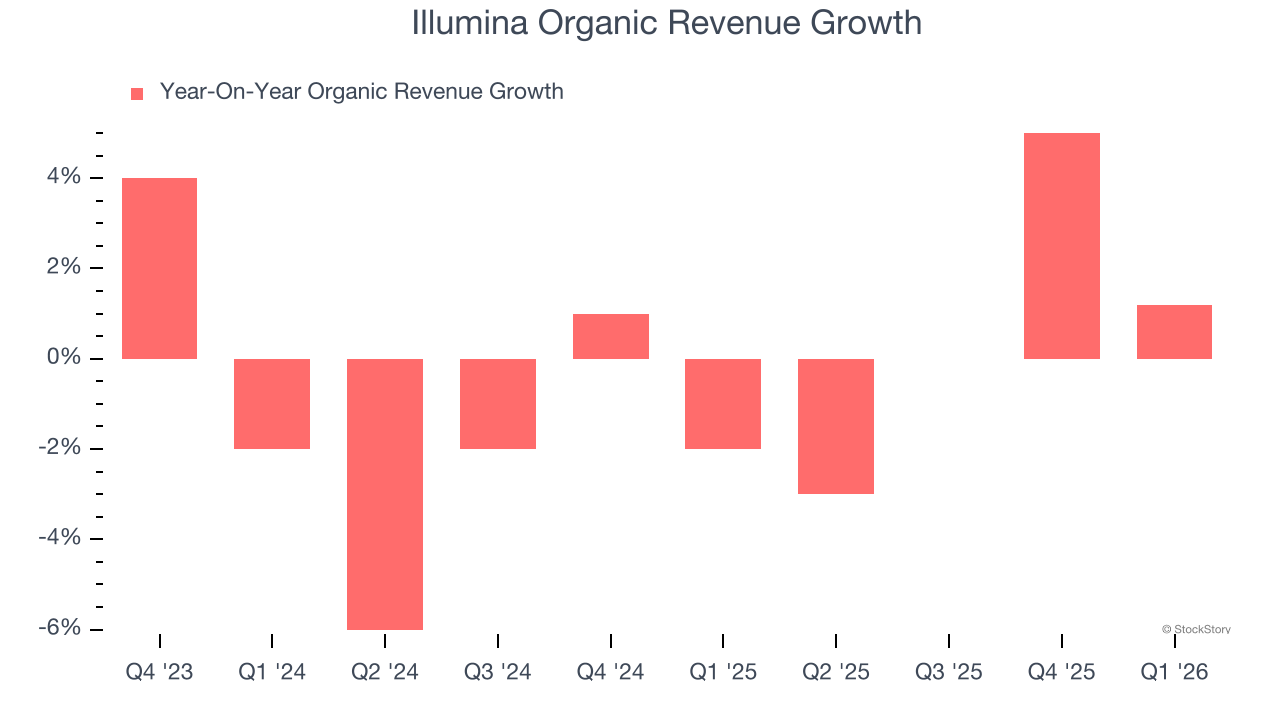

- Organic Revenue rose 1.2% year on year (beat)

- Market Capitalization: $18.29 billion

"Illumina delivered a strong start to 2026, reflecting strength of the Illumina ecosystem and progress against our strategy," said Jacob Thaysen, Chief Executive Officer of Illumina.

Company Overview

Pioneering the ability to read the human genome at unprecedented speed and affordability, Illumina (NASDAQ: ILMN) develops and sells advanced DNA sequencing and microarray technologies that allow researchers and clinicians to analyze genetic variations and functions.

Revenue Growth

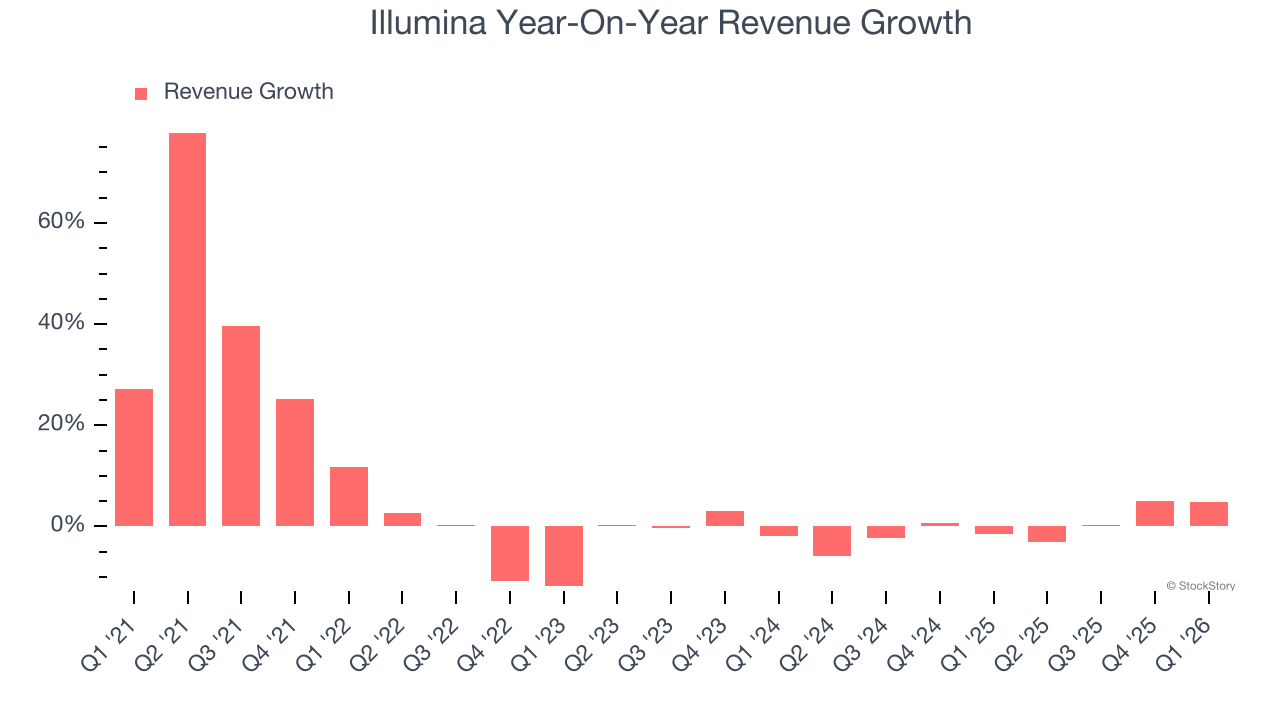

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Illumina grew its sales at a mediocre 4.8% compounded annual growth rate. This was below our standard for the healthcare sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Illumina’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Illumina’s organic revenue was flat. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Illumina reported modest year-on-year revenue growth of 4.8% but beat Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow 4.6% over the next 12 months. Although this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

Illumina has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 22%.

Looking at the trend in its profitability, Illumina’s adjusted operating margin decreased by 3.6 percentage points over the last five years, but it rose by 6.3 percentage points on a two-year basis. Still, shareholders will want to see Illumina become more profitable in the future.

In Q1, Illumina generated an adjusted operating margin profit margin of 21.9%, up 1.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

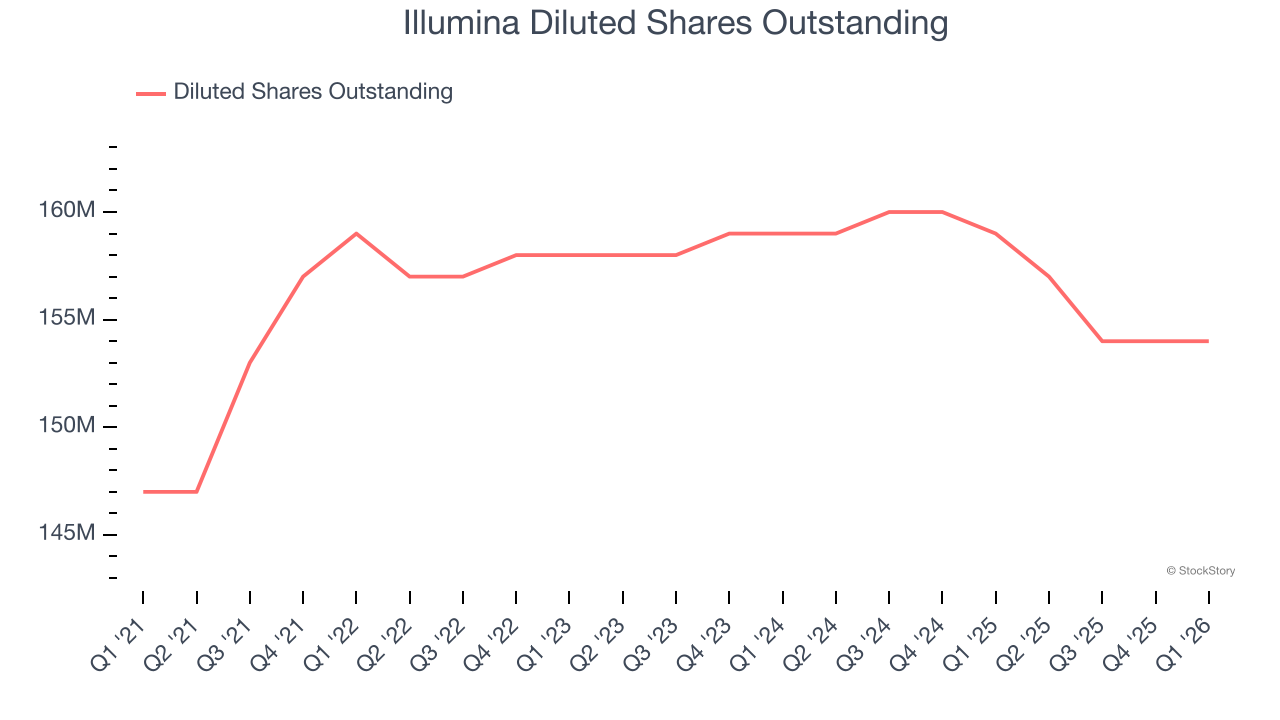

Illumina’s EPS grew at an unimpressive 1.2% compounded annual growth rate over the last five years, lower than its 4.8% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Diving into the nuances of Illumina’s earnings can give us a better understanding of its performance. As we mentioned earlier, Illumina’s adjusted operating margin expanded this quarter but declined by 3.6 percentage points over the last five years. Its share count also grew by 4.8%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q1, Illumina reported adjusted EPS of $1.15, up from $0.97 in the same quarter last year. This print beat analysts’ estimates by 9%. Over the next 12 months, Wall Street expects Illumina’s full-year EPS of $5.03 to grow 6.6%.

Key Takeaways from Illumina’s Q1 Results

It was encouraging to see Illumina beat analysts’ full-year EPS guidance expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. Investors were likely hoping for more, and shares traded down 2.1% to $124.06 immediately after reporting.

Is Illumina an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).