The past year was full of panic for Alphabet (GOOGL). The market seriously feared that Google's absolute control in search would fall under the onslaught of AI solutions from Microsoft (MSFT) and OpenAI, and that key clients like Apple (AAPL) would turn away from the company. But reality put everything in its place. Google didn't just fend off attacks from competitors — it kept the crown, proving that its ecosystem is much stronger than pessimists thought.

GOOGL stock quotes responded logically. Today, shares trade at the $336 level, with the market capitalization having broken through the $4 trillion mark. But that raises a reasonable question: if the fears are behind us and the business works like clockwork, should investors expect the explosive rally to continue? That's where Google faces a fundamental macroeconomic problem.

Alphabet's Fair Valuation and Phenomenal Cash Flow

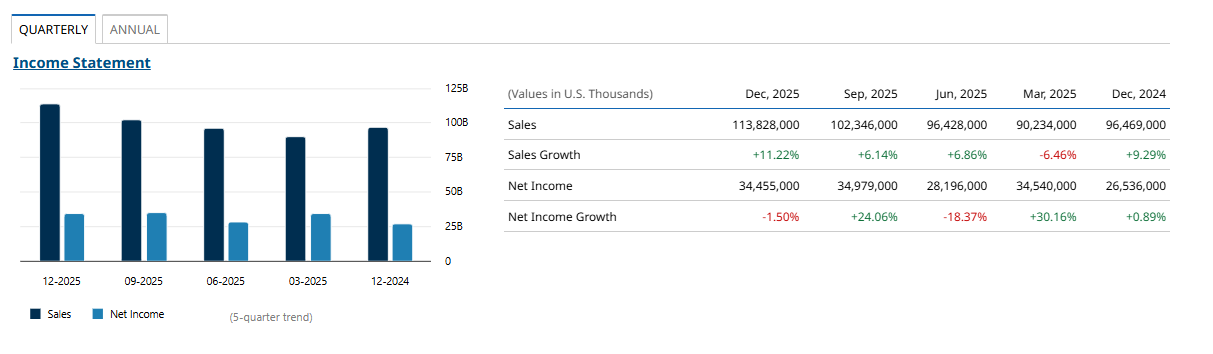

Let's look at the hard numbers. Alphabet showed stunning results for 2025. Annual revenue reached $402.8 billion, marking 15% growth year-over-year (YOY), and net profit soared to $132.1 billion, marking 32% growth. Currently, the trailing price-to-earnings (P/E) multiple is about 31 times. For a tech leader with such cash generation pacing, this is an absolutely fair and adequate valuation. The company has an excellent cash flow, earns huge money, and there are no bubbles in this valuation.

But here is the catch: if you buy shares right now, you are counting on their further growth. And growing capitalization from $4 trillion requires completely different drivers than growing from $1 trillion to $2 trillion.

Proxy Asset of the World Economy: Alphabet Faces a Trap of Scale

Google's main problem today is its own phenomenal success and achieved scale. A $4 trillion market cap and annual revenue over $400 billion mean that the company can no longer grow in a vacuum. Google has become so huge that it has turned into a full-fledged proxy asset of the entire world economy. That's where the tech giant collides with the physical boundaries of its expansion.

In essence, any money in the economy is the equivalent of materialized, "frozen" human labor. Alphabet's revenue — the lion's share of which still comes from advertising and services — depends directly on how much of this "frozen labor" the final consumer has in the form of purchasing power. Google controls search traffic, dominates mobile operating systems with Android, and owns the largest video hosting site, YouTube. It masterfully collects a "digital tax" on world trade and consumption.

At the same time, a harsh ceiling hides within this: Google cannot detach itself from the foundations of global consumption. If the world economy stagnates or grows by a modest 2% to 3% per year, final consumer incomes do not increase. This means advertisers have no reason to multiply their budgets, as the buyer still won't be able to buy more goods. Google has mastered practically all niches accessible to it, and now its organic growth in these segments is rigidly shackled by global GDP growth rates and demographics. There is simply nowhere else for the company to expand because Earth is finite, and new continents with billions of untapped users won't just fall from the sky.

The Explosive AI Phase Has Passed

Bulls will object, asking, "What about artificial intelligence?" Indeed, over the last two to three years, investors have observed how AI became the most powerful driver of the company's revaluation. The implementation of generative models gave a massive boost to the Google Cloud business and allowed the firm to successfully sell premium Gemini Advanced subscriptions.

However, in my view, this explosive period of integration has already passed. The novelty effect is wearing off. Corporations that wanted to transfer their capacities to AI clouds have already done so or allocated their budgets. Users ready to pay for a smart assistant have already subscribed. We have hit a peculiar digital demographic barrier: the number of people and companies with the purchasing power to consume the current spectrum of AI services is finite. AI works excellently to hold Google's dominant position and justifies the current $4 trillion valuation, but within the existing product lineup, it is no longer capable of generating the exponential growth the market saw in 2023 and 2024.

The Visionary's Dilemma: Basic Questions of Economics

To grow further and outstrip the world economy, Google must step into the role of an absolute visionary. Tactical successes — like expanding the Waymo robotaxi fleet into new cities or implementing local AI features into services — are excellent. But for a giant of this size, these are local, niche stories. They are not capable of creating the large-scale cash flow that would add another $1 trillion of value to the company.

Alphabet needs to create fundamentally new markets with huge capacity — markets measured in tens and hundreds of billions of dollars. The company needs to invent services and products that will change human behavior itself and create new forms of consumption.

Here, the industry leader collides with the classic economic triad: what to produce, how to produce, and for whom to produce. The problem is that the answers to these questions in the new tech paradigm have not yet been found. How do you monetize breakthroughs beyond advertising and subscriptions? Who will pay for this? We cannot currently build these future markets into financial models because they haven't been invented yet. As the flagship, Google is forced to walk in the dark, feeling its way toward these markets through colossal capital expenditures.

Alphabet Has Entered a Time of Calm Sailing

Today, Alphabet is a magnificent, high-margin business generating gigantic cash flow. The current valuation at a P/E of around 31 times is absolutely fair and accounts for the company's leadership in the tech sector. The risk that competitors would destroy Google Search did not materialize.

But investors need to change their optics. Google is no longer an overgrown startup capable of doubling itself every couple of years. This is a heavyweight whose pulse beats in time with the world economy. Without inventing fundamentally new, currently non-existent methods of large-scale monetization, the company is doomed to calm, moderate growth alongside the market. The thesis has played out, and the leadership is protected. Now begins the long and difficult work of visionaries searching for new markets beyond the exhausted opportunities of planet Earth.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Tilray Stock Pops on New Trump-Driven Cannabis Hopes. Should You Chase the Rally?

- Tim Cook Is Stepping Down as Apple CEO, AAPL Stock Dips in After-Hours Trading

- Save This Psychedelic Stock Watchlist After Trump’s Latest Executive Order

- BlackBerry Stock Is Soaring on a New Nvidia Deal. Does That Make BB a Buy Here?