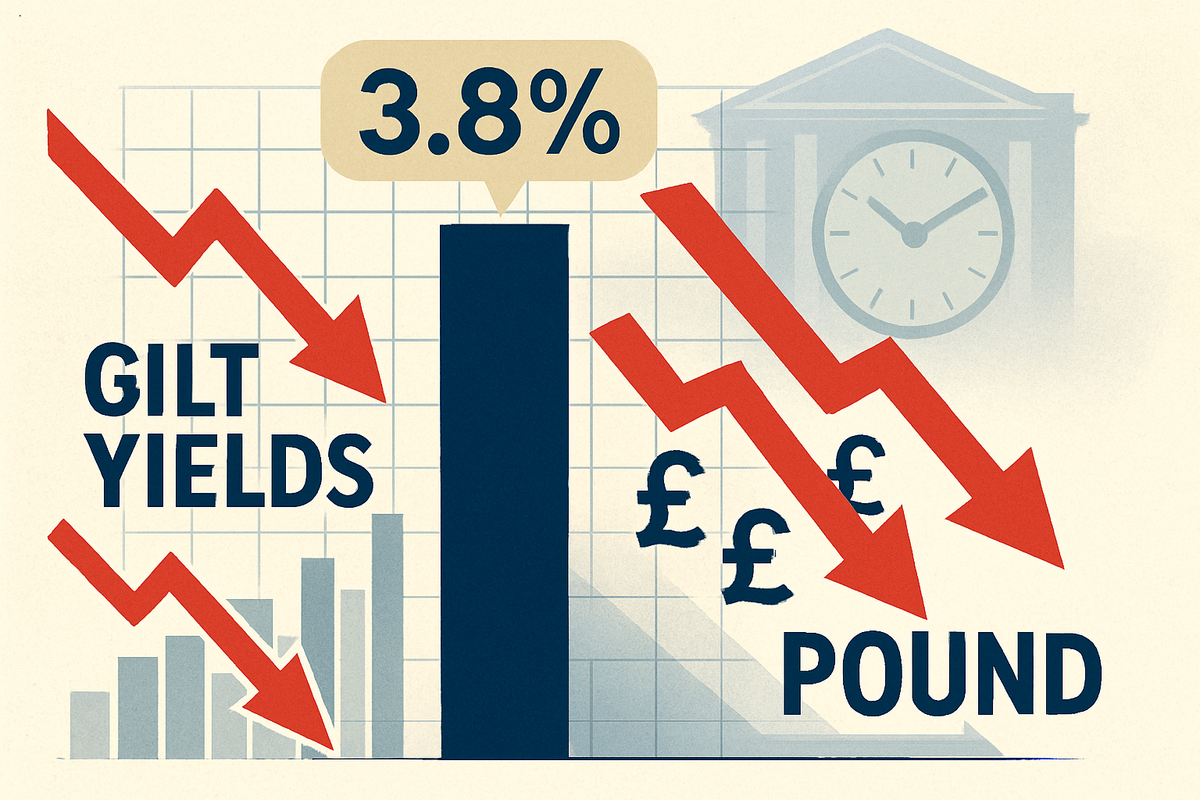

London, UK – October 22, 2025 – The United Kingdom's economic landscape experienced a significant shift today as the Office for National Statistics (ONS) announced that the Consumer Price Index (CPI) annual inflation rate unexpectedly held steady at 3.8% in September 2025. This figure defied widespread economist forecasts, which largely anticipated a rise to 4.0%, and undershot the Bank of England's (BoE) own projection for inflation to peak at 4.0% in the same month. The softer-than-expected data immediately sent ripples through financial markets, triggering a tumble in gilt yields and a slide in the pound, as traders aggressively ramped up their bets on earlier and more substantial interest rate cuts by the Bank of England.

The surprising stability in inflation, while still nearly double the BoE's 2% target, has ignited hopes for a more rapid easing of monetary policy. This development offers a potential reprieve for households and businesses that have grappled with persistent cost-of-living pressures and high borrowing costs. However, the path ahead remains nuanced, with policymakers facing the delicate task of balancing disinflationary trends against underlying economic fragilities.

September's Inflation Surprise: A Deeper Dive into the Data and Market Reaction

The ONS bulletin, "Consumer price inflation, UK: September 2025," released at 7:00 AM on Wednesday, October 22, 2025, revealed that the headline CPI rate remained at 3.8%, matching the rates recorded in August and July 2025. Adding to the surprise, core CPI, which strips out volatile components like energy and food, slowed unexpectedly to 3.5% from 3.6% in August, missing forecasts of 3.7%. Services inflation, a metric closely monitored by the Bank of England, also held firm at 4.7% year-on-year, defying predictions of a rise to 4.8% and falling below the BoE's 5.0% projection.

Several factors contributed to this unexpected moderation. While upward pressures came from transport prices (motor fuels and airfares) and accelerated prices for restaurants, hotels, and clothing, these were significantly offset by a notable slowdown in recreation and culture inflation (falling to 2.7% from 3.2%, partly due to an 8.6% drop in live music prices) and the first fall in food and non-alcoholic drinks prices since May 2024, dropping to 4.5% from 5.1% in August. Housing and household services inflation also eased slightly.

The immediate market reaction was swift and decisive. UK government bond (gilt) yields fell sharply, with the yield on the 10-year gilt trading below 4.40%, a significant drop from over 4.80% just a month prior. The yield on 2-year gilts saw a nine-basis-point decline, reaching its lowest levels since August 2024. Simultaneously, the British pound (GBP) weakened against major currencies, falling 0.4% against the US dollar to trade at USD1.3366 by the close of the London equity market, making it the worst-performing currency in the G-10 group. This depreciation was largely driven by a substantial increase in the probability of a 25-basis point rate cut by the Bank of England in December 2025, which surged from 46% to 75%. Bets for further rate cuts in 2026 also intensified, with 64 basis points now being priced into market expectations.

Key players involved in this unfolding economic narrative include the Office for National Statistics (ONS), the data provider; the Bank of England (BoE), whose Monetary Policy Committee (MPC) will scrutinize this data for future rate decisions; and a host of economists and financial analysts whose forecasts were largely proven incorrect by September's figures. The HM Treasury and the Chancellor, Rachel Reeves, are also closely monitoring the data as they prepare for the upcoming November Budget.

Corporate Fortunes: Who Wins and Loses from Potential Rate Cuts

The prospect of accelerated Bank of England interest rate cuts, spurred by the softer inflation data, will undoubtedly redraw the lines between winners and losers across various sectors of the UK's public companies.

The banking sector is generally expected to face headwinds. Lower interest rates typically compress Net Interest Margins (NIMs) – the difference between what banks earn on loans and pay on deposits – thereby impacting core profitability. While cheaper borrowing might marginally boost loan demand, it often isn't enough to offset the narrower spreads. Major UK banks like HSBC Holdings plc (LSE: HSBA), Barclays PLC (LSE: BARC), and Lloyds Banking Group plc (LSE: LLOY) are highly exposed to the domestic interest rate environment, with a significant portion of their earnings derived from net interest income. A sustained period of lower rates could lead to reduced earnings expectations and consequently, a negative impact on their stock valuations.

Conversely, the real estate sector, particularly housebuilders and property developers, stands to gain significantly. Lower mortgage rates directly enhance affordability for prospective homebuyers, stimulating demand and potentially leading to increased property sales and rising house prices. This translates to higher revenues and profits for housebuilders. Reduced borrowing costs also make it cheaper for developers to finance new projects, encouraging expansion. Companies like Persimmon Plc (LSE: PSN) and Taylor Wimpey plc (LSE: TW.) are well-positioned to benefit from an invigorated housing market, seeing a boost in buyer confidence and sales volumes.

The retail sector could also see a mixed but generally positive impact. With lower mortgage payments, households will have more disposable income, potentially translating into higher consumer spending on goods and services. This directly boosts sales for retailers. Additionally, retailers themselves may benefit from lower borrowing costs for operational financing, such as inventory or store expansions. While consumer confidence might not surge instantly, an active housing market often drives spending on big-ticket home-related items. Major retailers such as Marks & Spencer Group Plc (LSE: MKS), JD Sports Fashion Plc (LSE: JD.), and Tesco Plc (LSE: TSCO) could see an uplift, particularly in discretionary spending categories. Tesco, with its banking arm, might experience some NIM pressure, but its core grocery business is less elastic to economic cycles.

Broader Significance: Navigating the Economic Crosscurrents

The unexpected undershoot in September's inflation data marks a critical juncture for the UK economy, influencing the Bank of England's future policy direction, the broader economic outlook, and creating ripple effects across various markets.

For the Bank of England's monetary policy, this moderation provides a "welcome relief," strengthening the case for a more accommodative stance. The market's aggressive pricing in of rate cuts, potentially as early as December 2025, reflects this sentiment. However, the MPC faces a delicate balancing act. Despite the lower figure, inflation remains well above the 2% target, suggesting that caution will prevail. Splits within the MPC are evident, with some members, like Alan Taylor, warning against overly restrictive rates pushing the economy into a "bumpy landing," while others advocate for maintaining higher rates to fully embed disinflationary pressures. The central bank's primary mandate remains price stability, and sustainable movement towards the target will be key.

For the overall UK economic outlook, softer inflation is generally good news, easing the cost-of-living squeeze and potentially providing "enough oxygen for the economy to pick up some momentum." Weaker energy price inflation and a slowdown in wage growth are contributing factors. However, the economy still faces "stubborn price pressures, mounting government debt, and the prospect of tax hikes." Public borrowing remains high, indicating persistent fiscal challenges that could necessitate difficult decisions in the upcoming November Budget, regardless of the latest inflation figure.

The ripple effects are already visible. The weakening of the Pound Sterling reflects investors' increased bets on lower UK interest rates, reducing the currency's attractiveness. Conversely, demand for UK government bonds (gilts) has strengthened, leading to falling yields, as investors anticipate lower future borrowing costs. In the housing and mortgage markets, more aggressive rate cuts would be a boon for borrowers. For government debt and public finances, while lower inflation might marginally reduce the cost of servicing inflation-linked debt, high debt levels mean the Chancellor will still face pressure to raise revenues. In international markets, a weaker pound could support the FTSE 100, particularly for multinational companies with significant overseas earnings.

Historically, the UK has seen similar inflation surprises. For instance, in February 2024 and January 2024, inflation undershot expectations, prompting similar market reactions of a weakening pound and rallying gilts. These events underscore the perennial challenge for central banks in accurately forecasting and responding to evolving economic conditions. The current situation highlights the tightrope walk for the BoE: managing disinflationary pressures without premature easing that could reignite inflation, or conversely, an overly tight stance that stifles economic growth and risks a "bumpy landing."

What Comes Next: Navigating the Path Ahead

The unexpected September inflation data has significantly altered the short-term and long-term possibilities for the Bank of England's interest rate policy, necessitating strategic adaptations from businesses and policymakers and presenting both opportunities and challenges for investors.

In the short term, the Bank of England is highly likely to adopt a more dovish stance. Having already initiated rate cuts in August 2025, the September undershoot could accelerate the pace of further reductions, potentially even leading to larger 50-basis point cuts or more frequent adjustments. The BoE would likely use strong forward guidance to signal its commitment to accommodative monetary policy, aiming to anchor market expectations for lower rates. There's also a possibility of reviewing its quantitative tightening (QT) program, potentially pausing or slowing it if disinflationary pressures are deemed significant.

Looking at the long term, a sustained inflation undershoot could usher in a prolonged period of "lower for longer" interest rates, potentially pushing the "neutral rate" lower as the BoE prioritizes avoiding deflationary traps. While less likely without a formal government review, persistent undershoots could even spark a debate about the flexibility of the 2% inflation target. With inflation firmly below target, the BoE's secondary mandate of supporting government objectives for growth and employment would gain prominence, leading to more explicitly growth-oriented policy decisions.

Strategic pivots and adaptations will be crucial for businesses. Lower borrowing costs will make new investments more attractive, particularly in sectors like real estate and construction. However, a disinflationary environment might pressure businesses to reduce prices, impacting profit margins. Policymakers, particularly the government, will need to consider complementary fiscal measures to support the economy, such as targeted spending or tax cuts, especially if monetary policy alone proves insufficient. Lower interest rates will reduce government debt servicing costs, potentially creating some fiscal headroom, though high debt levels persist.

For investors, significant opportunities and challenges will emerge. Fixed income assets, particularly UK government bonds (gilts), are likely to perform well as lower interest rates lead to higher bond prices. In equities, growth stocks and small and mid-cap stocks historically tend to outperform in the year following rate cuts, benefiting from lower discount rates and stimulated domestic demand. The real estate sector could see increased attractiveness due to cheaper financing and potential capital appreciation. Conversely, cash holdings will become less appealing due to reduced interest income, and financials (banks) might continue to face pressure on their net interest margins. The global economic environment, including factors like potential trade wars or slowdowns, will remain a key factor.

Comprehensive Wrap-up: A New Chapter for UK Monetary Policy

The September 2025 UK inflation data marks a pivotal moment, signaling a potentially faster trajectory towards disinflation than previously anticipated. The headline CPI holding steady at 3.8% and undershooting forecasts has unequivocally shifted market expectations, with traders now firmly pricing in more aggressive Bank of England interest rate cuts. This has led to an immediate decline in gilt yields and a weakening of the pound, reflecting the market's conviction that the era of tightening monetary policy is drawing to a close.

Moving forward, the Bank of England's Monetary Policy Committee faces the complex task of navigating these evolving economic conditions. While the inflation undershoot offers a welcome respite and strengthens the case for easing, the persistent gap above the 2% target means the BoE will likely proceed with a degree of caution, seeking sustained evidence of disinflation. The path of rate cuts will be closely watched, with implications for household budgets, business investment, and the overall economic growth trajectory.

For investors, the coming months will demand careful consideration of sector-specific impacts. While interest-rate sensitive sectors like real estate and parts of retail are poised for potential gains, the banking sector may face continued pressure on profitability. The shift towards a "lower for longer" rate environment could favor equities and fixed income over cash, but global economic uncertainties will remain a key factor.

What investors should watch for in the coming months are further inflation data releases, any explicit forward guidance from the Bank of England, and the details of the Chancellor's November Budget, which will outline the government's fiscal response. The interplay between monetary and fiscal policy will be crucial in shaping the UK's economic recovery and its ability to achieve sustainable growth while maintaining price stability.

This content is intended for informational purposes only and is not financial advice