Dividends have long been one of the simplest ways companies reward their shareholders. While stock prices may rise and fall with the market, dividends provide investors with a steady return and often reflect a company’s financial strength and confidence in its future. In many ways, dividends turn patient ownership into a rewarding partnership between companies and their investors.

That said, dividend hikes are not uncommon. Companies frequently raise payouts as earnings grow. However, when the size of the increase is significant, it tends to draw attention and invites a closer look at the company behind the move.

That’s precisely what recently happened with Dell Technologies (DELL), the global technology company known for its computers, servers, and enterprise infrastructure powering modern data centers.

The company announced a 20% jump in its quarterly dividend, raising it to $0.63 from $0.525. While dividend hikes are routine, the scale of this increase stands out, especially as Dell pushes deeper into artificial intelligence (AI)-driven growth and benefits from rising demand for AI infrastructure.

With this confidence on display, should investors consider picking up DELL stock now?

About Dell Technologies Stock

Headquartered in Round Rock, Texas, Dell Technologies is one of the early pioneers of the personal computer and server industry. Over the years, it has evolved into a global technology leader helping businesses and individuals build their digital future.

The company, boasting a market capitalization of $97.1 billion, offers a wide range of devices, infrastructure, and services designed for today’s data-driven world. Through its Infrastructure Solutions Group (ISG), Dell provides servers, storage, and networking systems that power AI and data-heavy workloads. Meanwhile, its Client Solutions Group (CSG) delivers PCs, laptops, and workstations used by enterprises and consumers alike, keeping Dell firmly positioned across multiple layers of the modern technology ecosystem.

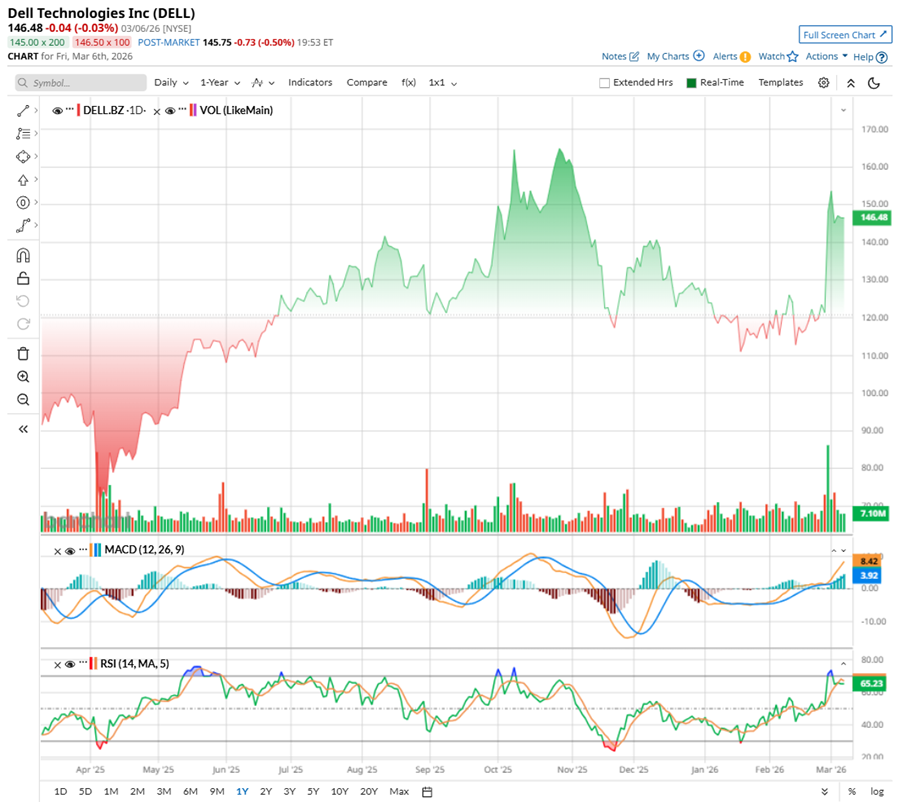

Shares of Dell have had a somewhat bumpy ride in early 2026. The stock faced pressure as the broader hardware sector softened, while a few analyst downgrades, rising competition in the AI server space, and slower-than-expected adoption of AI-powered PCs weighed on sentiment.

However, things changed quickly after Dell reported strong fiscal Q4 earnings on Feb. 26. Investors reacted positively, pushing the stock up nearly 22% in the very next trading session. Thanks to that sharp rally, DELL stock is now up about 56% over the past 52 weeks.

The stock had reached a 52-week high of $168.08 in November 2024 before dropping to a low of $110.22 in January. Since then, shares have rebounded strongly, rising nearly 33% and moving closer to those previous highs again.

Technically, the rebound appears well supported. Trading volumes have picked up noticeably, pointing to stronger buying interest. The 14-day RSI sits near 65, suggesting solid momentum, though it could also hint at a brief pause. Meanwhile, the MACD oscillator remains bullish, with the MACD line above the signal line and a positive histogram, indicating that upward momentum is still in play.

When it comes to valuation, DELL looks surprisingly reasonable. The stock is priced at about 11.53 times forward adjusted earnings and roughly 0.71 times sales, well below many sector peers. At a time when several AI-linked stocks carry lofty price tags, Dell appears more grounded. With solid growth prospects tied to AI infrastructure, this could be a wise entry point for investors.

Dell Doubles Down on Shareholder Rewards with Dividends and Buybacks

Dell Technologies is making a clear effort to reward shareholders. The company has now paid dividends for three straight years, and its recently increased payout of $0.63 per share will be distributed on May 1. That brings Dell’s forward annualized dividend to $2.52 per share, offering a yield of about 1.72%—comfortably above the roughly 1.08% yield of the S&P 500 SPDR (SPY).

With a payout ratio of 20.3%, the dividend still leaves plenty of room for reinvestment. Dell also boosted its share repurchase authorization by $10 billion and returned $2.2 billion to shareholders in the fourth quarter through dividends and buybacks, reinforcing its commitment to shareholder value.

A Closer Look at Dell’s Stellar Q4 Report

Dell Technologies released its fourth-quarter results on Feb. 26, and the server maker wrapped up its fiscal 2026 with record financial performance, driven largely by surging demand for AI-optimized servers and infrastructure.

Fiscal 2026 revenue amounted to $113.5 billion, marking a solid 19% increase from the previous year. The bottom line also moved higher, with non-GAAP EPS climbing 27% year-over-year (YoY) to $10.30. The momentum was particularly visible in the fourth quarter. Dell reported revenue of $33.4 billion, representing an impressive 39% YoY jump. Meanwhile, non-GAAP EPS rose 45% annually to $3.89. Both top and bottom lines beat Wall Street’s estimates.

The strong performance reflected continued demand for Dell’s AI solutions and the company’s ability to execute efficiently as enterprises expand their computing capacity.

Strong cash generation remained another highlight. The company generated $11.5 billion in adjusted free cash flow, up 272% YoY, and returned $7.5 billion to shareholders, including the repurchase of 54 million shares.

A big part of the story lies in Dell’s growing role in the AI infrastructure market. During fiscal 2026, the company generated $64.1 billion in AI orders and shipped $25.2 billion worth of AI systems. In Q4 alone, Dell delivered $9.5 billion in AI servers and ended the year with a record $43 billion backlog. Even after fulfilling numerous orders, the company’s sales pipeline kept expanding, suggesting that demand remains strong rather than being a one-time surge.

Looking ahead, the momentum appears far from slowing down. Dell booked another $34.1 billion in AI orders, signaling continued customer adoption. The enterprise AI customer base has also expanded significantly, now exceeding 4,000 clients. These customers range from neocloud providers and sovereign organizations to traditional enterprises, showing that AI infrastructure spending is spreading across multiple industries.

Management believes this trend will remain a key growth driver. For fiscal 2027, Dell expects roughly $50 billion in AI-related revenue, implying 103% growth YoY. With a strong backlog, a growing customer base, and a rapidly expanding pipeline, Dell appears well-positioned as businesses around the world scale their AI workloads and modernize their data center infrastructure.

Dell’s management expects a solid start to the year. For Q1, revenue is projected to land between $34.7 billion and $35.7 billion, with non-GAAP EPS around $2.90. For fiscal 2027, management sees revenue in the $138 billion to $142 billion range, implying strong YoY growth of 23% at the midpoint, while non-GAAP EPS is projected to be around $12.90 for the year.

Analysts tracking Dell expect fiscal 2027 EPS to rise about 27.8% YoY to $11.82 before growing by another 11.8% annually to $13.21 in fiscal 2028.

What Do Analysts Expect for Dell Technologies Stock?

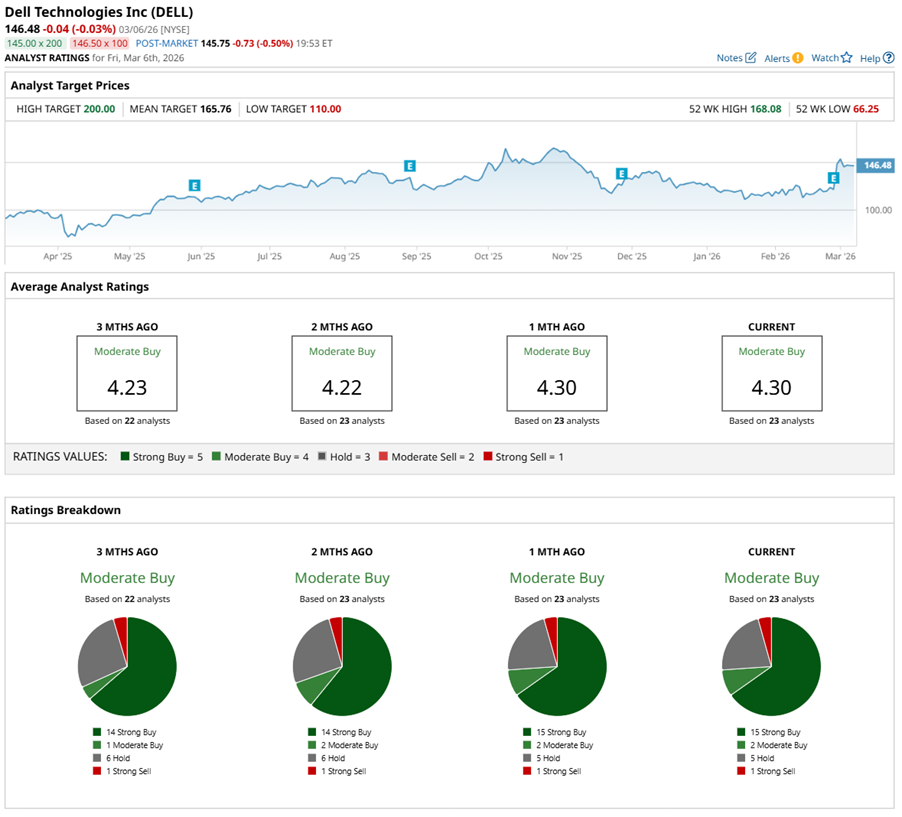

After Dell Technologies delivered its latest earnings report and an upbeat outlook, several brokerages revised their price targets for DELL, reflecting growing confidence in the company’s role in the rapidly expanding AI infrastructure market. For instance, J.P. Morgan raised the target to $165 from $155 while maintaining an “Overweight” rating.

The reasoning is fairly straightforward—Dell is well-positioned in the ongoing AI-driven compute investment cycle. As companies ramp up spending on AI infrastructure, the investment bank expects Dell’s ISG segment to benefit from stronger demand, particularly for servers and storage systems. According to J.P. Morgan, this surge in AI-related spending could help Dell maintain double-digit earnings growth even as some of its traditional segments, such as PCs and general-purpose servers, face pressure from broader economic conditions.

The investment bank also believes Dell’s current valuation may not fully reflect its exposure to AI infrastructure spending and that there’s more room for the stock to command a higher valuation multiple than it has historically. Dell may not always be viewed as the most direct beneficiary of the AI boom compared with chipmakers like Nvidia (NVDA), but still, the opportunity remains significant because the AI ecosystem relies heavily on servers, storage, and networking systems—areas where Dell plays a critical role.

Meanwhile, Bank of America analyst Wamsi Mohan also raised his price target for DELL to $155 from $135 while maintaining a “Buy” rating. He believes the company’s outlook for the coming year looks “unexpectedly strong,” supported by steady AI demand and solid execution.

However, the analyst did flag a potential concern. Dell raised PC prices last year to offset higher costs, and those increases could eventually affect demand. He anticipates the second half of the year to be slightly softer than the first. Even so, the analyst believes the overall trend remains favorable, with enterprise AI adoption still in its early stages and demand for Dell’s storage and infrastructure solutions continuing to grow.

Analysts monitoring DELL are optimistic, with a consensus rating of “Moderate Buy.” Out of 23 analysts, 15 recommend a “Strong Buy,” two suggest a “Moderate Buy,” five are on the sidelines, giving it a “Hold” rating, and one analyst advises a “Strong Sell.”

Its average price target of $165.76 implies upside potential of 13.2%. Meanwhile, the Street-high target of $200 suggests DELL stock could rise as much as 36.5% from the current price levels.

Final Thoughts on DELL Stock

Putting it all together, Dell Technologies appears to be steadily strengthening its investment case. The company is benefiting from a powerful tailwind in AI infrastructure, delivering strong earnings growth while maintaining a relatively reasonable valuation. Meanwhile, the 20% dividend hike and expanded buyback program signal management’s confidence in the company’s cash generation and long-term outlook.

Of course, risks remain, including cyclical pressure in the PC market and broader macro uncertainty. But with strong demand for AI servers, a growing backlog, and steady analyst backing, Dell Technologies appears poised for growth. For investors looking at the AI infrastructure space without paying steep valuations, the stock could be worth a closer look—although whether to step in now may still depend on individual risk appetite.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart