The artificial intelligence (AI) market continues to expand, but the focus is gradually shifting beyond just advanced chips. Data centers today rely heavily on memory, high-speed optical links, and networking systems to support growing AI workloads. As more companies invest in AI infrastructure, these core components are becoming critical to performance, and in many cases, are facing supply constraints.

BNP Paribas analyst Karl Ackerman points out that investors are increasingly leaning into these constrained parts of the value chain. Instead of chasing crowded compute names, the focus is turning to areas where supply remains tight, particularly memory ICs and optical components.

Backed by strong demand for AI servers, he expects DRAM prices to spike significantly in the near term, with NAND following a similar trajectory. The analyst estimates that the data center switch and transceiver total addressable market crossing $140 billion by 2028, highlighting the sheer scale of this opportunity.

Against this backdrop, companies tied to these critical layers are gaining attention. Arista Networks (ANET), Fabrinet (FN), and Ciena Corporation (CIEN) are well-positioned names, and the stock could be wise portfolio additions this earnings season.

Data Center Stock #1: Arista Networks

Headquartered in Santa Clara, California, Arista Networks is a networking company specializing in high-performance solutions for cloud, enterprise, and AI-driven environments. With a market capitalization of about $202.3 billion, it stands as a key player in modern digital infrastructure.

Its portfolio includes Ethernet switches, routers, and software platforms built on its Extensible Operating System (EOS), enabling scalable, automated, and secure network operations. Arista’s technology is widely used across data centers and campus networks, helping organizations efficiently manage large-scale data traffic and evolving connectivity needs.

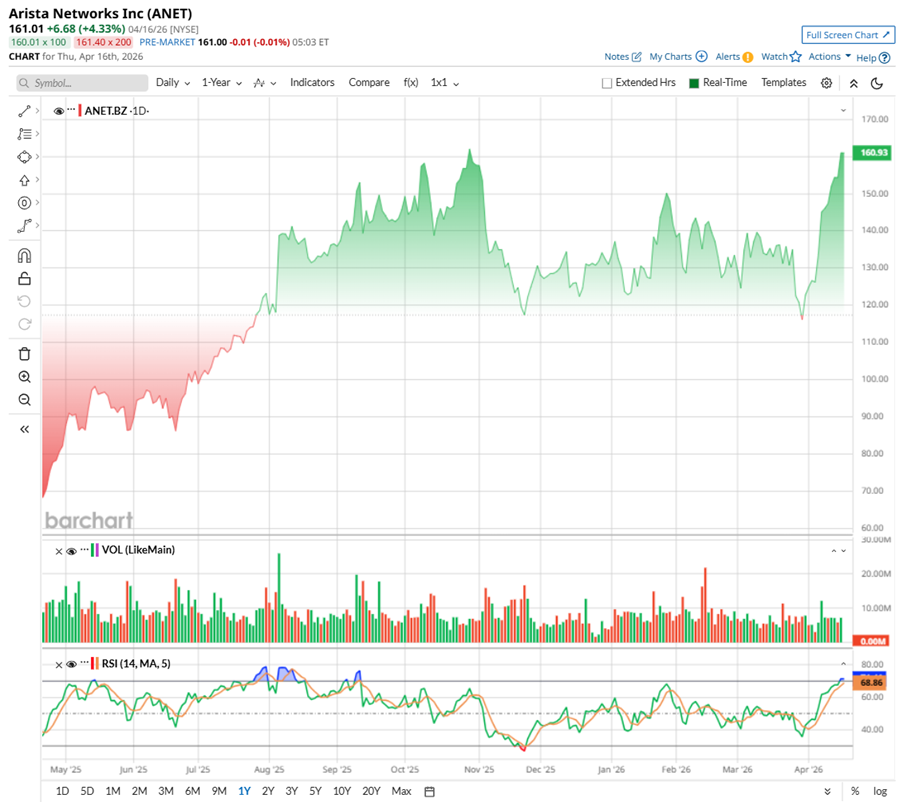

Arista Networks has had a dynamic run over the past year, balancing strong gains with periods of volatility. The stock touched a 52-week high of $164.94 in October 2025, and on Apr. 17, it reached a high of $165.28. Still, the bigger picture remains compelling with ANET stock is up 131.4% over the past 52 weeks, highlighting sustained investor confidence in its role within AI and cloud networking.

In 2026, momentum has stayed intact, with the stock gaining 25.74% year-to-date (YTD), supported by renewed optimism around AI infrastructure spending. Short-term moves have also been notable. For instance, shares jumped 3.2% on Feb. 25 amid strong sector sentiment, fueled by developments like major AI hardware partnerships, reinforcing demand for data center networking.

More recently, the stock climbed over 11.82% in just five days, signaling continued buying interest. Much of the stock’s performance over the past year is tied to Arista’s strong fundamentals. Rising demand from hyperscalers, consistent revenue growth, solid margins, and a track record of earnings outperformance all continue to support its long-term growth story.

Technically, rising volumes indicate active investor participation and renewed positioning, while the 14-day RSI, now 73.48, suggests the stock is now at the overbought territory, pointing to strong momentum but also the possibility of a near-term pause.

Arista Networks is not exactly cheap right now, priced at 48.88 times forward adjusted earnings and 17.67 times sales. But that premium tells that the market is clearly willing to pay up for its strong position in the AI networking boom.

When Arista Networks reported its fourth-quarter 2025 results on Feb. 12, it was clear the AI networking wave was still working in its favor. Revenue amounted to $2.5 billion, up 28.9% year-over-year (YOY), as demand from cloud giants and enterprises stayed strong.

Profits followed through, with non-GAAP net income rising to about $1.1 billion from $849.6 million last year, while non-GAAP EPS of $0.82 grew 24.2% annually and beat Street’s expectations. Meanwhile, Arista kept pushing innovation, rolling out new AI-focused networking solutions and unveiling its R4 series platforms – built to deliver faster speeds, lower power usage, and better efficiency for modern data centers.

The cloud networking giant is set to report its first-quarter earnings results for fiscal 2026 on May 5, Tuesday, after the market closes. For Q1 2026, management has guided revenue to around $2.6 billion, with non-GAAP gross margins expected between 62% and 63%, and operating margins projected to come in near 46%, reflecting steady profitability alongside continued growth.

Meanwhile, analysts tracking the company project revenue for the quarter to land somewhere around $2.6 billion, with EPS anticipated to rise 14.3% YOY to $0.72. Looking further ahead to fiscal 2026, EPS is estimated to grow 16.6% annually to $3.16, followed by a further 19.9% annual rise to $3.79 in fiscal 2027.

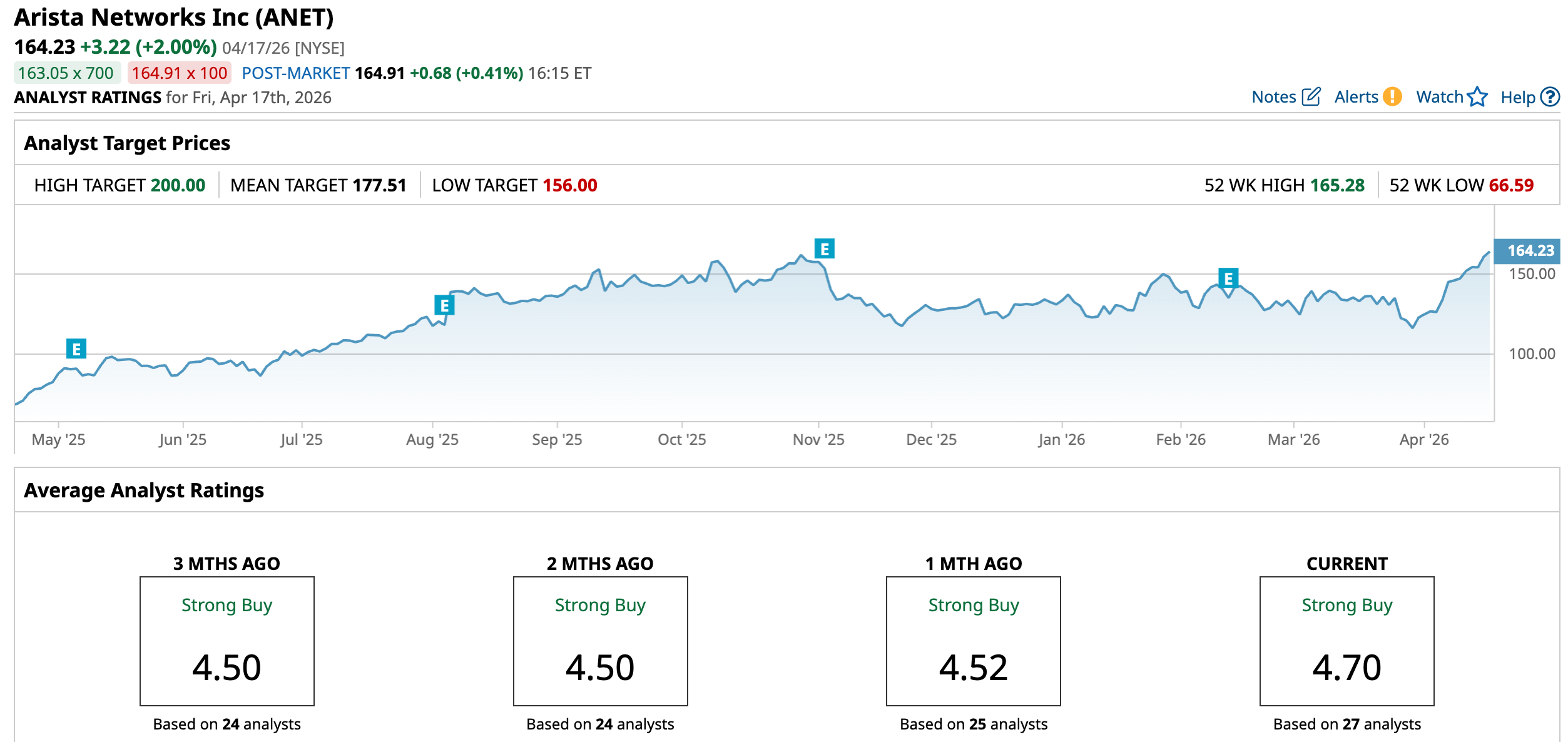

Wall Street is majorly bullish on ANET. Overall, ANET has a consensus “Strong Buy” rating. Of the 27 analysts covering the stock, 22 advise a “Strong Buy,” two suggest a “Moderate Buy,” and the remaining three analysts are playing it safe, giving it a “Hold” rating.

ANET’s average analyst price target of $177.51 suggests an upside potential of 8.1%, while the Street-high target price of $200 suggests that the stock could rally as much as 21.8%.

Data Center Stock #2: Fabrinet

Founded in 2000, Fabrinet began as a specialized manufacturer focused on low-volume, high-mix production of complex optical components. Today, it is a leading provider of advanced optical packaging and precision manufacturing services for OEMs across industries like optical communications, automotive, medical devices, and industrial systems.

The company offers end-to-end capabilities, from design and engineering to assembly and testing, with operations spanning Thailand, the U.S., China, and Israel. Positioned at the heart of the AI infrastructure buildout, Fabrinet plays a key role in producing high-speed optical and electronic components, benefiting from rising demand and expanding capacity in next-generation networking.

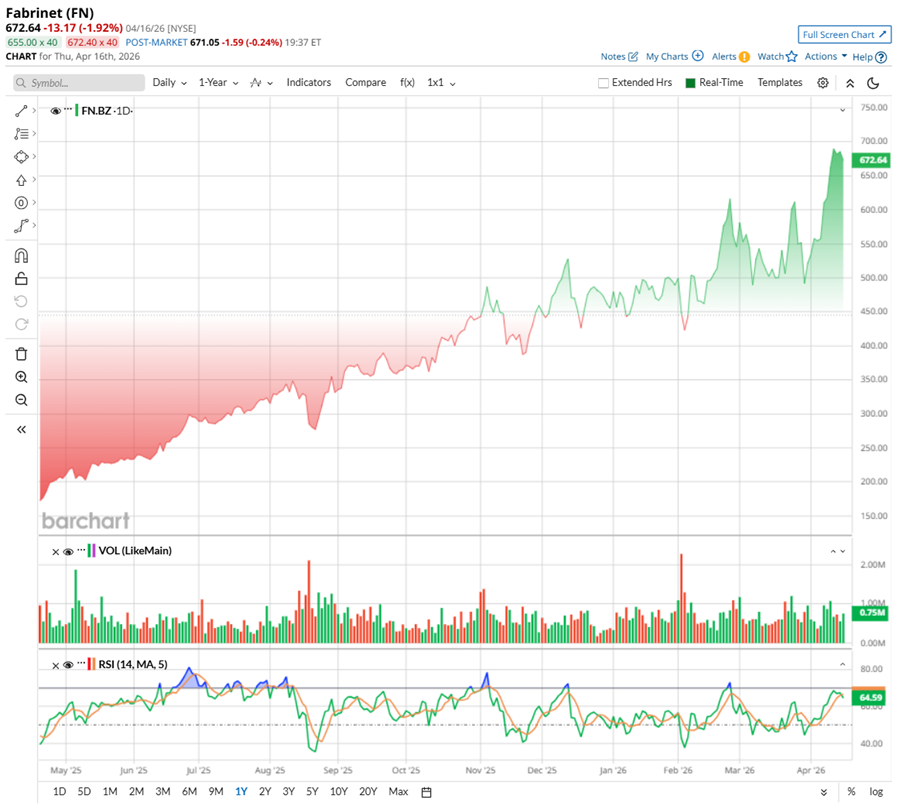

Valued at a market cap of $24.1 billion, shares of Fabrinet have been on a powerful run that’s hard to ignore. Over the long term, the stock has delivered massive gains – up nearly 2,000% over the past decade, 605% in three years, and 315% over the last two.

Zooming into the past year, the momentum has only accelerated. FN bounced sharply from a 52-week low of $167.33 last April and has surged about 312% since then. Over the past 52 weeks, the stock is up 275%, with a further 68% gain over the past six months. In 2026 alone, shares have climbed nearly 51.45%, even touching a high of $708.20 on Apr. 14 before a modest 2.6% breather. Notably, the stock has logged 63 new highs over the past year.

Technically, the setup still looks solid. Volume is picking up, with the 14-day RSI sittiing at 66.54, and momentum feels strong without screaming overbought just yet.

FN trades at a premium, with the stock currently priced around 53.87 times forward adjusted earnings and 5.30 times forward sales – both above the sector averages and its own historical medians. That may seem expensive, but it also reflects confidence in the company’s strong execution, rising demand for optical components, and its growing role in powering AI-driven data center infrastructure.

Fabrinet delivered a strong second quarter for fiscal 2026 on Feb. 2, comfortably beating both its own guidance and Wall Street’s projections. Revenue climbed 35.9% YOY to $1.13 billion, while adjusted EPS rose 28.7% annually to $3.36, reflecting solid execution and operating leverage.

Growth was broad-based, driven by multiple key programs across its business. Optical Communications remained the core driver, contributing 73% of total revenue. Within that, Datacom accounted for 33%, generating $278.1 million, while Telecom made up 67%, with revenue jumping 59.3% annually to $554.4 million.

Looking ahead, the management expects continued momentum, guiding Q3 revenue between $1.15 billion and $1.20 billion and non-GAAP EPS in the range of $3.45 to $3.60.

Wall Street monitoring Fabrinet expects the company to be a strong beneficiary of the AI boom. Earnings are projected to stay solid in the near term, with Q3 EPS around $3.40. Looking ahead, fiscal 2026 EPS is expected to climb 37.5% YOY to $12.73, followed by another 19.3% annual increase to $15.18 in fiscal 2027.

Analysts are confident, with FN stock having an overall “Moderate Buy” rating, a downgrade from the “Strong Buy” two months back and last month. Nevertheless, of the 10 analysts tracking the stock, six back it with a “Strong Buy,” one has a “Moderate Buy,” while three sit on the sidelines with a “Hold" rating.

FN currently trades above its average target of $585. The Street’s highest $715 price target hints the stock could rally as much as 3.64%.

Data Center Stock #3: Ciena

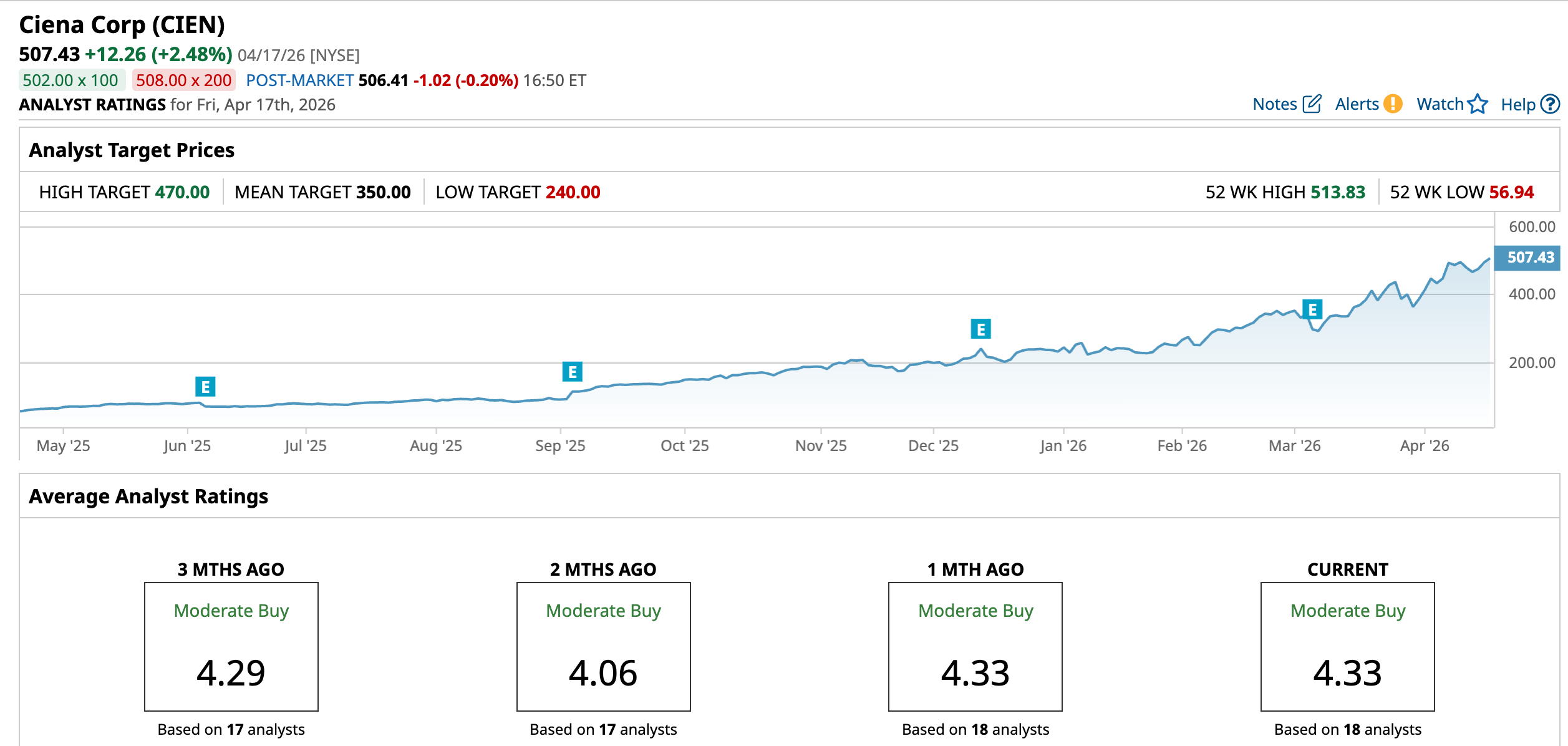

Valued at $70 billion, Ciena operates at the heart of the global data network. Founded in 1992 and headquartered in Hanover, Maryland, the company designs high-speed optical and packet networking systems that move vast amounts of data across long distances. It may not build AI directly, but it enables it at scale. With a presence in over 35 countries and its WaveLogic technology powering nearly 85% of leading service providers, Ciena remains a critical backbone of today’s digital and AI-driven infrastructure.

Ciena has been on a remarkable run, reflecting its growing importance in the AI-driven networking cycle. Over the past 52 weeks, the stock has surged an eye-catching 743.75%, significantly outperforming even the broader tech benchmark S&P 500 Information Technology Index ($SRIT). Strong fundamentals, including a record backlog and rising demand for optical networking, have helped fuel this rally.

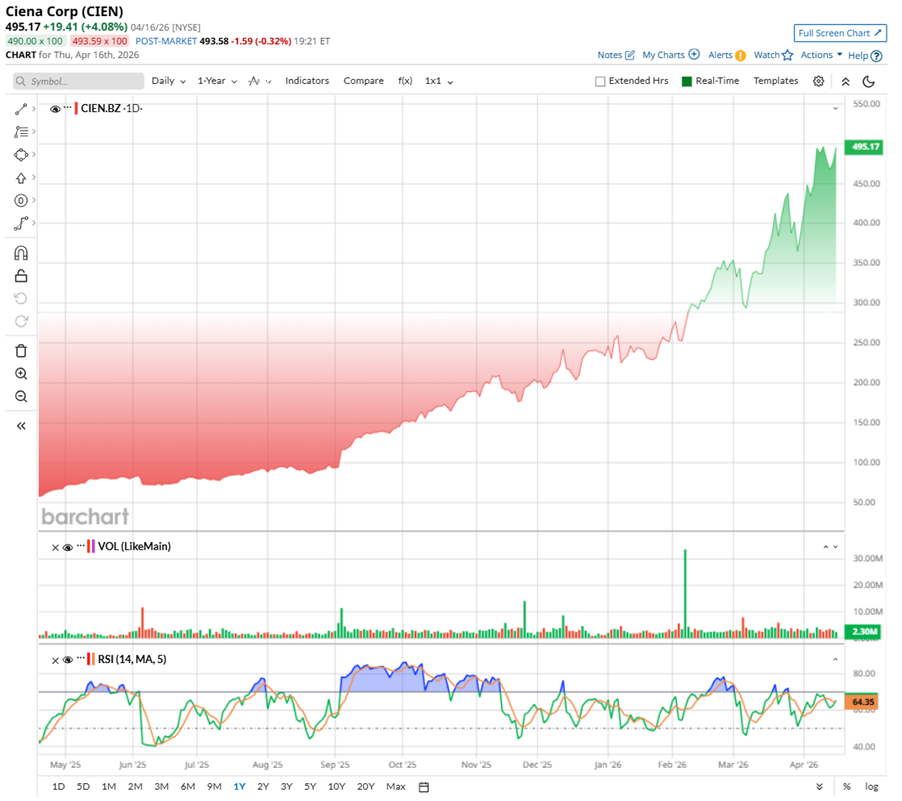

The journey has not been entirely smooth. Following its March 5 earnings, the stock briefly dropped 12.9% on conservative guidance, but sentiment quickly turned. Since its Q1 report, CIEN has rebounded sharply, gaining over 44%. In the past month alone, the stock is up 37%, even hitting a high of $513.49 on Apr. 9 before a modest pullback.

What stands out is consistency. CIEN has marked new highs 28 times in 2026 so far. Technically, momentum remains healthy, with steady volumes and a 14-day RSI at 67.09, suggesting the uptrend still has room to run.

From a valuation standpoint, CIEN carries a premium price tag, priced at around 80.54 times forward adjusted earnings and 11.43 times sales. But in this AI-driven cycle, the market is willing to pay up for companies owning critical infrastructure, and Ciena’s positioning in high-speed optical networks keeps that premium story alive.

Ciena entered 2026 with strong momentum, delivering a standout Q1 performance – report released on March 5 – that put it firmly on investors’ radar. The company reported record revenue of $1.43 billion, up 33% YOY, comfortably beating expectations. Adjusted EPS came in at $1.35, more than doubling from $0.64 last year and well ahead of consensus estimates.

This growth was largely driven by its Optical Networking segment, which surged over 40% as hyperscalers ramped up spending to upgrade data center interconnects for AI workloads.

During the Q1 earnings call, management described demand as “incredibly strong,” supported by robust order activity and long-term commitments. Notably, backlog increased by $2 billion in the quarter, taking the total to $7 billion, providing solid visibility into revenue through 2027.

Plus, Ciena ended the quarter with $1.12 billion in cash and cash equivalents and generated $228 million in operating cash flow.

Looking ahead, management guided fiscal 2026 revenue between $5.9 billion and $6.3 billion, implying 28% growth at the midpoint. Ciena continues to see strong momentum, driven by rising AI-led demand for high-speed connectivity. CEO Gary Smith called demand for its 1.6T WaveLogic 6 solutions “unprecedented,” supported by a record order book extending visibility through 2027. Growth is broad-based, including markets like India, though supply constraints remain a key limiter.

With hyperscalers expected to spend billions in 2026, including on networking, Ciena is well positioned. As copper reaches its limits, optical solutions are gaining ground, opening long-term opportunities. Investments in next-gen interconnects and strong customer expansion should support continued growth into fiscal 2026.

Analysts are also optimistic, forecasting EPS to climb 210% annually in fiscal 2026 to $5.08, followed by another 46.9% growth in fiscal 2027 to $7.46, pointing to sustained, high-growth ahead.

Analysts are turning more positive on CIEN stock as demand tied to AI infrastructure builds momentum. BofA Securities recently raised its price target to $550, citing a strong backlog, giving better revenue visibility. The firm also sees hyperscaler spending accelerating, with CapEx expected to rise 65% in 2026. Its higher valuation multiple reflects confidence in Ciena’s role in interconnect and optical networks.

Meanwhile, Samik Chatterjee of JPMorgan also lifted CIEN’s price target to $550, maintaining an “Overweight” rating, driven by continued AI-led demand across networking and optical infrastructure.

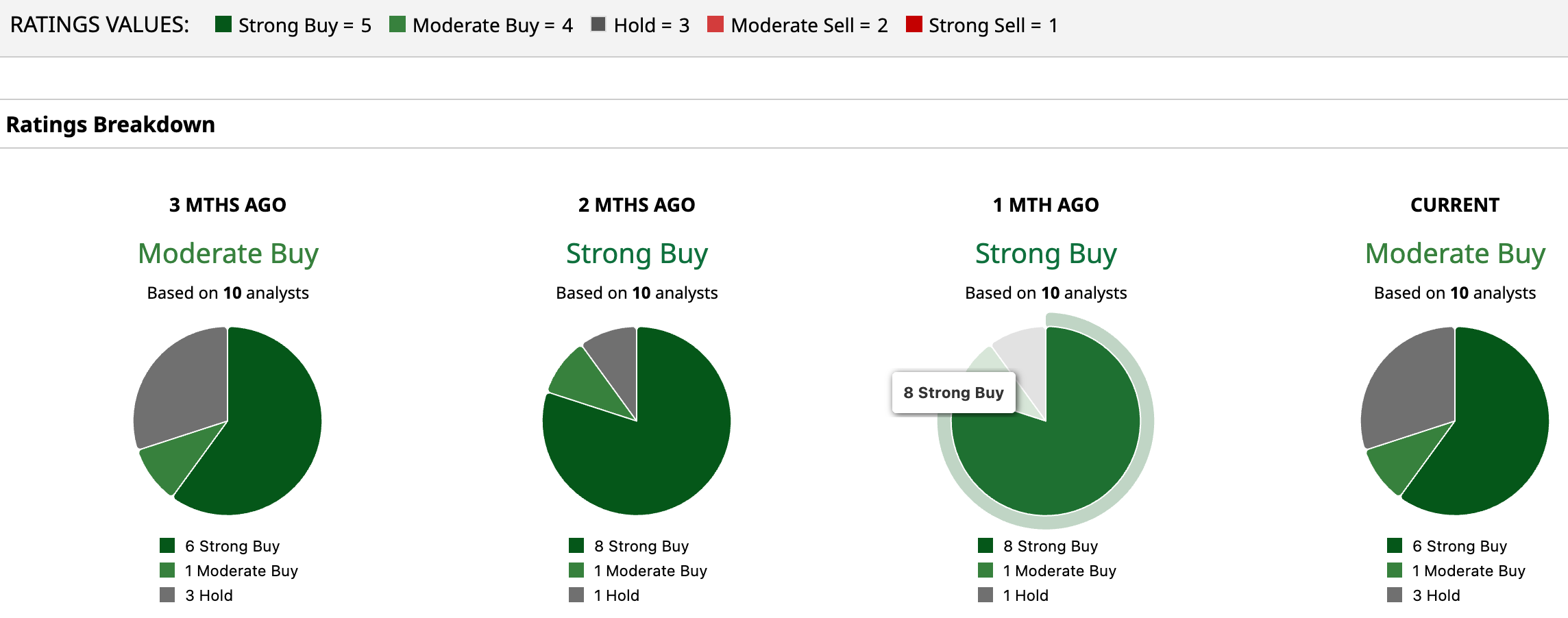

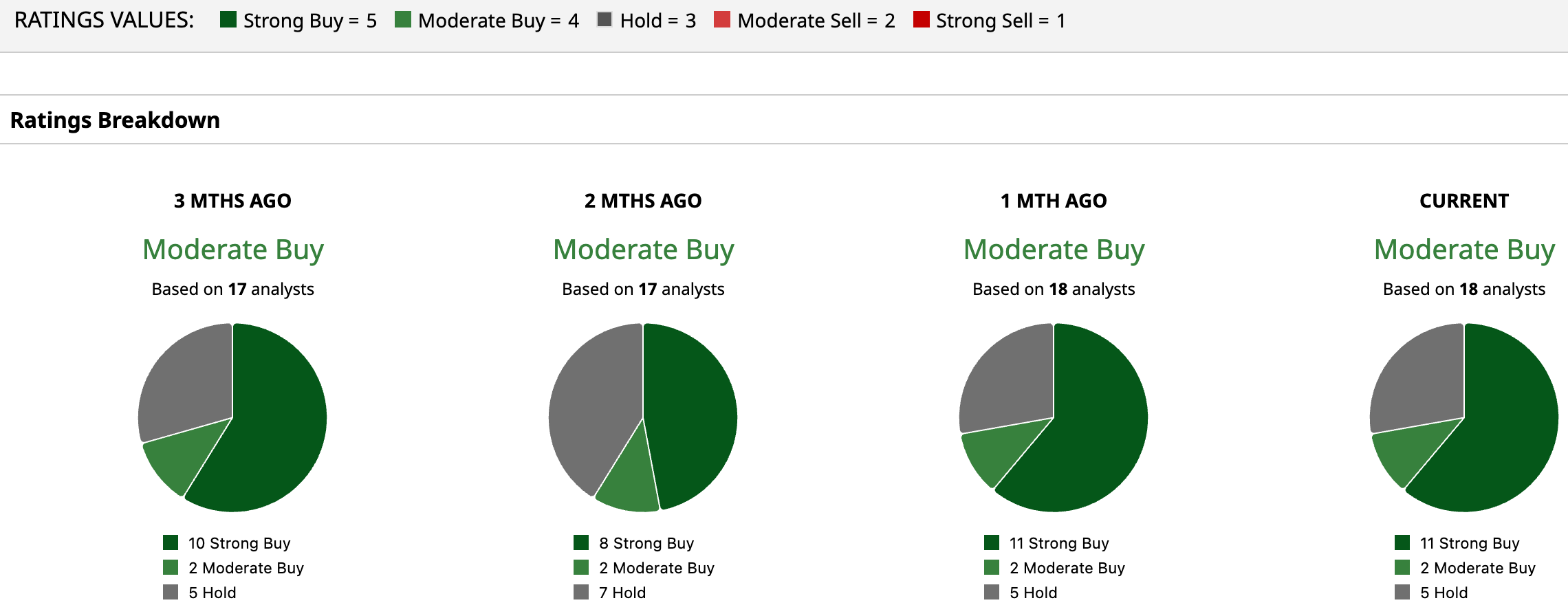

Overall, analysts are bullish on CIEN’s growth potential, giving the stock a consensus rating of “Moderate Buy.” Of the 18 analysts covering the stock, 11 advise a “Strong Buy,” two suggest a “Moderate Buy,” and the remaining five recommend a “Hold.”

Given CIEN’s exceptional rally, the stock trades far above the average analyst price target of $350 as well as the Street-high target price of $470.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart