The U.S. manufacturing sector signaled a complex "good news, bad news" narrative this morning as the Institute for Supply Management (ISM) released its February 2026 report. While the headline Purchasing Managers' Index (PMI) showed the sector expanding for the second consecutive month, a massive spike in the Prices Index to 70.5—the highest level since mid-2022—has sent shockwaves through the financial markets. The data suggests that while factories are humming again, the cost of doing business is escalating at a pace that could reignite broader inflationary pressures across the economy.

The duality of the report presents a significant challenge for policymakers and corporate leaders alike. The expansion in activity, driven by a modest recovery in new orders, is being overshadowed by a "tariff transmission lag" and a sudden spike in raw material costs, particularly in the metals and energy sectors. As manufacturers grapple with these surging inputs, the threat of "margin squeeze" has moved to the forefront of investor concerns, casting a shadow over the industrial recovery that began earlier this winter.

A Volatile February: Expansion Meets Price Shocks

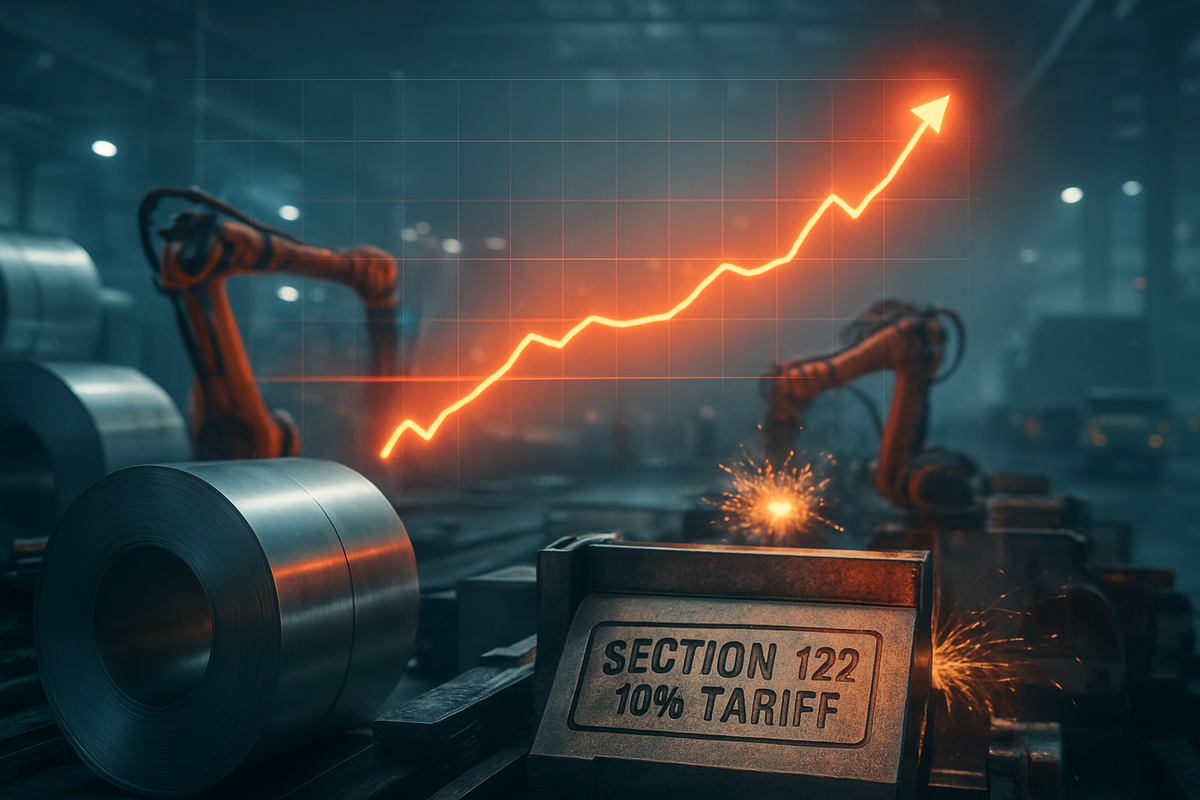

The February 2026 Manufacturing PMI registered 52.4, a slight increase from January’s reading and the second straight month above the 50-point threshold that separates expansion from contraction. This modest growth follows a difficult 2025 characterized by high interest rates and stagnant demand. However, the true story of the month lies within the sub-indices. The Prices Index took a massive leap from 59.0 in January to 70.5 in February. Historically, a reading above 70 in the Prices Index is associated with rapid inflationary spikes that eventually force the Federal Reserve’s hand.

This sudden surge is closely tied to a chaotic shift in trade policy. Following a February 2026 Supreme Court ruling in Learning Resources Inc. v. Trump, which challenged the administration's use of the International Emergency Economic Powers Act (IEEPA) for broad tariffs, the White House pivoted on February 24 to a new 10% global tariff under Section 122 of the Trade Act of 1974. This new baseline applies to roughly $1.2 trillion in annual imports. While lower than some of the 50% "national security" duties seen in late 2025, the broad application of this global tariff has effectively raised the floor for commodity prices, especially steel, aluminum, and petroleum-based products.

The timeline leading to this report shows a sector that was just beginning to find its footing. In late 2025, the Prices Index was stable in the high 50s, but the sudden regulatory and legal shifts surrounding metal duties in the last 30 days have forced suppliers to hike quotes almost overnight. Primary metals reported the highest price increases of all six major manufacturing industries, followed by petroleum and coal. Market reaction was swift this morning, with Treasury yields ticking upward as traders began pricing in a more "hawkish" Federal Reserve for the remainder of 2026.

Winners and Losers: The Great Margin Squeeze

The dramatic rise in the Prices Index creates a clear divide between raw material producers and the heavy manufacturers who consume them. Domestic steel producers like Nucor Corporation (NYSE: NUE) and Steel Dynamics, Inc. (NASDAQ: STLD) are currently positioned as potential "winners" in the short term. These companies can leverage the protectionist environment and the 70.5 Prices Index to push through their own price hikes, defending their margins even as scrap and energy costs rise. United States Steel Corp (NYSE: X) also stands to benefit from the reduced competition of the new 10% global tariff, though it must navigate a more competitive landscape than it did under the previous 50% Section 232 duties.

Conversely, the "losers" list is dominated by the automotive and aerospace giants who are the primary victims of rising metal costs. Ford Motor Company (NYSE: F) and General Motors Company (NYSE: GM) are facing a severe headwind; with the average vehicle containing over 2,000 pounds of steel and 400 pounds of aluminum, these firms are seeing their bill of materials explode. Analysts suggest that the cumulative impact of these tariffs could add upwards of $1,000 to the production cost of high-volume trucks and SUVs. Tesla, Inc. (NASDAQ: TSLA) is similarly exposed due to its heavy reliance on aluminum for chassis and battery enclosures, testing the company's ability to maintain its aggressive price-cutting strategy of years past.

The aerospace sector is also feeling the heat. The Boeing Company (NYSE: BA) is dealing with a double-edged sword: rising costs for specialized alloys and titanium, coupled with supplier delivery times that have "stretched" to 55.1 in the latest ISM report. This indicates that suppliers are not only charging more but are also struggling to keep up with orders. Similarly, GE Aerospace (NYSE: GE) is seeing "substantial increases in operating expenses," according to recent analyst notes, which could dampen the gains from its robust aftermarket services business if the inflation in raw materials isn't curtailed soon.

Broader Significance: The "Tariff Transmission" Dilemma

The February ISM report is more than just a data point; it represents a fundamental shift in the 2026 economic narrative. For the past year, the market hoped for a "soft landing" where inflation would gracefully return to 2%. However, the 70.5 Prices Index reading suggests that inflation is becoming "sticky" and "embedded" in the supply chain. This event fits into a broader trend of "re-globalization" or "near-shoring," where the U.S. is prioritizing domestic production at the cost of higher consumer prices. The transition from Section 232 "national security" tariffs to the broader Section 122 "global" tariffs marks a new era where trade policy is used as a primary tool for industrial management, regardless of the inflationary side effects.

Historically, when the ISM Prices Index crosses the 70 mark, it serves as a precursor to Consumer Price Index (CPI) spikes three to six months down the line. This "tariff transmission lag" means that the true pain for the American consumer may not be felt until the summer of 2026, when companies have exhausted their pre-tariff inventories and are forced to pass 100% of the new costs to the public. Comparisons are already being drawn to the inflationary cycles of the late 1970s, where supply shocks in energy and materials created a "stagflationary" environment that was difficult to break without aggressive interest rate hikes.

What Lies Ahead: Demand Destruction or Adaptation?

In the short term, investors should prepare for a "margin squeeze" across the industrial sector. Companies that lack "pricing power"—the ability to raise prices without losing customers—will likely see their earnings downgraded in the coming quarters. We may see a strategic pivot among manufacturers toward "value engineering," where companies attempt to use less expensive materials or simplify designs to offset the 10% global tariff burden. However, in heavy industries like aerospace and defense, such pivots take years, not months.

The long-term risk is "demand destruction." If Caterpillar Inc. (NYSE: CAT) or the Big Three automakers are forced to raise prices by 5-10% to cover their material costs, it could lead to a slowdown in construction and consumer spending. This creates a potential scenario where the manufacturing expansion we see today (PMI 52.4) is short-lived, as the very inflation driving the Prices Index eventually kills the demand that fueled the recovery. Watch for "Inventory Sentiment" in future ISM reports; if manufacturers begin to feel their inventories are too high because customers are walking away from higher prices, the expansion could flip back into contraction by late 2026.

Wrap-Up: A Precarious Path Forward

The February 2026 ISM report is a stark reminder that economic growth and price stability are often at odds in a protectionist trade environment. While it is encouraging to see the manufacturing sector expanding for a second month, the jump to a 70.5 Prices Index is a "red alert" for inflation. The pivot to Section 122 tariffs has created a new, higher baseline for production costs that will reverberate through every layer of the American supply chain, from the steel mills of the Midwest to the car dealerships of the Sunbelt.

As we move forward, the market will be laser-focused on the Federal Reserve's response. Will the central bank view this as a temporary "tariff shock," or will they see it as the beginning of a new inflationary spiral? For investors, the coming months will require a high degree of selectivity. Companies with deep moats and the ability to pass on costs will survive, while those buried in the middle of the supply chain may find 2026 to be one of their most challenging years on record. Watch the next three months of CPI data closely—it will tell us if the 70.5 reading was a one-time anomaly or the start of a new, expensive reality.

This content is intended for informational purposes only and is not financial advice.