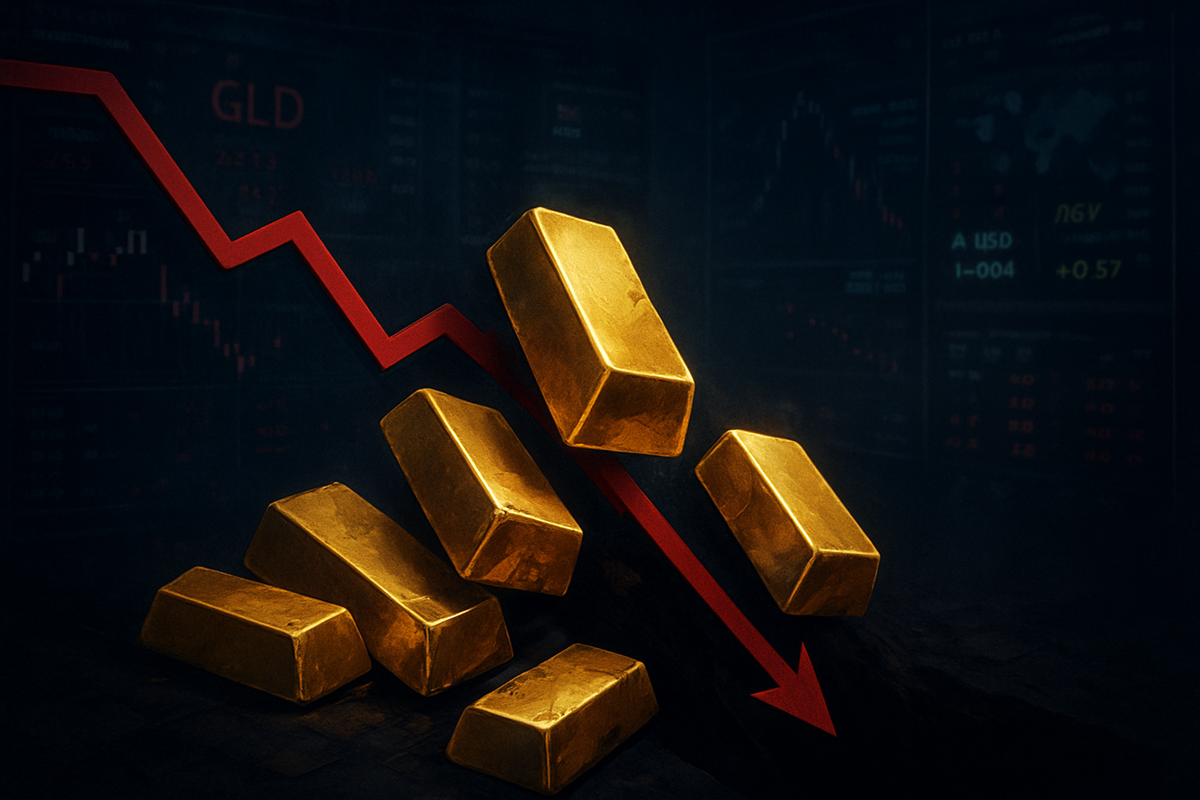

In a week that will be etched into the annals of financial history, the gold market has experienced a staggering reversal of fortune. After two years of seemingly relentless gains, the precious metal has plunged below the critical $4,400 mark, marking its worst weekly performance in 15 years with a 9.6% decline. This sudden evaporation of value has sent shockwaves through global markets, catching many retail and institutional investors off guard who had viewed the yellow metal as an invincible bastion against geopolitical instability.

The immediate implications are profound for the broader financial ecosystem. The sell-off represents a massive liquidation of what was the world's most crowded "safe-haven" trade, as capital pivots toward the liquidity of the U.S. Dollar and the attractive returns of rising Treasury yields. For the public, this crash signals a potential shift in inflation expectations and a re-evaluation of how "risk-off" assets are defined in an era of high-interest rates and escalating Middle Eastern tensions.

The Descent from the Peak: A Timeline of Volatility

The current carnage stands in stark contrast to the euphoric atmosphere of early 2026. On January 21, 2026, gold reached a historic all-time high of $5,602, driven by a combination of central bank diversification and fears of a broadening conflict in the Middle East. At that time, analysts were predicting a march toward $6,000, fueled by the SPDR Gold Shares (NYSE: GLD) reaching record-high inflows. However, the market sentiment began to sour in February as the nature of the Iran conflict shifted from a localized skirmish to a broader energy crisis, triggering an unexpected economic reaction.

The timeline of the crash began last Monday, when a series of hawkish comments from Federal Reserve officials suggested that interest rates would remain "higher for longer" to combat oil-induced inflation. This triggered a massive sell-off in the bond market, sending the 10-year Treasury yield to heights not seen in years. As yields rose, the opportunity cost of holding non-yielding gold became untenable for large-scale institutional funds. By Wednesday, a "margin call" environment emerged; as other asset classes dipped, investors were forced to liquidate their winning gold positions to cover losses elsewhere, accelerating the downward spiral.

Initial market reactions have been characterized by panic and a flight to cash. The 9.6% weekly drop is the largest since the 2011 peak-to-trough correction, effectively erasing nearly four months of gains in a matter of five trading sessions. Stakeholders ranging from jewelry manufacturers to sovereign wealth funds are now grappling with a landscape where the "inflation hedge" is falling even as energy prices remain elevated. The suddenness of the move has left technical charts "broken," with gold slicing through several key support levels that had held firm throughout 2025.

Market Winners and Losers in the Wake of the Crash

The most immediate "losers" in this scenario are the major gold miners and the exchange-traded funds that track the metal. The SPDR Gold Shares (NYSE: GLD) saw its largest single-day outflow in its history this past Thursday, as investors scrambled for the exits. Major mining companies, which had expanded operations based on $5,000 gold projections, are now facing a margin squeeze. Newmont Corporation (NYSE: NEM) and Barrick Gold Corporation (NYSE: GOLD) both saw their stock prices tumble by double digits this week, as the market revalued their future cash flows against a significantly lower spot price.

Conversely, the U.S. Dollar and high-yield instruments have emerged as the surprise winners of this crisis. The Invesco DB US Dollar Index Bullish Fund (NYSEARCA: UUP) has surged as the greenback reasserted its dominance as the world’s premier liquidity tool during times of war. While gold is a store of value, it cannot provide the 4.5%+ "risk-free" return currently offered by the iShares 7-10 Year Treasury Bond ETF (NASDAQ: IEF). Investors who pivoted early into short-duration fixed income or dollar-denominated assets have found themselves shielded from the volatility that has decimated the commodities sector.

Streaming and royalty companies, such as Franco-Nevada Corporation (NYSE: FNV), are also under intense pressure. These firms, which provide upfront capital to miners in exchange for future production at fixed prices, are highly sensitive to spot price fluctuations. While they carry less operational risk than traditional miners, their premium valuations are built on the assumption of a high-gold-price environment. If the price remains below $4,400 for an extended period, these companies may see significant downward revisions in their earnings guidance for the remainder of 2026.

A Fundamental Shift in the Safe-Haven Narrative

This event fits into a broader industry trend where the traditional inverse correlation between the U.S. Dollar and gold has become more pronounced during geopolitical shocks. In previous decades, a conflict involving Iran would almost certainly drive gold prices higher. However, in 2026, the global market’s extreme sensitivity to inflation and interest rates has created a new paradigm. When war drives up oil prices, it now drives up inflation expectations, which in turn drives up Treasury yields. In this "yield-driven" environment, gold loses its luster to the interest-bearing Dollar.

The ripple effects on competitors and partners in the precious metals space are likely to be long-lasting. Silver and platinum, often viewed as "beta" plays on gold, have suffered even more dramatic percentage losses. This suggests a broader de-risking move across the entire commodities complex. Historical precedents, such as the 1983 gold crash and the 2013 "taper tantrum" sell-off, remind us that when gold enters a corrective phase after a massive run-up, the consolidation period can last for years rather than months.

Furthermore, the policy implications for central banks are significant. Over the last 18 months, central banks in emerging markets were the primary buyers of gold. If these institutions perceive that gold has lost its stability as a reserve asset, they may slow their purchasing programs or even begin to diversify back into U.S. Treasuries to take advantage of the high yields. This would remove the "floor" that many analysts believed existed at the $4,500 level, potentially leading to a self-reinforcing cycle of lower prices.

Looking Ahead: The Path to $3,500?

In the short term, the market is looking for a signs of stabilization, but many analysts are pessimistic. A growing chorus of bears, including lead strategists at several Wall Street firms, is now warning that the floor could be as low as $3,500. This level represents a return to the long-term trend line established before the 2024 breakout. For this scenario to manifest, Treasury yields would likely need to remain above 5% while the Iran conflict continues to provide a "liquidity premium" to the U.S. Dollar rather than a "safety premium" to bullion.

Strategically, mining companies will likely need to pivot toward cost-cutting and dividend protection. The era of aggressive expansion and high-cost acquisitions that defined 2025 is likely over. We may see a wave of consolidation in the junior mining sector, as smaller players with higher production costs find themselves unable to survive in a sub-$4,400 environment. Market opportunities may emerge for "value hunters" if the price hits the $3,500 to $3,800 range, but for now, the momentum is decidedly to the downside.

The long-term scenario depends heavily on the Federal Reserve's next moves. If the U.S. economy begins to buckle under the weight of high interest rates, the Fed may be forced to pivot and cut rates regardless of inflation. Such a move would be the ultimate catalyst for a gold recovery, as it would destroy the yield advantage currently held by Treasuries. However, until there is clear evidence of an economic slowdown or a de-escalation in the Middle East, gold investors appear to be in for a period of painful "price discovery."

Final Assessment: The End of the Bull Run

The historic 9.6% drop in gold prices marks a definitive end to the parabolic "Super-Rally" of 2025. By breaking below $4,400, the market has signaled that it is no longer willing to pay a massive premium for a non-yielding asset, even in the face of international conflict. The "January High" of $5,602 now stands as a distant peak, a monument to a period of unprecedented speculation and fear-based buying that has finally met the reality of a high-yield economic environment.

For investors, the key takeaway is that the definition of a "safe haven" is fluid. In 2026, liquidity is king, and the U.S. Dollar remains the ultimate liquid asset. Moving forward, the market will be watching the $4,200 support level closely; a breach there could accelerate the move toward the $3,500 target. Investors should maintain a cautious stance, keeping a close eye on the 10-year Treasury yield and DXY index, as these will be the primary drivers of gold's trajectory in the coming months.

The luster of gold has been temporarily dimmed by the cold reality of mathematical returns. While the metal will always have a place in a diversified portfolio, the "Gilded Age" of 2025 has officially been replaced by the "Yield Age" of 2026. The coming months will determine whether this is a healthy correction in a long-term bull market or the beginning of a prolonged multi-year bear cycle for the world's oldest currency.

This content is intended for informational purposes only and is not financial advice.