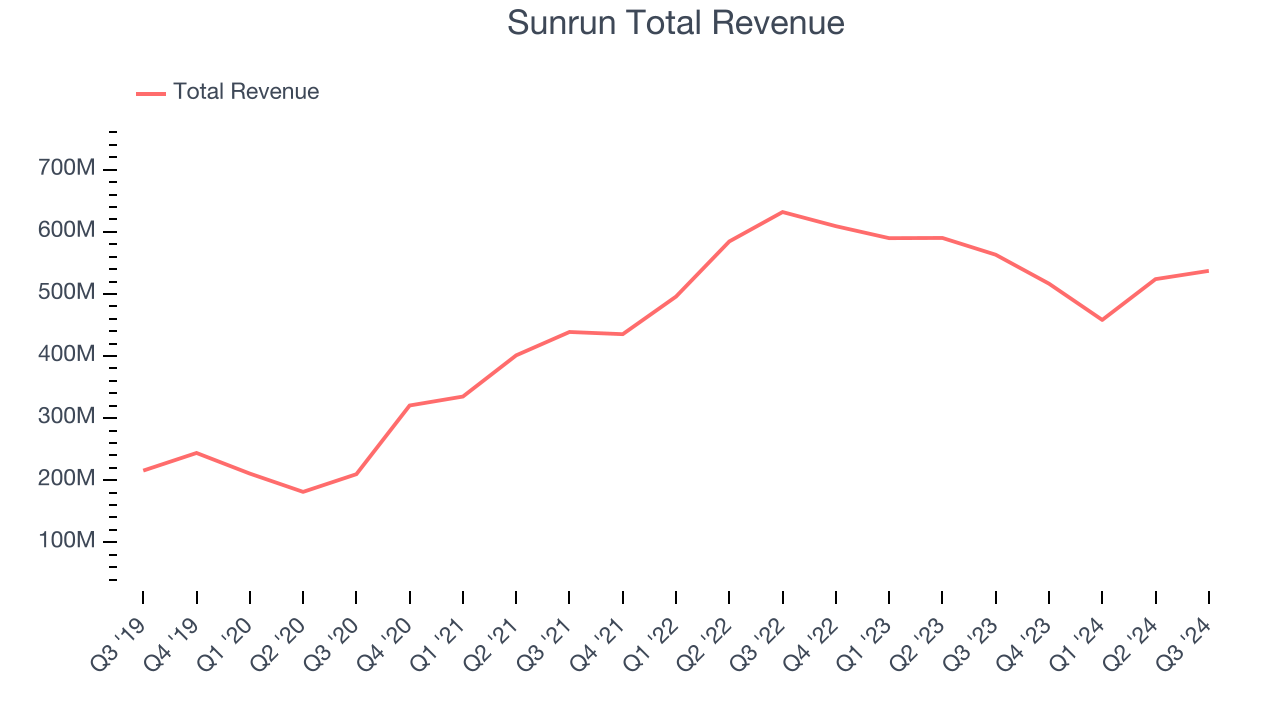

Residential solar energy company Sunrun (NASDAQ: RUN) fell short of the market’s revenue expectations in Q3 CY2024, with sales falling 4.6% year on year to $537.2 million. Its GAAP loss of $0.37 per share was also 111% below analysts’ consensus estimates.

Is now the time to buy Sunrun? Find out by accessing our full research report, it’s free.

Sunrun (RUN) Q3 CY2024 Highlights:

- Revenue: $537.2 million vs analyst estimates of $564.9 million (4.9% miss)

- EPS: -$0.37 vs analyst estimates of -$0.18 (-$0.19 miss)

- EBITDA: $27.75 million vs analyst estimates of $18.17 million (52.7% beat)

- Gross Margin (GAAP): 19.3%, up from 8% in the same quarter last year

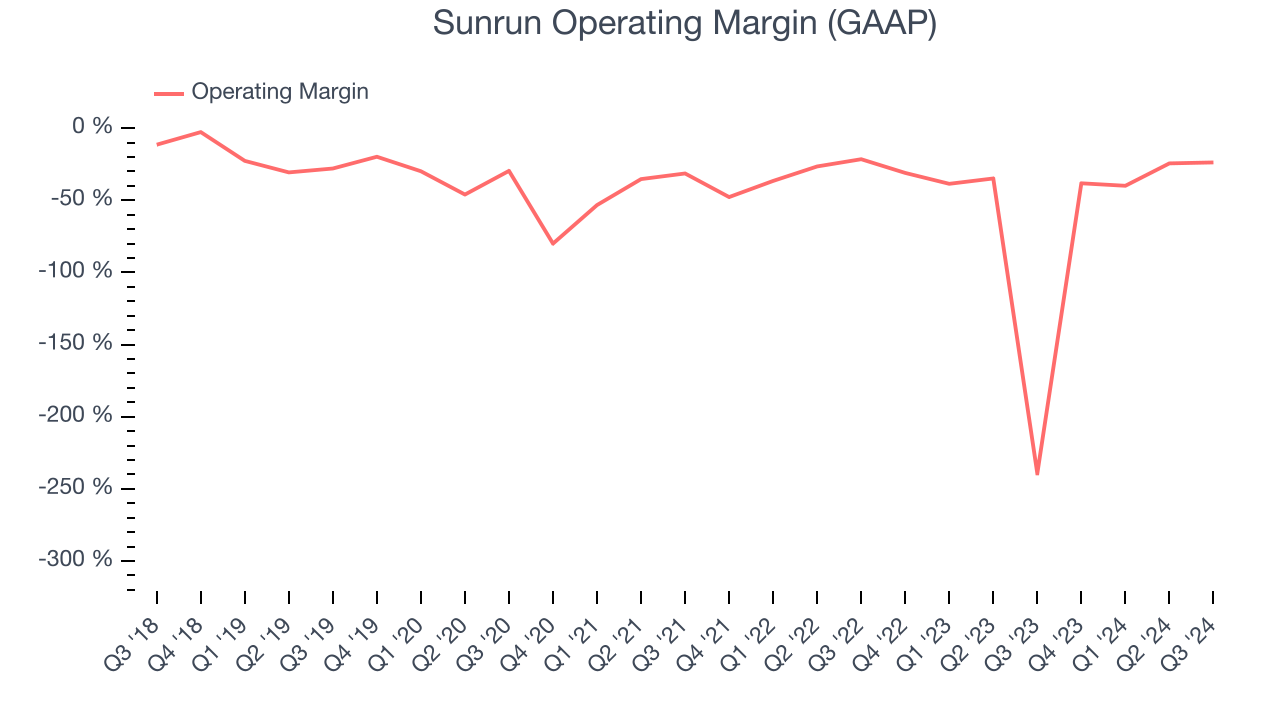

- Operating Margin: -23.8%, up from -239% in the same quarter last year

- EBITDA Margin: 5.2%, up from -215% in the same quarter last year

- Free Cash Flow was -$156.4 million compared to -$67.91 million in the same quarter last year

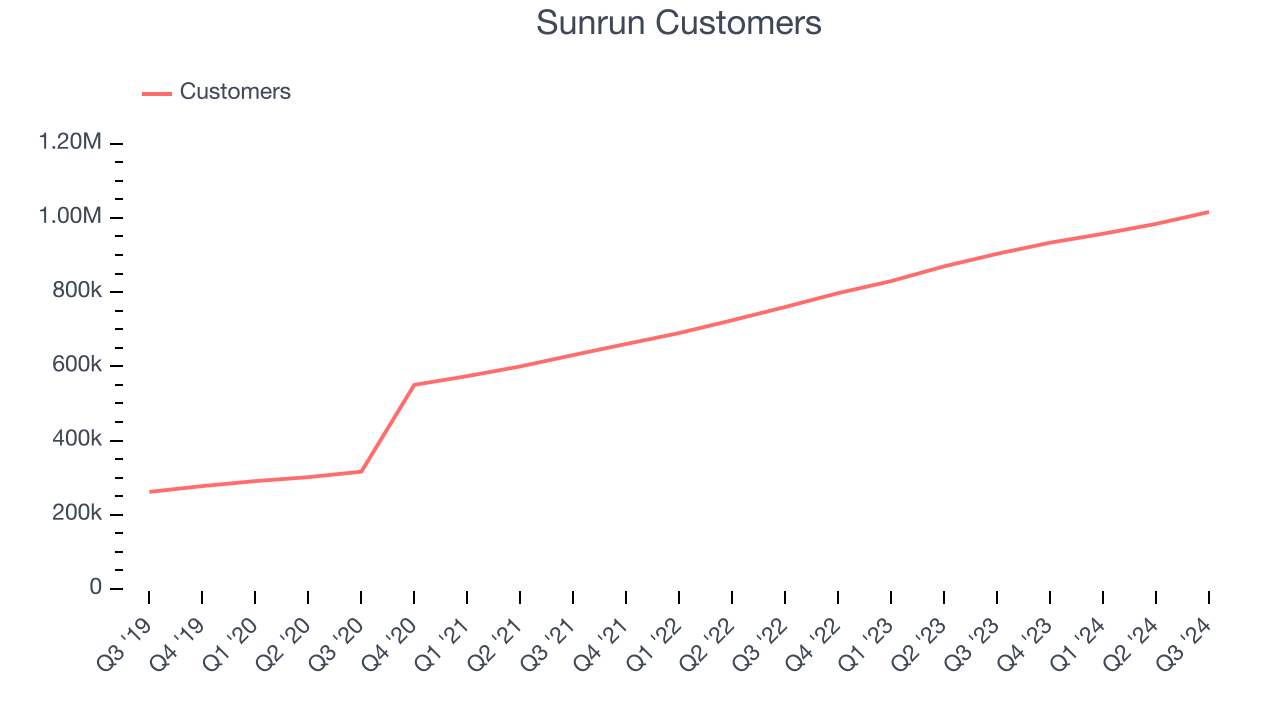

- Customers: 1.02 million, up from 984,000 in the previous quarter

- Market Capitalization: $2.66 billion

“Sunrun’s focus on providing customers with the best experience and differentiated offerings is delivering strong operating and financial results. In the third quarter, we again set new records for both storage installation attachment rates and delivered solid quarter-over-quarter growth for solar installations while reporting higher Net Subscriber Values,” said Mary Powell, Sunrun’s Chief Executive Officer.

Company Overview

Helping homeowners use solar energy to power their homes, Sunrun (NASDAQ: RUN) provides residential solar electricity, specializing in panel installation and leasing services.

Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Sales Growth

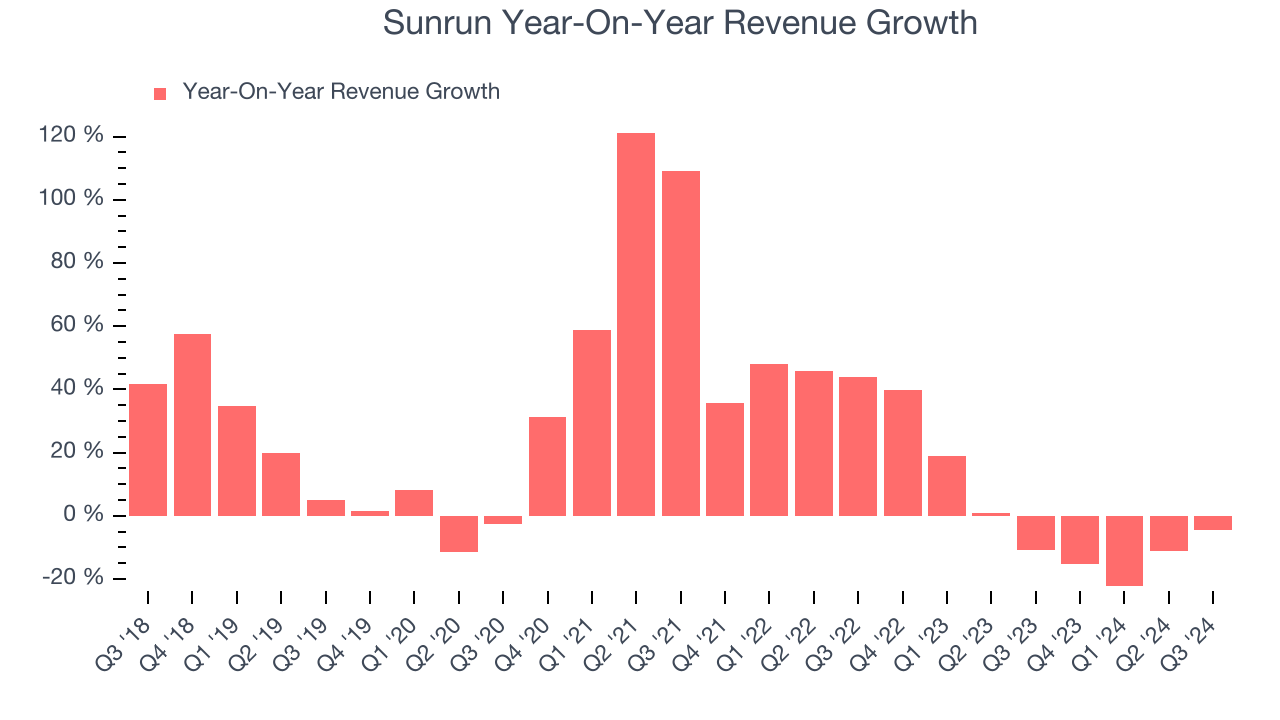

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Sunrun’s 19% annualized revenue growth over the last five years was incredible. This is a useful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Sunrun’s recent history marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 2.6% over the last two years.

Sunrun also reports its number of customers, which reached 1.02 million in the latest quarter. Over the last two years, Sunrun’s customer base averaged 17.3% year-on-year growth. Because this number is better than its revenue growth, we can see the average customer spent less money each year on the company’s products and services.

This quarter, Sunrun missed Wall Street’s estimates and reported a rather uninspiring 4.6% year-on-year revenue decline, generating $537.2 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 16.9% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and indicates the market thinks its newer products and services will fuel higher growth rates.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

Sunrun’s high expenses have contributed to an average operating margin of negative 48% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Sunrun’s annual operating margin might have seen some fluctuations but has generally stayed the same over the last five years, which doesn’t help its cause.

In Q3, Sunrun generated a negative 23.8% operating margin. The company's lacking profits are certainly concerning.

Earnings Per Share

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

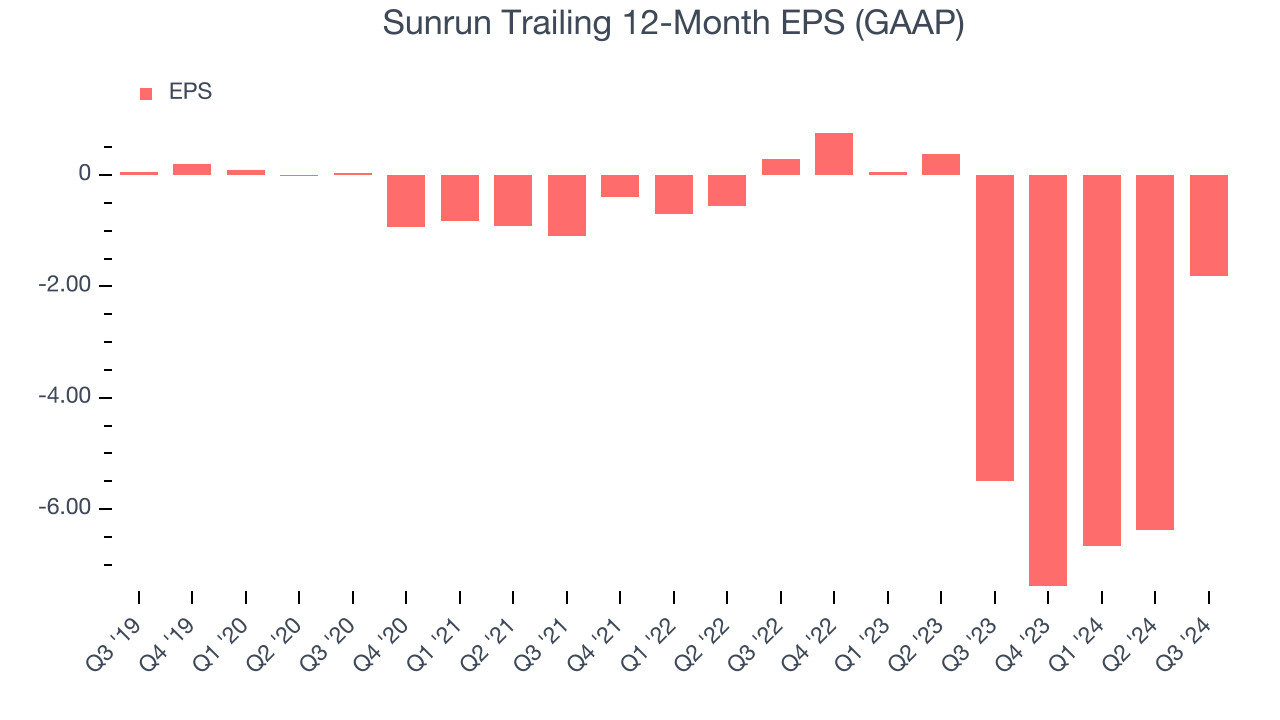

Sadly for Sunrun, its EPS declined by 109% annually over the last five years while its revenue grew by 19%. However, its operating margin didn’t change during this timeframe, telling us that non-fundamental factors affected its ultimate earnings.

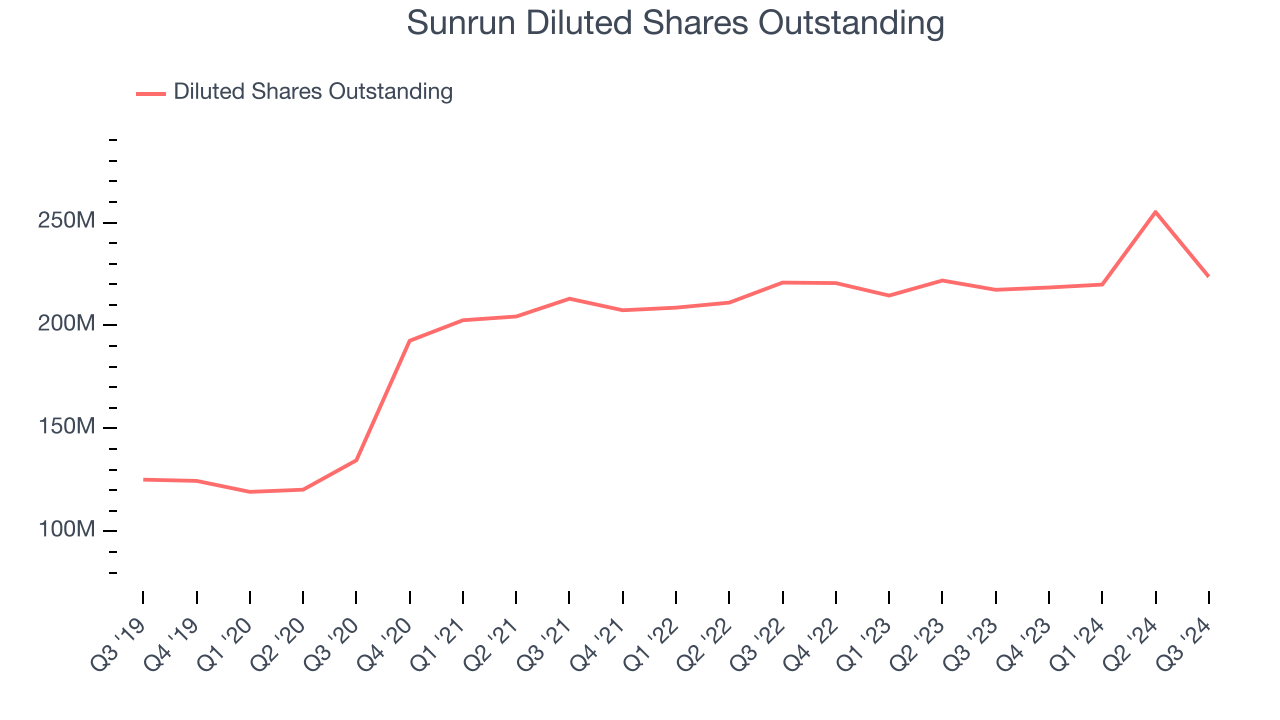

Diving into the nuances of Sunrun’s earnings can give us a better understanding of its performance. A five-year view shows Sunrun has diluted its shareholders, growing its share count by 78.7%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Sunrun, its two-year annual EPS declines of 190% show it’s continued to underperform. These results were bad no matter how you slice the data.In Q3, Sunrun reported EPS at negative $0.37, up from negative $4.92 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Sunrun to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.82 will advance to negative $0.77.

Key Takeaways from Sunrun’s Q3 Results

We were impressed by how significantly Sunrun blew past analysts’ EBITDA expectations this quarter. On the other hand, its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock traded up 4.1% to $12.05 immediately after reporting.

Is Sunrun an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.