Since June 2024, Lyft has been in a holding pattern, floating around $15.57. The stock also fell short of the S&P 500’s 12.1% gain during that period.

Is now the time to buy LYFT? Or does the price properly account for its business quality and fundamentals? Find out in our full research report, it’s free.

Why Does LYFT Stock Spark Debate?

Founded by Logan Green and John Zimmer as a long-distance intercity carpooling company Zimride, Lyft (NASDAQ: LYFT) operates a ridesharing network in the US and Canada.

Two Things to Like:

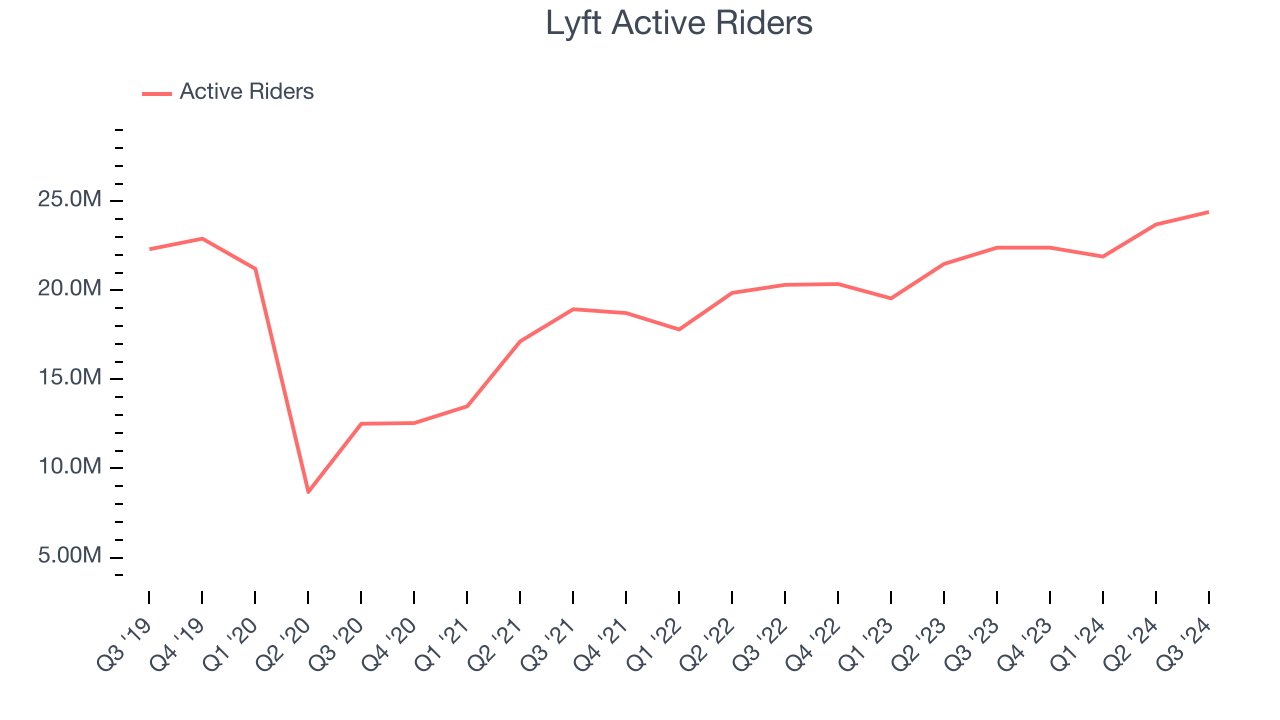

1. Active Riders Drive Additional Growth Opportunities

As a gig economy marketplace, Lyft generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Over the last two years, Lyft’s active riders, a key performance metric for the company, increased by 9.8% annually to 24.4 million in the latest quarter. This growth rate is solid for a consumer internet business and indicates people are excited about its offerings.

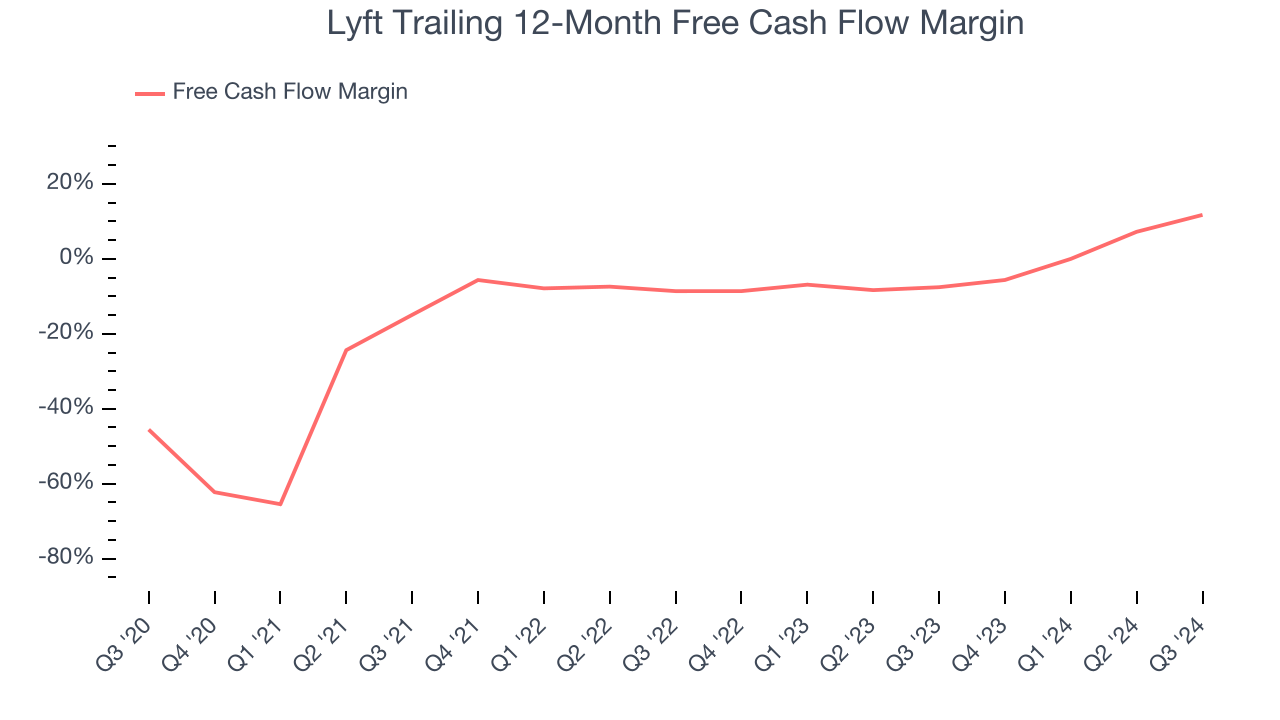

2. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Lyft’s margin expanded by 26.7 percentage points over the last few years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose by more than its operating profitability. Lyft’s free cash flow margin for the trailing 12 months was 11.7%.

One Reason to be Careful:

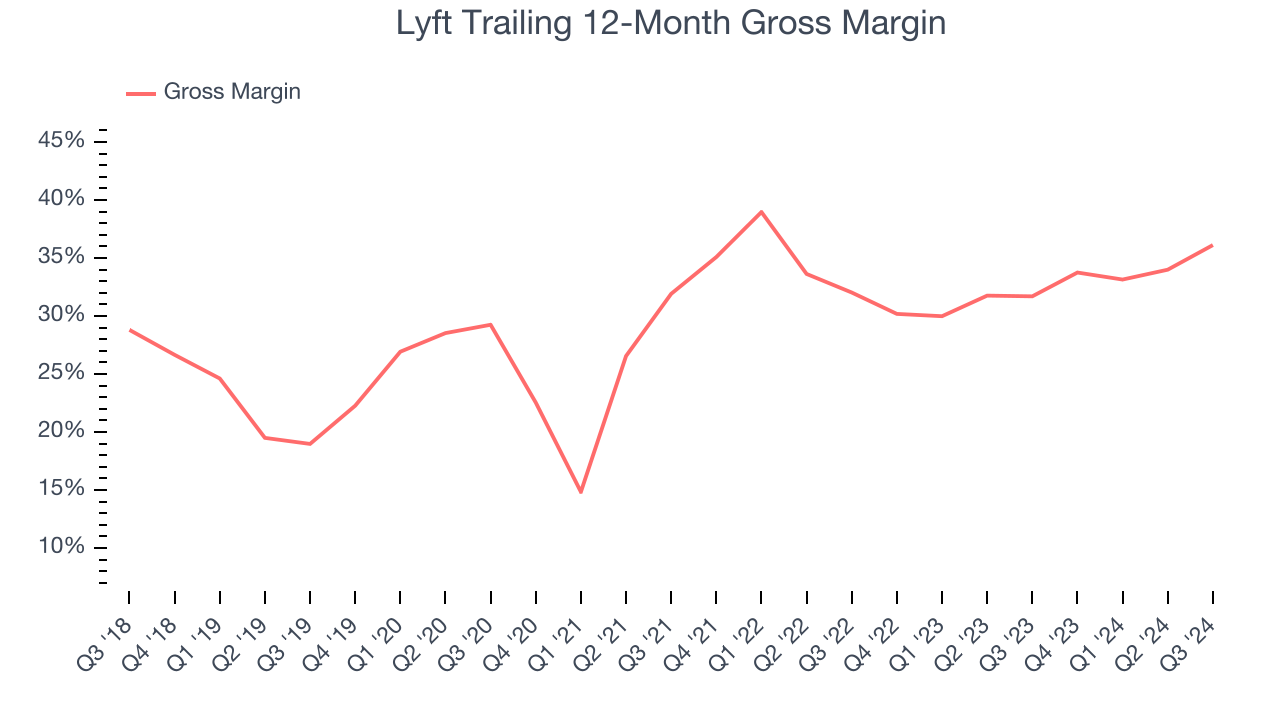

Low Gross Margin Reveals Weak Structural Profitability

For gig economy businesses like Lyft, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include server hosting, customer support, and payment processing fees. Another cost of revenue could also be insurance to protect against liabilities arising from providing transportation, housing, or freelance work services.

Lyft’s unit economics are far below other consumer internet companies, signaling it operates in a competitive market and must pay many third parties a slice of its sales to distribute its products and services. As you can see below, it averaged a 34.2% gross margin over the last two years. That means Lyft paid its providers a lot of money ($65.84 for every $100 in revenue) to run its business.

Final Judgment

Lyft has huge potential even though it has some open questions. With its shares trailing the market in recent months, the stock trades at 14.9× forward EV-to-EBITDA (or $15.57 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Lyft

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.