Accel Entertainment trades at $11.47 per share and has stayed right on track with the overall market, gaining 13.5% over the last six months. At the same time, the S&P 500 has returned 13.5%.

Is now the time to buy Accel Entertainment, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.We don't have much confidence in Accel Entertainment. Here are three reasons why you should be careful with ACEL and a stock we'd rather own.

Why Is Accel Entertainment Not Exciting?

Established in Illinois, Accel Entertainment (NYSE: ACEL) is a provider of electronic gaming machines and interactive amusement terminals to bars and entertainment venues.

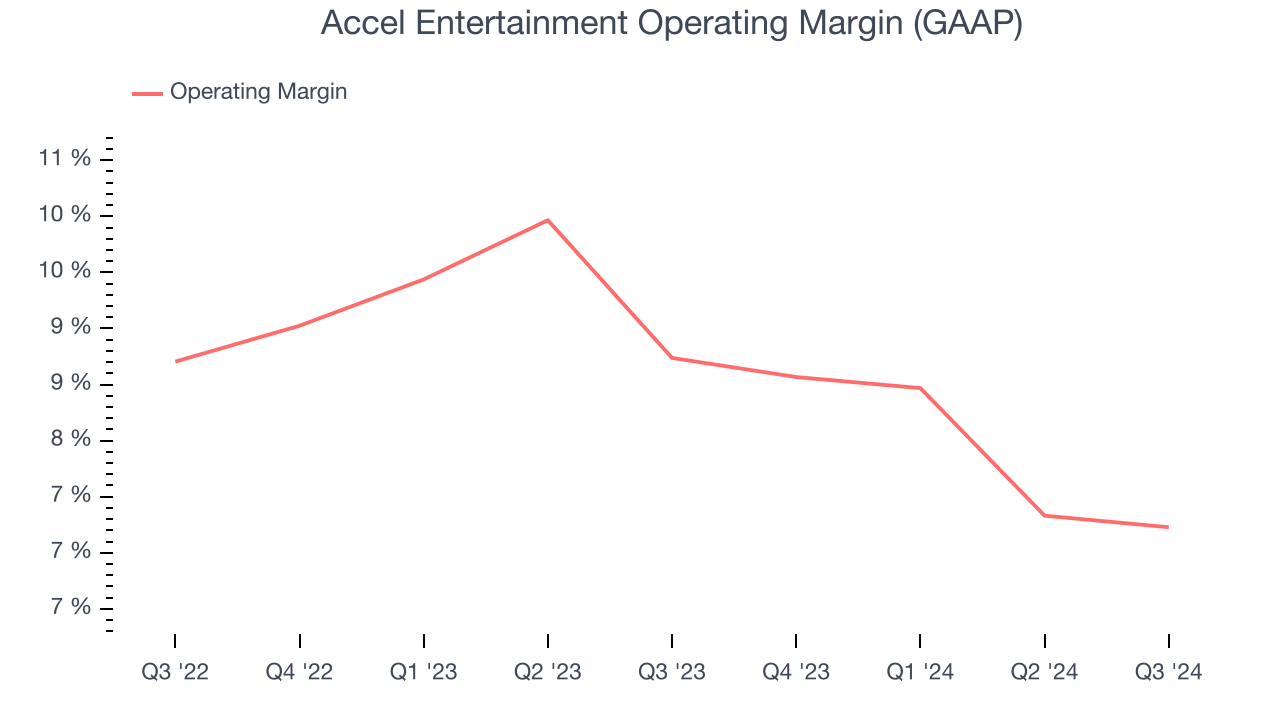

1. Weak Operating Margin Could Cause Trouble

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Accel Entertainment’s operating margin has shrunk over the last 12 months and averaged 8.6% over the last two years. Although this result isn’t good, the company’s top-notch historical revenue growth suggests it ramped up investments to capture market share. We’ll keep a close eye to see if this strategy pays off.

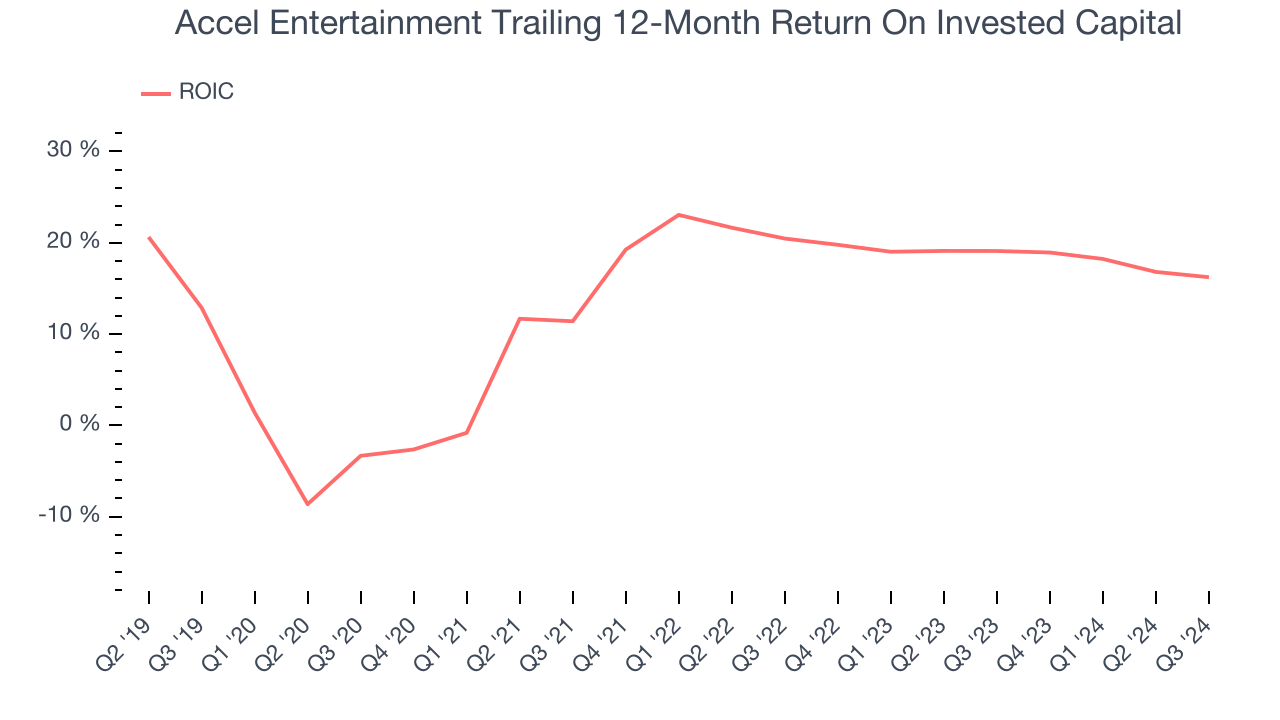

2. Previous Growth Initiatives Haven’t Paid Off Yet

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Accel Entertainment historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 12.8%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

3. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Accel Entertainment’s revenue to rise by 2.9%, a deceleration versus its 17% annualized growth for the past two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

Final Judgment

Accel Entertainment isn’t a terrible business, but it isn’t one of our picks. That said, the stock currently trades at 12.5× forward price-to-earnings (or $11.47 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at Cloudflare, one of our top software picks that could be a home run with edge computing.

Stocks We Like More Than Accel Entertainment

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.