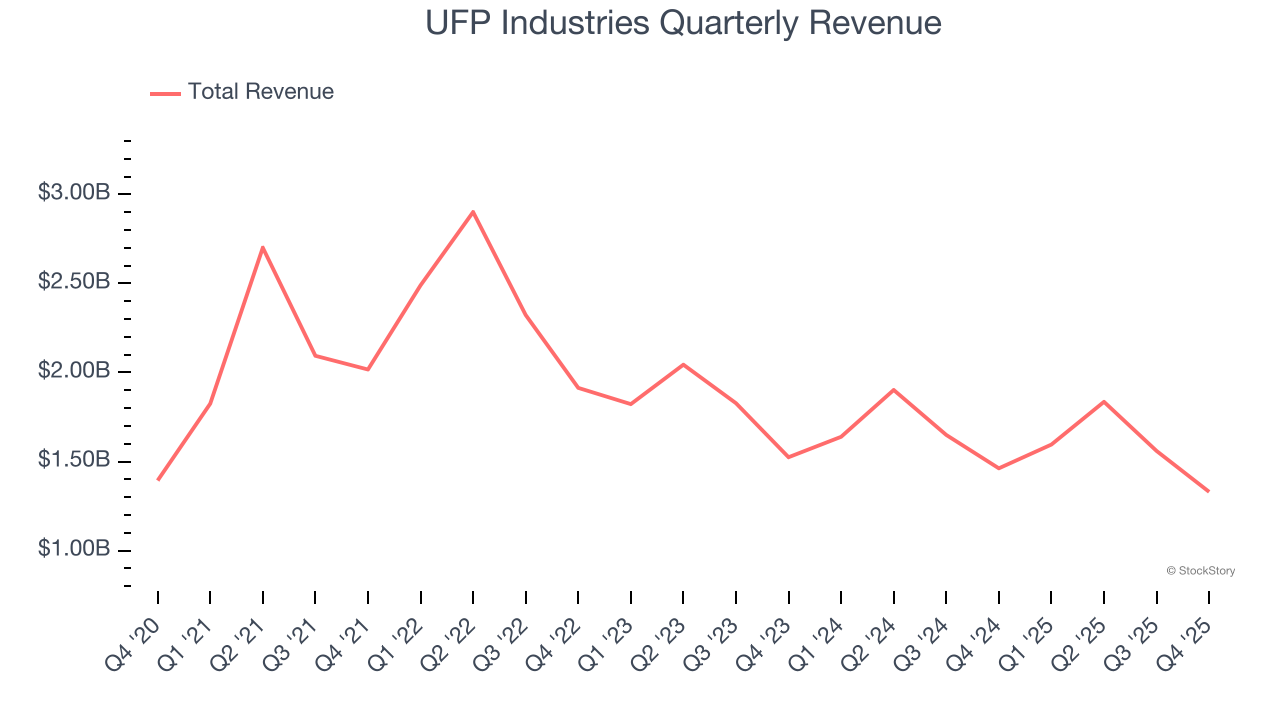

Building materials manufacturer UFP Industries (NASDAQ: UFPI) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 9% year on year to $1.33 billion. Its GAAP profit of $0.70 per share was 34% below analysts’ consensus estimates.

Is now the time to buy UFP Industries? Find out by accessing our full research report, it’s free.

UFP Industries (UFPI) Q4 CY2025 Highlights:

- Revenue: $1.33 billion vs analyst estimates of $1.4 billion (9% year-on-year decline, 5% miss)

- EPS (GAAP): $0.70 vs analyst expectations of $1.06 (34% miss)

- Adjusted EBITDA: $107.2 million vs analyst estimates of $116.8 million (8.1% margin, 8.2% miss)

- Operating Margin: 4.4%, in line with the same quarter last year

- Free Cash Flow Margin: 6.2%, similar to the same quarter last year

- Market Capitalization: $6.39 billion

Will Schwartz, President and CEO of UFP Industries, commented, "We continue to see trends stabilizing across the majority of our businesses. Despite generally soft end-market demand, our fourth quarter sales and profits were in line with internal expectations. While 2025 proved to be a challenging year given market volatility, our team made meaningful progress navigating this environment and executing on our strategy. Our disciplined focus on cost controls and growth investments leaves us on stronger footing and well-positioned as conditions improve. After several years of headwinds, we continue to see markets normalizing and are cautiously optimistic on our business prospects in 2026."

Company Overview

Beginning as a lumber supplier in the 1950s, UFP Industries (NASDAQ: UFPI) is a holding company making building materials for the construction, retail, and industrial sectors.

Revenue Growth

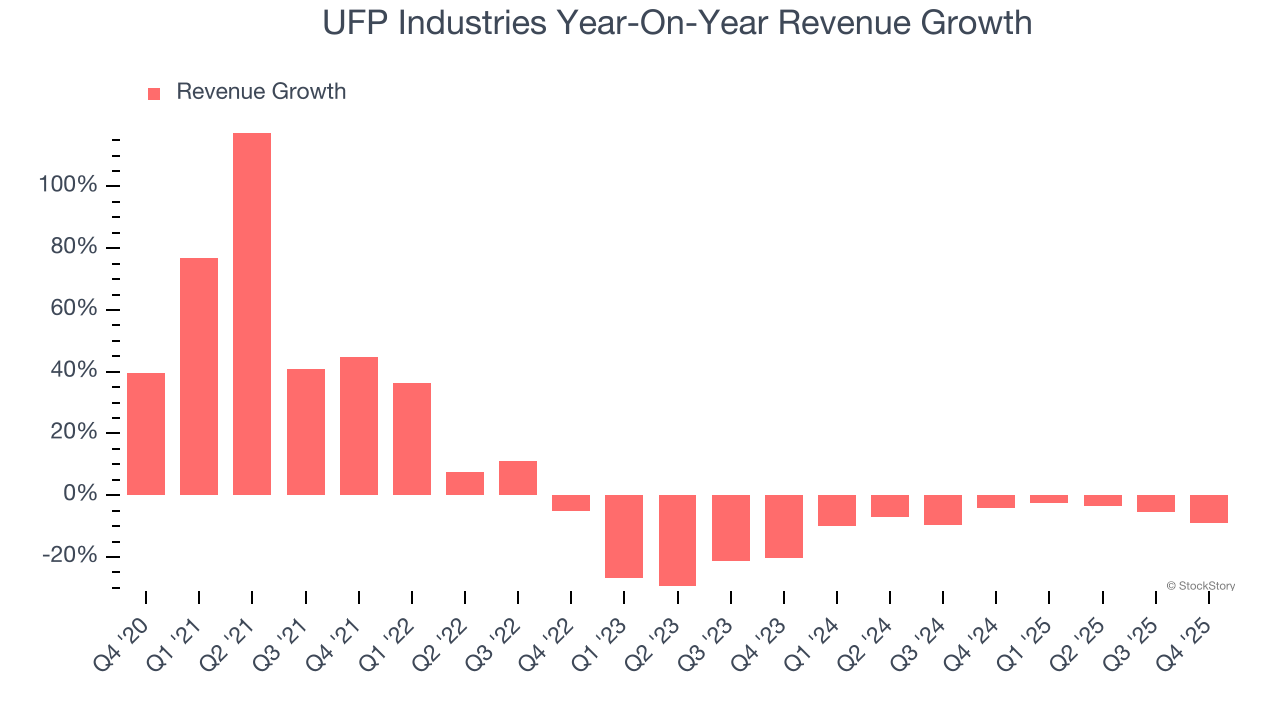

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, UFP Industries’s 4.2% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the industrials sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. UFP Industries’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 6.4% annually.

This quarter, UFP Industries missed Wall Street’s estimates and reported a rather uninspiring 9% year-on-year revenue decline, generating $1.33 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 2.9% over the next 12 months. While this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

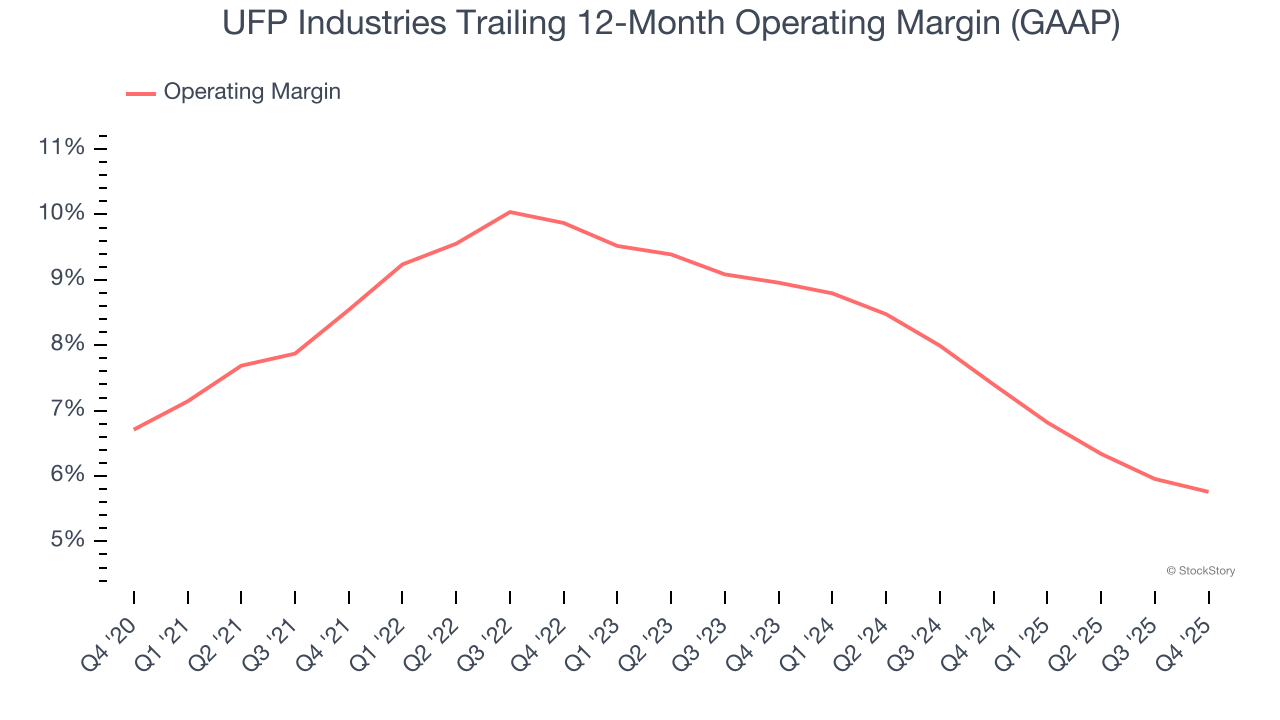

UFP Industries has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.3%, higher than the broader industrials sector.

Analyzing the trend in its profitability, UFP Industries’s operating margin decreased by 2.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, UFP Industries generated an operating margin profit margin of 4.4%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

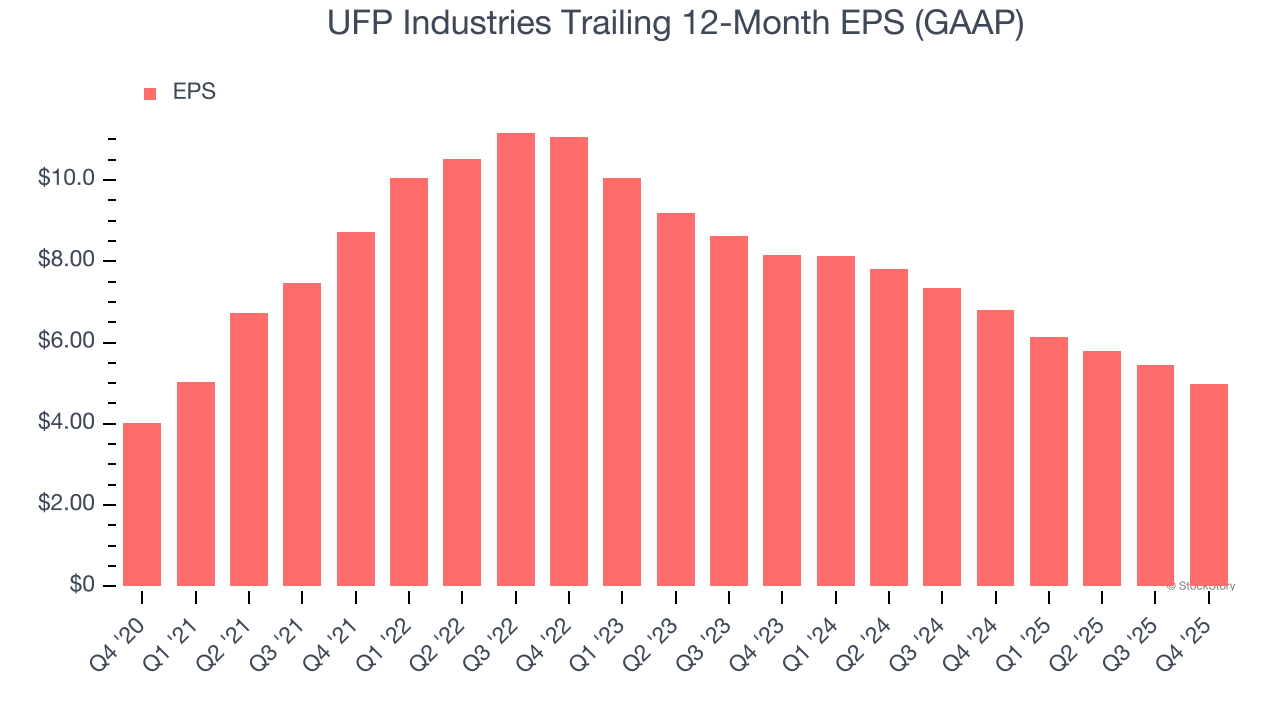

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

UFP Industries’s unimpressive 4.4% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

UFP Industries’s two-year annual EPS declines of 21.9% were bad and lower than its two-year revenue losses.

We can take a deeper look into UFP Industries’s earnings to better understand the drivers of its performance. While we mentioned earlier that UFP Industries’s operating margin was flat this quarter, a two-year view shows its margin has declined. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, UFP Industries reported EPS of $0.70, down from $1.16 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects UFP Industries’s full-year EPS of $4.98 to grow 17.3%.

Key Takeaways from UFP Industries’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $106.27 immediately following the results.

So do we think UFP Industries is an attractive buy at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).