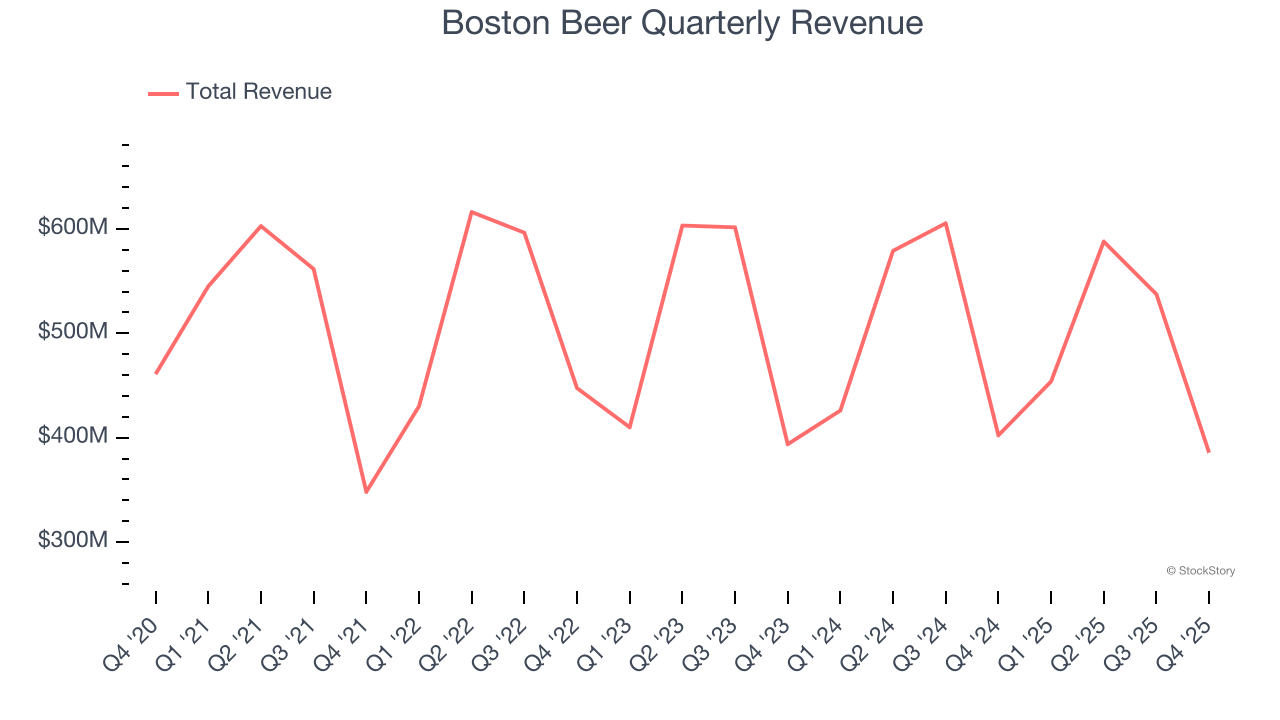

Beer company Boston Beer (NYSE: SAM) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 4.1% year on year to $385.7 million. Its GAAP loss of $2.12 per share was 15.3% above analysts’ consensus estimates.

Is now the time to buy Boston Beer? Find out by accessing our full research report, it’s free.

Boston Beer (SAM) Q4 CY2025 Highlights:

- Revenue: $385.7 million vs analyst estimates of $386.3 million (4.1% year-on-year decline, in line)

- EPS (GAAP): -$2.12 vs analyst estimates of -$2.50 (15.3% beat)

- Operating Margin: -8.6%, up from -13.9% in the same quarter last year

- Market Capitalization: $2.34 billion

“We were pleased to deliver on our financial commitments in 2025 while maintaining market share in a challenging operating environment,” said Chairman, Founder and CEO Jim Koch.

Company Overview

Known for its flavorful beverages challenging the status quo, Boston Beer (NYSE: SAM) is a pioneer in craft brewing and a symbol of American innovation in the alcoholic beverage industry.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.96 billion in revenue over the past 12 months, Boston Beer is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Boston Beer’s revenue declined by 2% per year over the last three years, a tough starting point for our analysis.

This quarter, Boston Beer reported a rather uninspiring 4.1% year-on-year revenue decline to $385.7 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection indicates its newer products will fuel better top-line performance, it is still below average for the sector.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

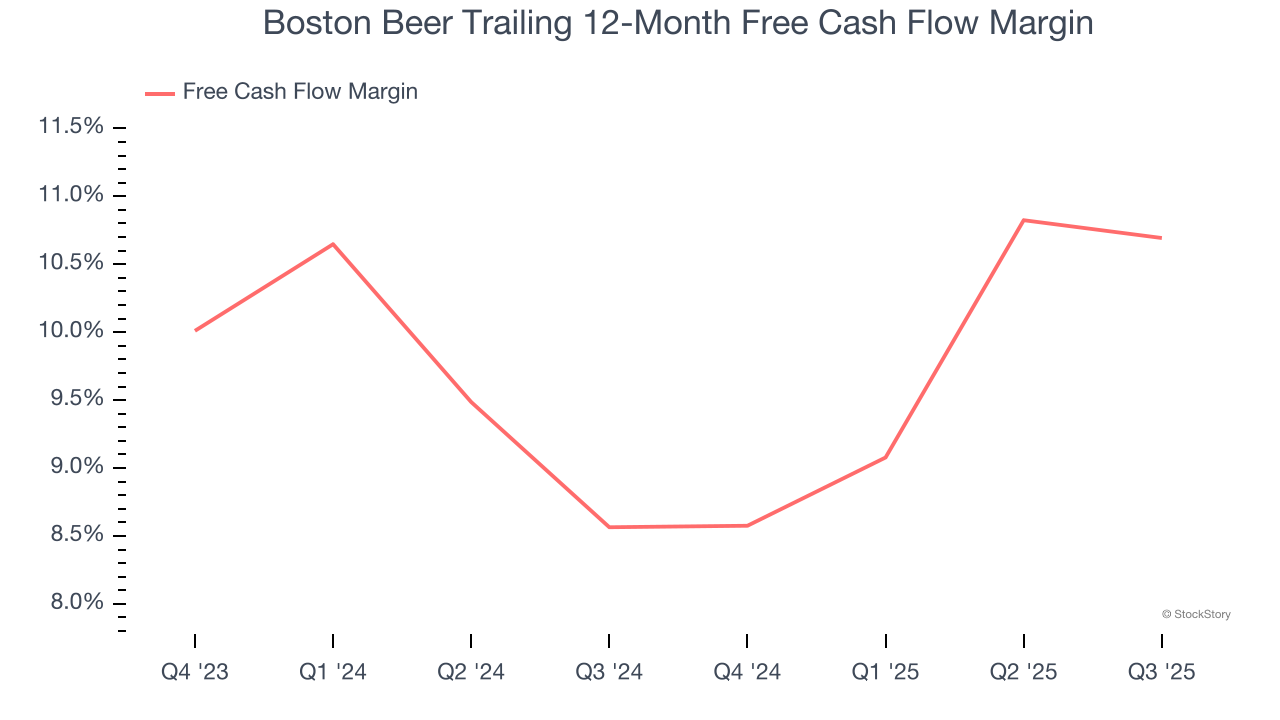

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Boston Beer has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.2% over the last two years, quite impressive for a consumer staples business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Key Takeaways from Boston Beer’s Q4 Results

We enjoyed seeing Boston Beer beat analysts’ gross margin expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $227.46 immediately following the results.

Is Boston Beer an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).