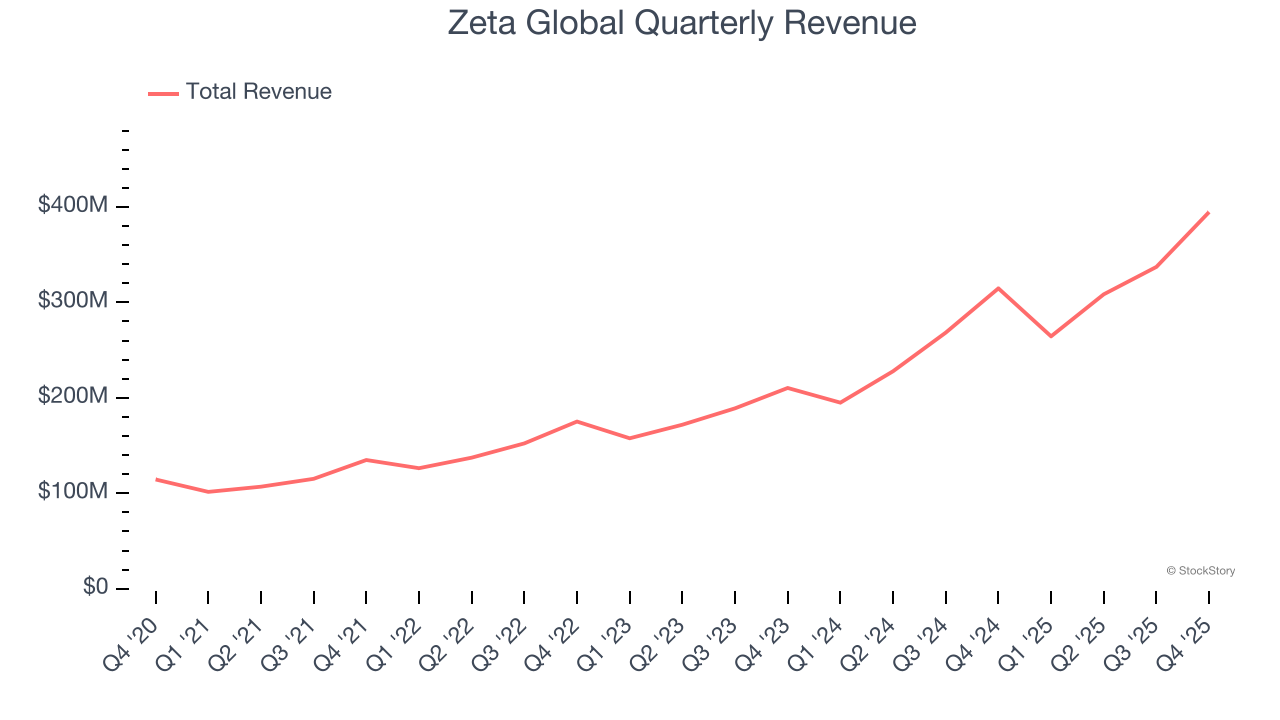

Marketing technology company Zeta Global (NYSE: ZETA) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 25.4% year on year to $394.6 million. Guidance for next quarter’s revenue was optimistic at $370 million at the midpoint, 2.1% above analysts’ estimates.

Is now the time to buy Zeta Global? Find out by accessing our full research report, it’s free.

Zeta Global (ZETA) Q4 CY2025 Highlights:

- Revenue: $394.6 million vs analyst estimates of $380.6 million (25.4% year-on-year growth, 3.7% beat)

- Adjusted EBITDA: $95.13 million vs analyst estimates of $91.17 million (24.1% margin, 4.3% beat)

- Revenue Guidance for Q1 CY2026 is $370 million at the midpoint, above analyst estimates of $362.3 million

- EBITDA guidance for the upcoming financial year 2026 is $391 million at the midpoint, above analyst estimates of $382.8 million

- Operating Margin: 4.5%, up from 2.2% in the same quarter last year

- Free Cash Flow Margin: 14.2%, similar to the previous quarter

- Market Capitalization: $3.68 billion

Company Overview

Powered by an AI engine that processes over one trillion consumer signals monthly, Zeta Global (NYSE: ZETA) operates a data-driven cloud platform that helps companies target, connect, and engage with consumers through personalized marketing across channels like email, social media, and video.

Revenue Growth

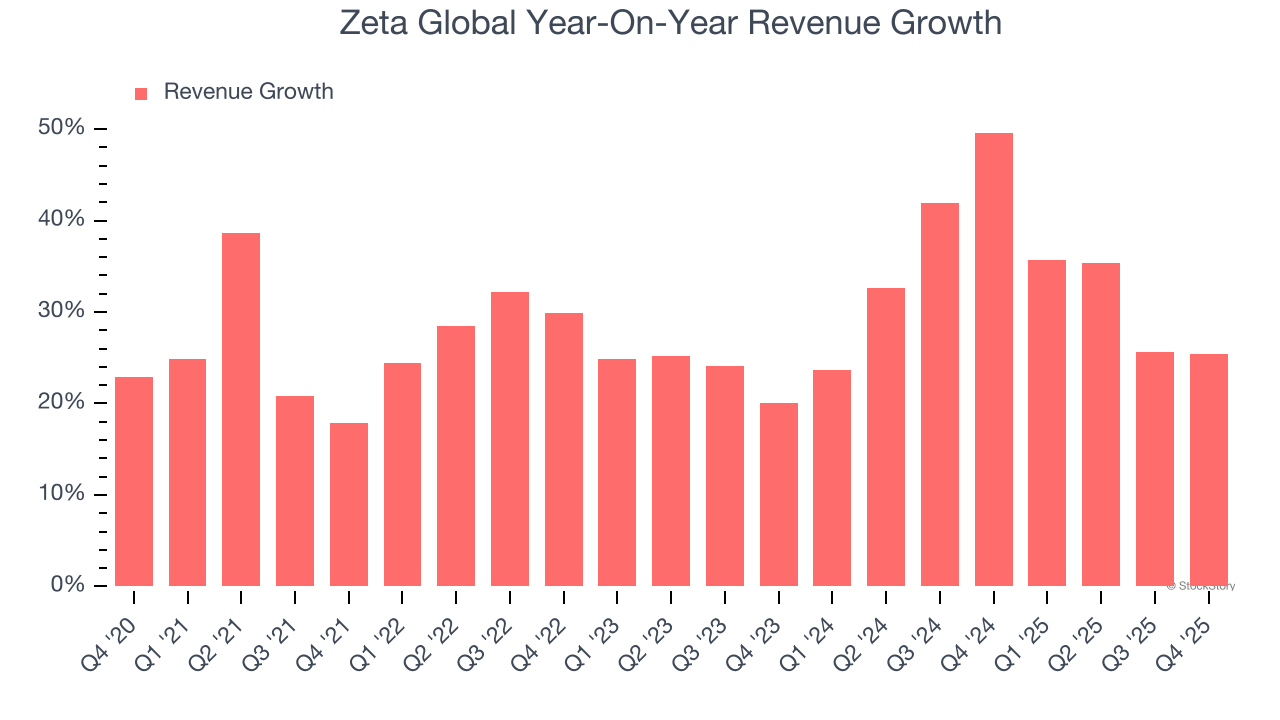

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Zeta Global’s 28.8% annualized revenue growth over the last five years was impressive. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Zeta Global’s annualized revenue growth of 33.8% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Zeta Global reported robust year-on-year revenue growth of 25.4%, and its $394.6 million of revenue topped Wall Street estimates by 3.7%. Company management is currently guiding for a 39.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 32.6% over the next 12 months, similar to its two-year rate. Still, this projection is noteworthy and indicates the market is baking in success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Zeta Global is extremely efficient at acquiring new customers, and its CAC payback period checked in at 5.6 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Zeta Global more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Key Takeaways from Zeta Global’s Q4 Results

It was great to see Zeta Global expecting revenue growth to accelerate next year. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 1.5% to $17.20 immediately following the results.

Zeta Global had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).