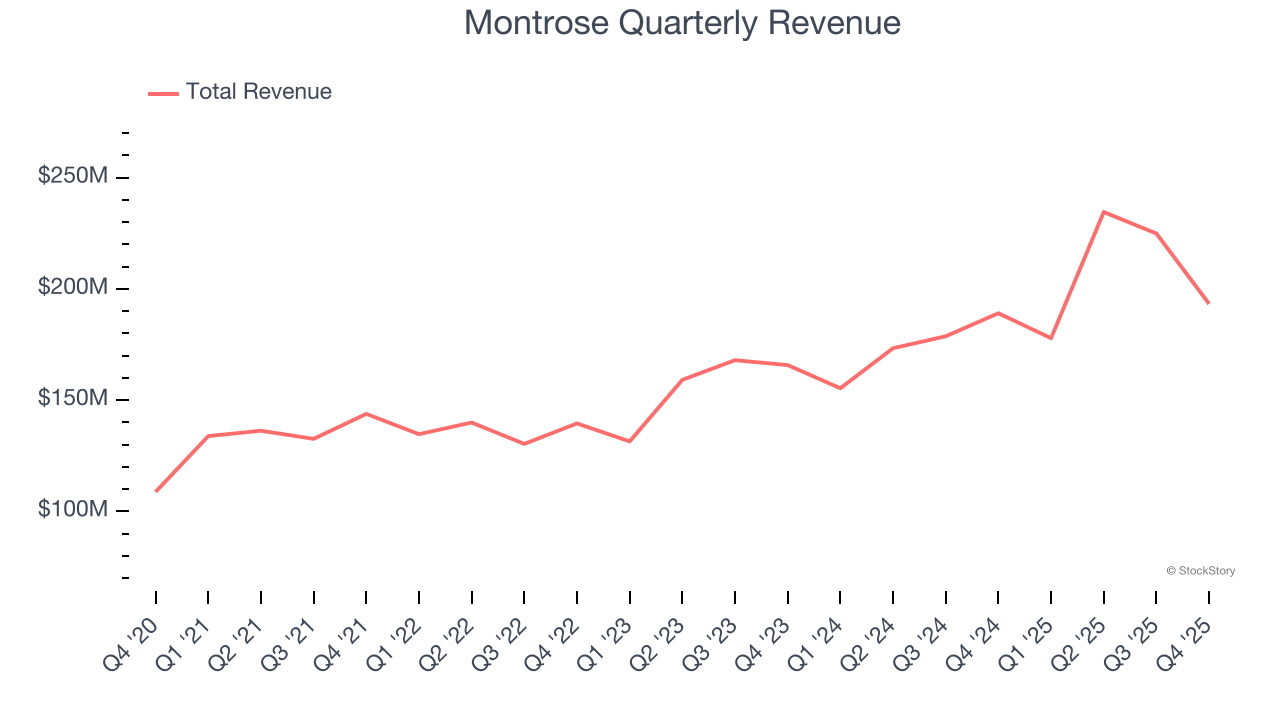

Environmental services provider Montrose (NYSE: MEG) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 2.2% year on year to $193.3 million. The company’s full-year revenue guidance of $870 million at the midpoint came in 2.6% above analysts’ estimates. Its non-GAAP profit of $0.35 per share was 84.4% above analysts’ consensus estimates.

Is now the time to buy Montrose? Find out by accessing our full research report, it’s free.

Montrose (MEG) Q4 CY2025 Highlights:

- Revenue: $193.3 million vs analyst estimates of $188.6 million (2.2% year-on-year growth, 2.5% beat)

- Adjusted EPS: $0.35 vs analyst estimates of $0.19 (84.4% beat)

- Adjusted EBITDA: $23.89 million vs analyst estimates of $23.23 million (12.4% margin, 2.8% beat)

- EBITDA guidance for the upcoming financial year 2026 is $127.5 million at the midpoint, above analyst estimates of $125.7 million

- Operating Margin: -1.3%, up from -12.1% in the same quarter last year

- Free Cash Flow Margin: 23.7%, up from 15.7% in the same quarter last year

- Market Capitalization: $799.3 million

Montrose Chief Executive Officer and Director, Vijay Manthripragada, commented, “Over a year ago, we announced a pause in acquisitions to highlight the quality and durability of our business. We also shared our expectation that US regulatory volatility would create more tailwinds than headwinds given our unique business model and global client focus. As we reflect on our focused execution in 2025, our business outperformed and exceeded every major objective. We delivered 13% organic revenue growth, expanded EBITDA margins, and generated record cash flow with 75% Free cash flow1 conversion. Our cash flow generation outperformance resulted in 2025 year-end leverage approximately 0.5x lower than our forecast at the start of 2025. We also accelerated cross-selling across our platform, expanded our IP portfolio, and attracted incredible talent, all of which position us very well for 2026 and beyond."

Company Overview

Founded to protect a tree-lined two-lane road, Montrose (NYSE: MEG) provides air quality monitoring, environmental laboratory testing, compliance, and environmental consulting services.

Revenue Growth

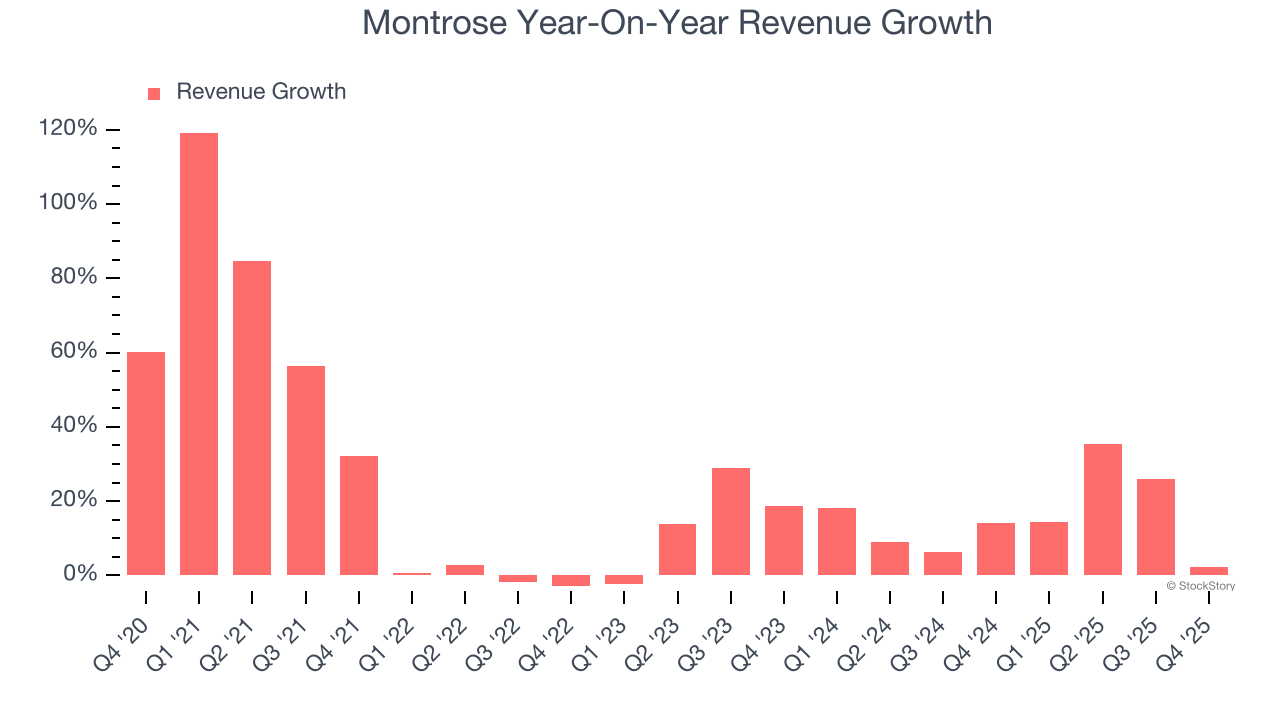

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Montrose’s sales grew at an incredible 20.4% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Montrose’s annualized revenue growth of 15.3% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Montrose reported modest year-on-year revenue growth of 2.2% but beat Wall Street’s estimates by 2.5%.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

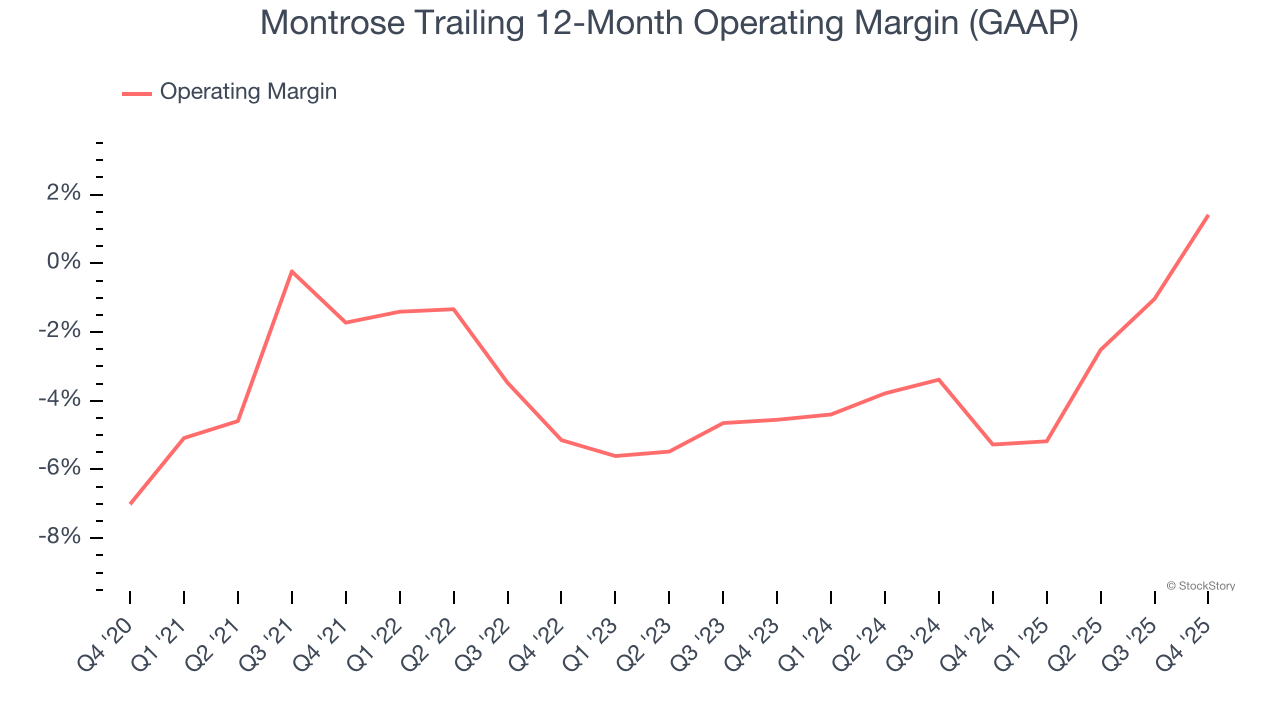

Montrose’s high expenses have contributed to an average operating margin of negative 2.8% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Montrose’s operating margin rose by 3.1 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

Montrose’s operating margin was negative 1.3% this quarter.

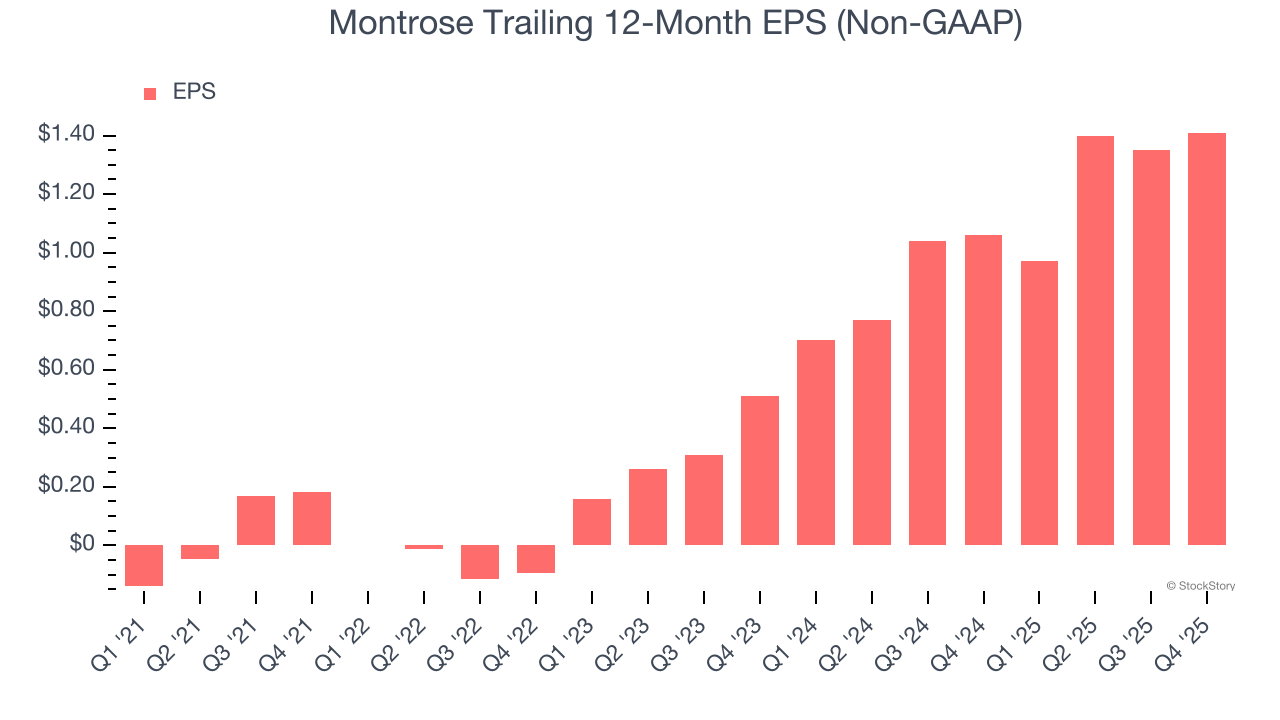

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Montrose’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Montrose’s EPS grew at an astounding 66.3% compounded annual growth rate over the last two years, higher than its 15.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into Montrose’s quality of earnings can give us a better understanding of its performance. Montrose’s operating margin has expanded over the last two years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Montrose reported adjusted EPS of $0.35, up from $0.29 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Montrose’s full-year EPS of $1.41 to grow 2%.

Key Takeaways from Montrose’s Q4 Results

It was good to see Montrose beat analysts’ EPS expectations this quarter. We were also glad its full-year revenue guidance exceeded Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 7.5% to $25.10 immediately after reporting.

Indeed, Montrose had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).