ICU Medical has been treading water for the past six months, recording a small return of 2.8% while holding steady at $120.94.

Is now the time to buy ICU Medical, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is ICU Medical Not Exciting?

We don't have much confidence in ICU Medical. Here are three reasons you should be careful with ICUI and a stock we'd rather own.

1. Revenue Growth Flatlining

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. ICU Medical’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect ICU Medical’s revenue to drop by 1.9%, a decrease from its 12.4% annualized growth for the past five years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

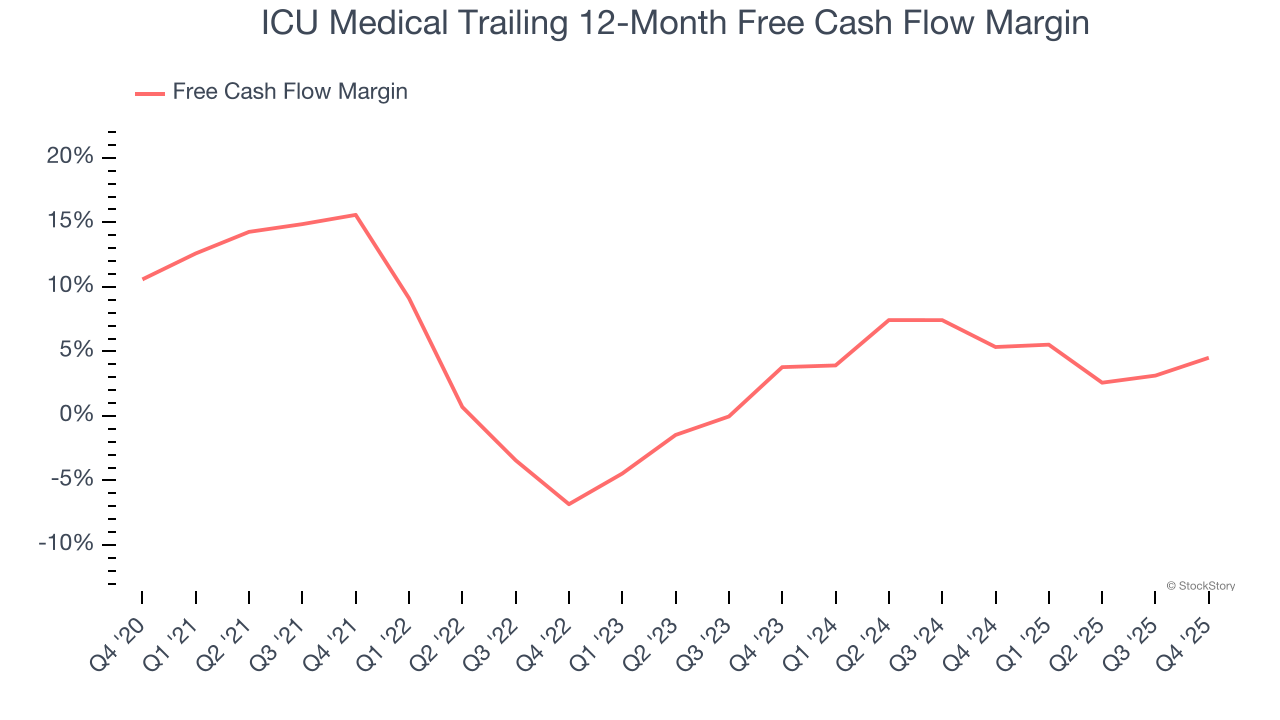

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, ICU Medical’s margin dropped by 11.1 percentage points over the last five years. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s becoming a more capital-intensive business. ICU Medical’s free cash flow margin for the trailing 12 months was 4.5%.

Final Judgment

ICU Medical isn’t a terrible business, but it isn’t one of our picks. That said, the stock currently trades at 15.2× forward P/E (or $120.94 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than ICU Medical

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.