JPMorgan Chase currently trades at $311.75 per share and has shown little upside over the past six months, posting a middling return of 2%.

Is now the time to buy JPMorgan Chase, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is JPMorgan Chase Not Exciting?

We don't have much confidence in JPMorgan Chase. Here are three reasons you should be careful with JPM and a stock we'd rather own.

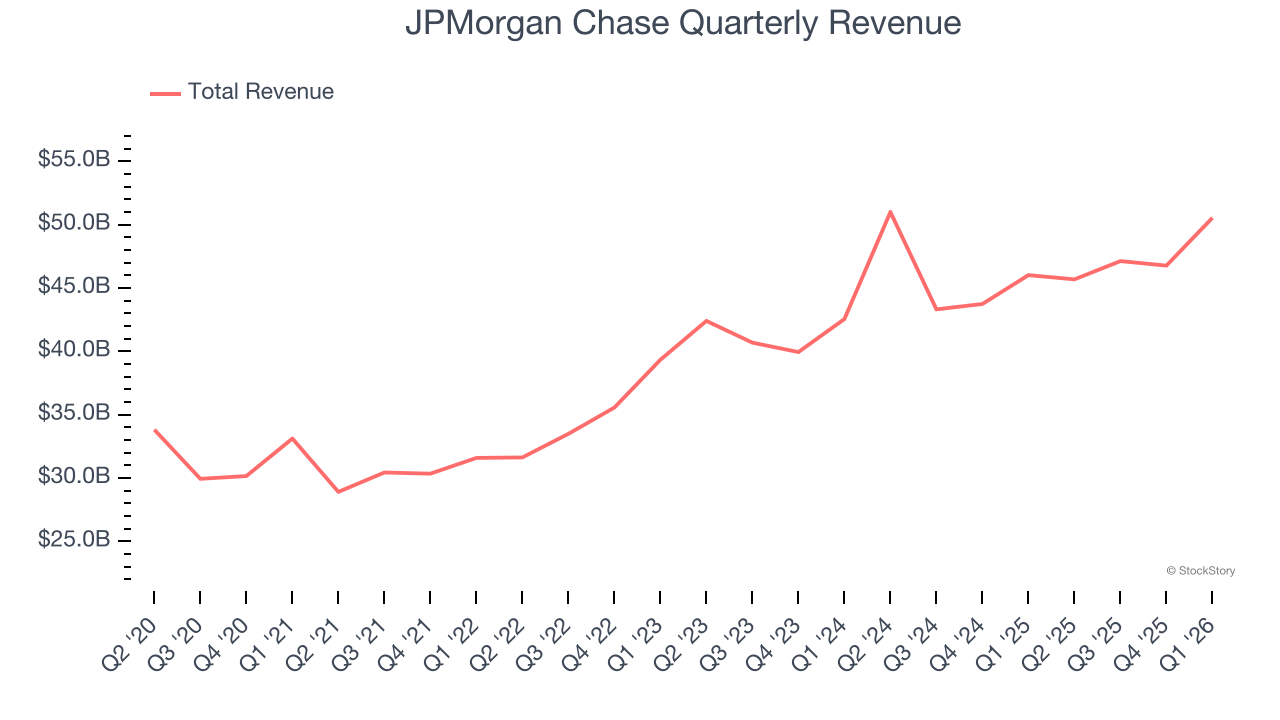

1. Long-Term Revenue Growth Disappoints

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees.

Over the last five years, JPMorgan Chase grew its revenue at a mediocre 8.4% compounded annual growth rate. This was below our standard for the banking sector.

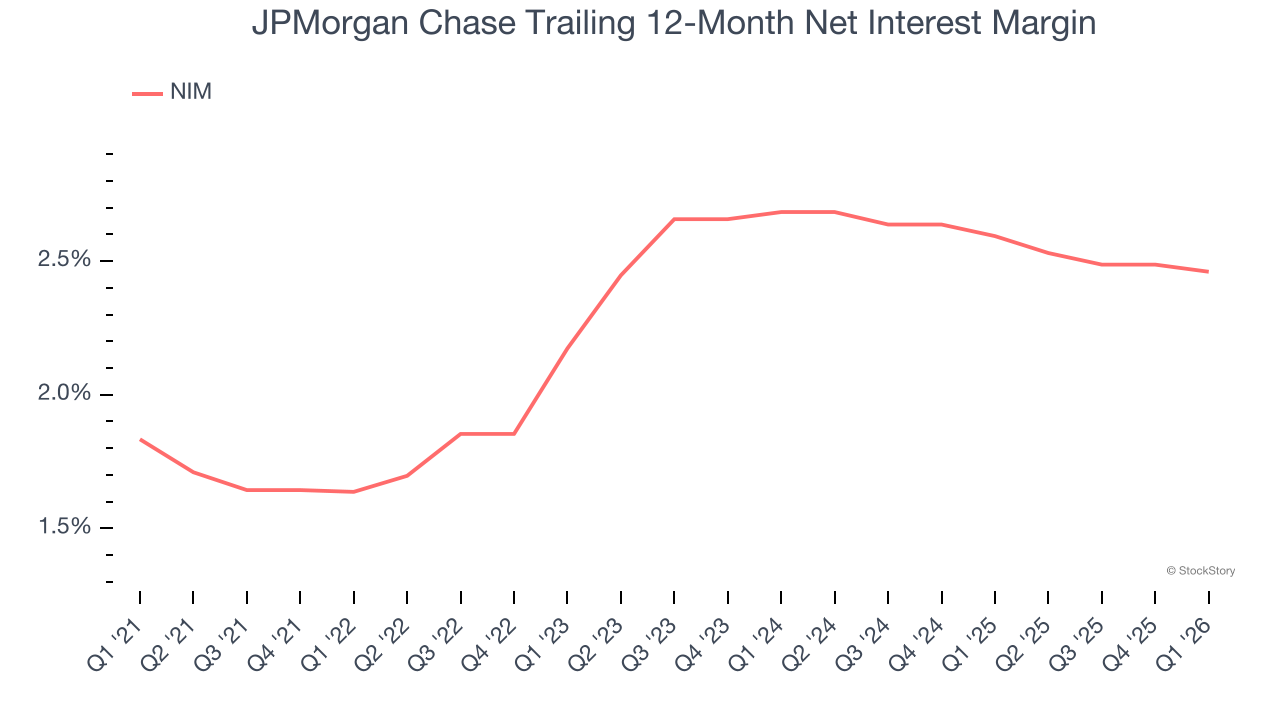

2. Low Net Interest Margin Reveals Weak Loan Book Profitability

Net interest margin (NIM) represents the unit economics of a bank by measuring the profitability of its interest-bearing assets relative to its interest-bearing liabilities. It's a fundamental metric that investors use to assess lending premiums and returns.

Over the past two years, we can see that JPMorgan Chase’s net interest margin averaged a poor 2.5%. This metric is well below other banks, signaling its loans aren’t very profitable.

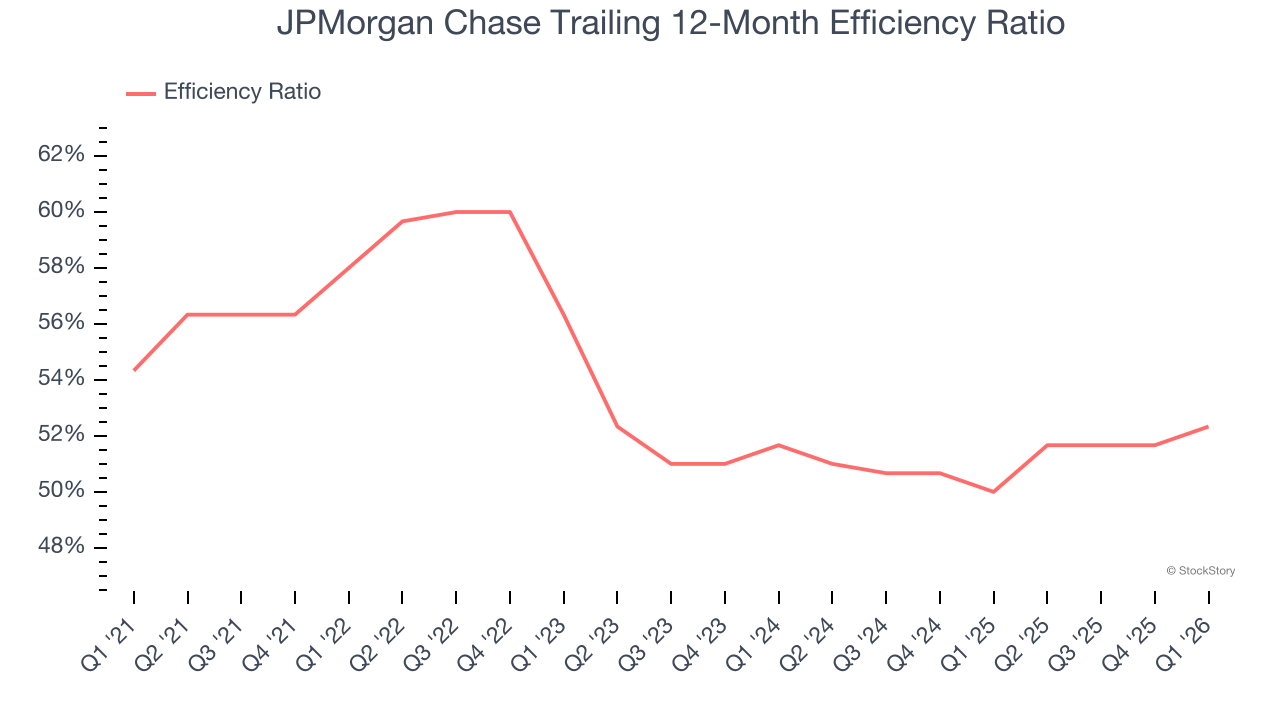

3. Efficiency Ratio Expected to Falter

Topline growth alone doesn't tell the complete story - the profitability of that growth shapes actual earnings impact. Banks track this dynamic through efficiency ratios, which compare non-interest expenses such as personnel, rent, IT, and marketing costs to total revenue streams.

Investors place greater emphasis on efficiency ratio movements than absolute values, understanding that expense structures reflect revenue mix variations. Lower ratios represent better operational performance since they show banks generating more revenue per dollar of expense.

For the next 12 months, Wall Street expects JPMorgan Chase to become less profitable as it anticipates an efficiency ratio of 54.1% compared to 52.3% over the past year.

Final Judgment

JPMorgan Chase’s business quality ultimately falls short of our standards. That said, the stock currently trades at 2.3× forward P/B (or $311.75 per share). This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere. Let us point you toward an all-weather company that owns household favorite Taco Bell.

Stocks We Would Buy Instead of JPMorgan Chase

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.