Behavioral health company Acadia Healthcare (NASDAQ: ACHC) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 7.6% year on year to $828.8 million. On the other hand, next quarter’s revenue guidance of $842.5 million was less impressive, coming in 2.7% below analysts’ estimates. Its non-GAAP profit of $0.37 per share was 39.7% above analysts’ consensus estimates.

Is now the time to buy Acadia Healthcare? Find out by accessing our full research report, it’s free.

Acadia Healthcare (ACHC) Q1 CY2026 Highlights:

- Revenue: $828.8 million vs analyst estimates of $823.5 million (7.6% year-on-year growth, 0.6% beat)

- Adjusted EPS: $0.37 vs analyst estimates of $0.26 (39.7% beat)

- Adjusted EBITDA: $199.5 million vs analyst estimates of $131.3 million (24.1% margin, 51.9% beat)

- The company reconfirmed its revenue guidance for the full year of $3.41 billion at the midpoint

- Management raised its full-year Adjusted EPS guidance to $1.48 at the midpoint, a 3.5% increase

- EBITDA guidance for the full year is $597.5 million at the midpoint, above analyst estimates of $587.6 million

- Operating Margin: 1.3%, down from 5.5% in the same quarter last year

- Free Cash Flow was -$15.03 million compared to -$163.2 million in the same quarter last year

- Sales Volumes rose 7.1% year on year (-1.1% in the same quarter last year)

- Market Capitalization: $2.54 billion

“The good start to the year reflects disciplined execution throughout Acadia as we provide quality care for individuals seeking treatment for mental health and substance abuse issues,” said Debbie Osteen, Chief Executive Officer of Acadia.

Company Overview

With a network of over 250 facilities serving patients in 38 states and Puerto Rico, Acadia Healthcare (NASDAQ: ACHC) operates facilities providing mental health and substance use disorder treatment services across the United States.

Revenue Growth

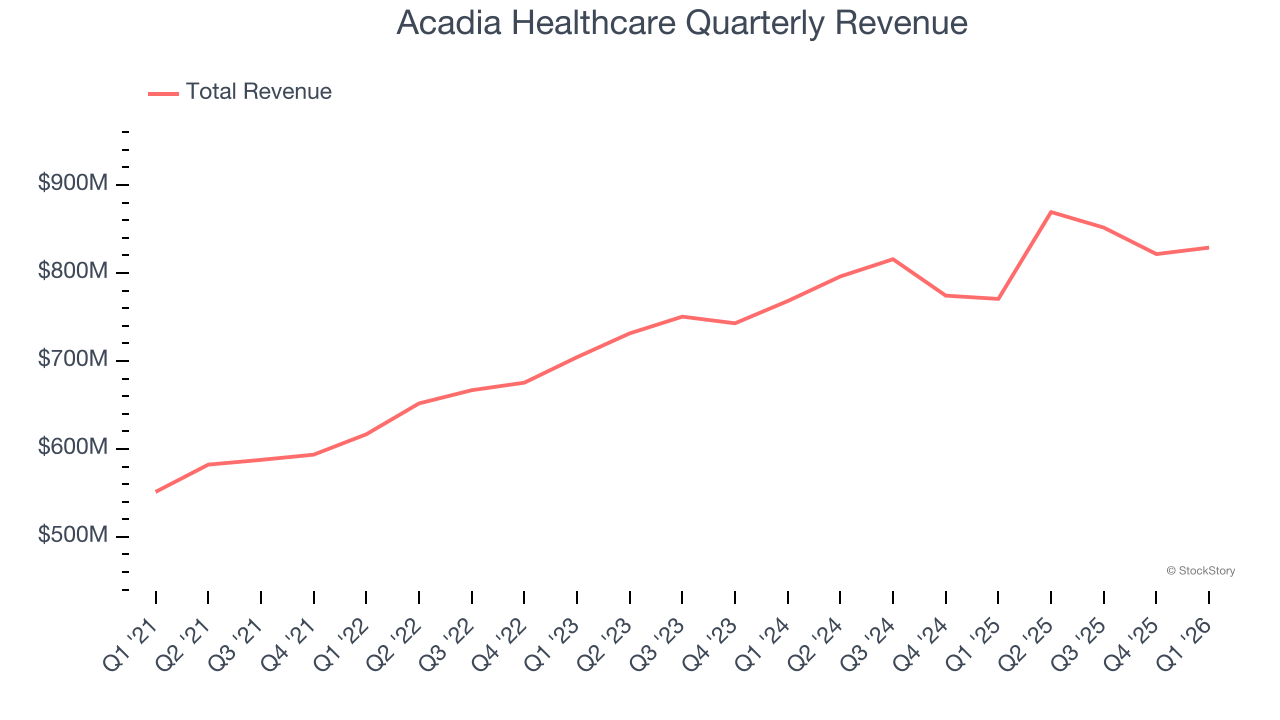

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Acadia Healthcare’s 9.6% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

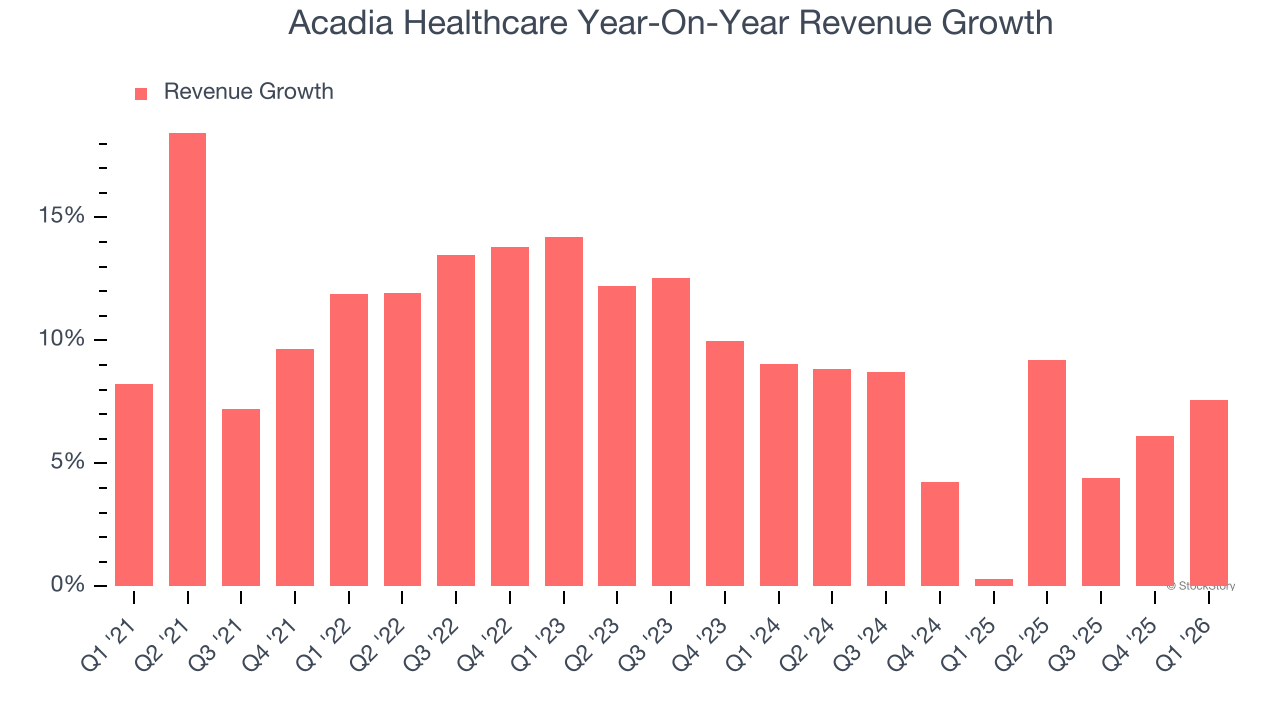

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Acadia Healthcare’s recent performance shows its demand has slowed as its annualized revenue growth of 6.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

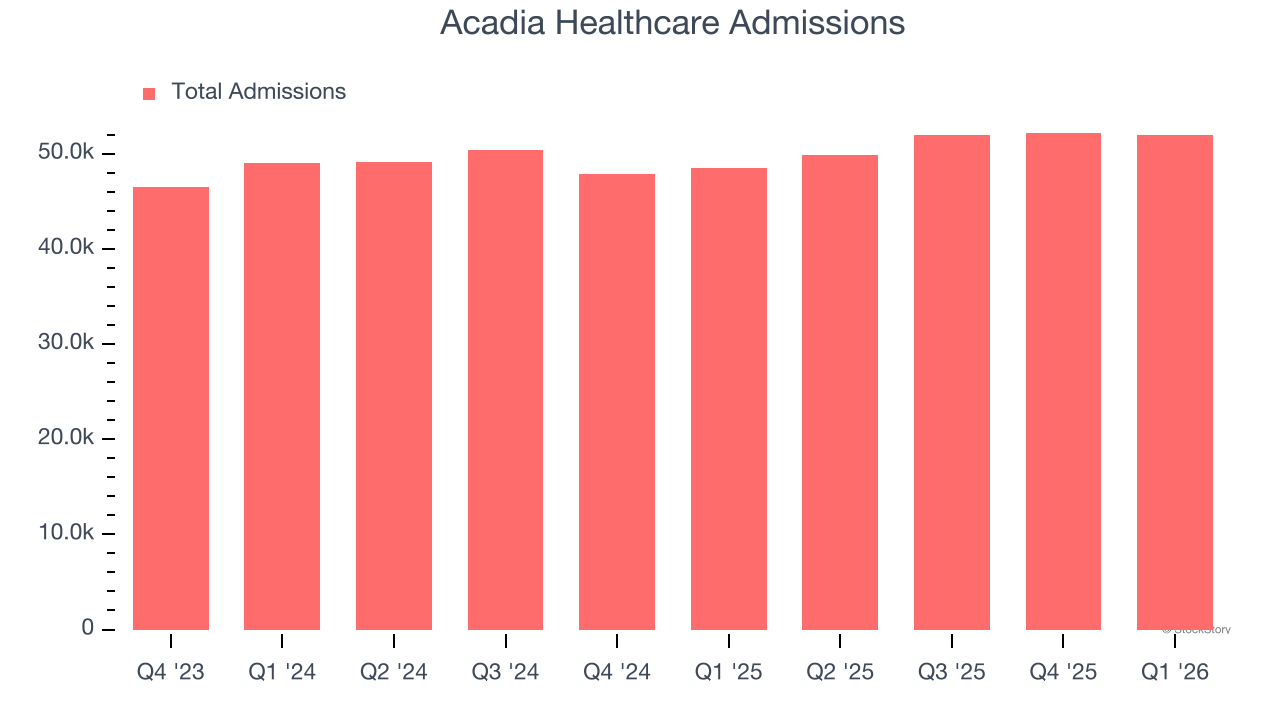

Acadia Healthcare also reports its number of admissions, which reached 51,959 in the latest quarter. Over the last two years, Acadia Healthcare’s admissions averaged 3.8% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Acadia Healthcare reported year-on-year revenue growth of 7.6%, and its $828.8 million of revenue exceeded Wall Street’s estimates by 0.6%. Company management is currently guiding for a 3.1% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

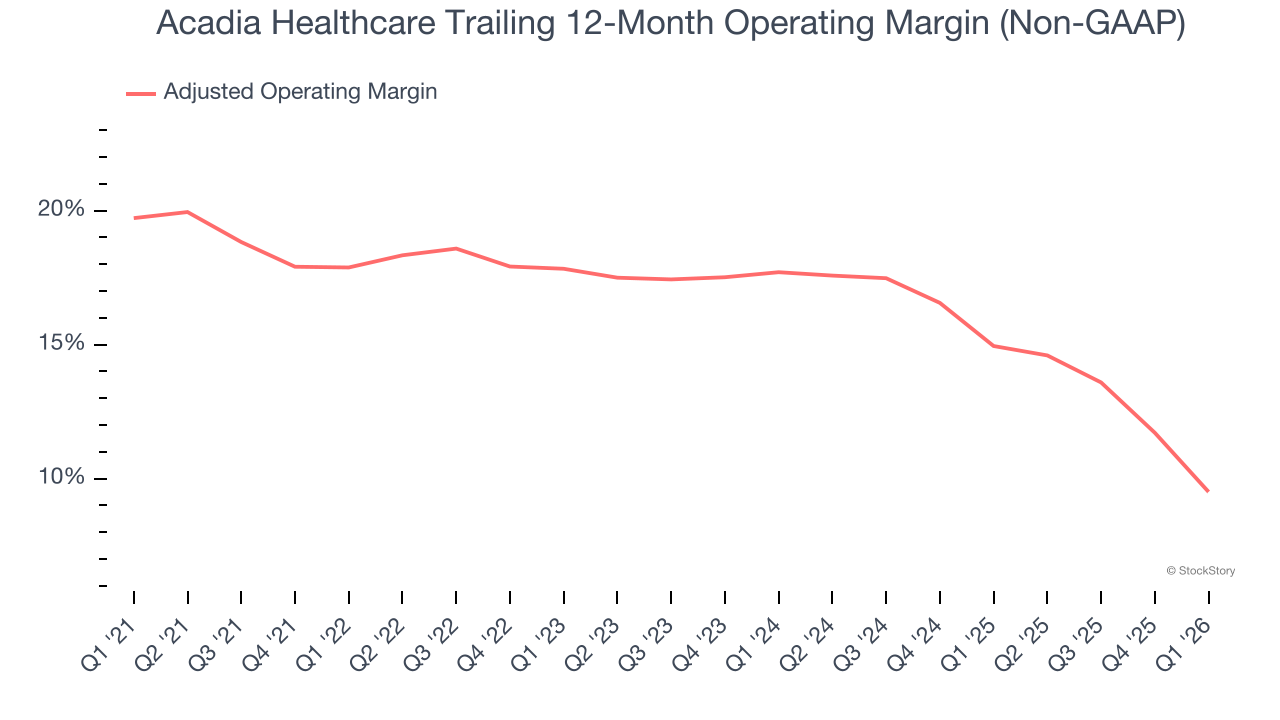

Adjusted Operating Margin

Acadia Healthcare has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average adjusted operating margin of 15.3%.

Looking at the trend in its profitability, Acadia Healthcare’s adjusted operating margin decreased by 8.4 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 8.2 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q1, Acadia Healthcare generated an adjusted operating margin profit margin of 1.3%, down 8.9 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

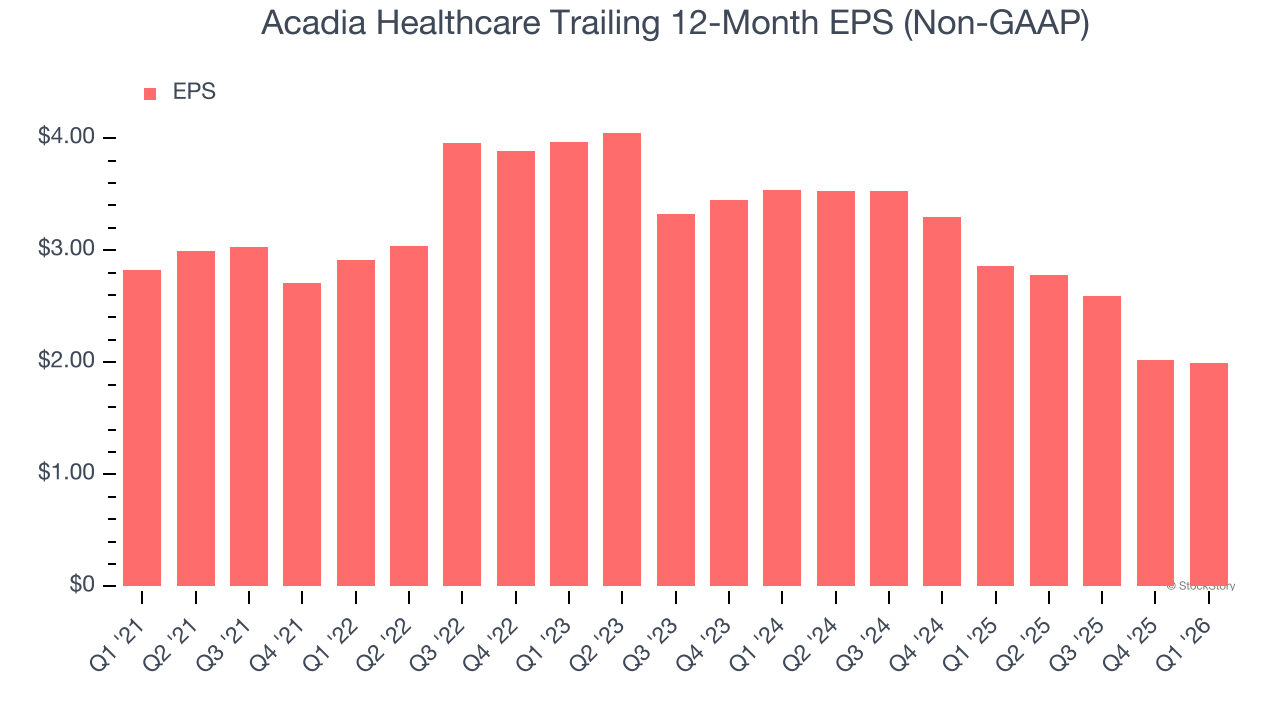

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Acadia Healthcare, its EPS declined by 6.7% annually over the last five years while its revenue grew by 9.6%. This tells us the company became less profitable on a per-share basis as it expanded.

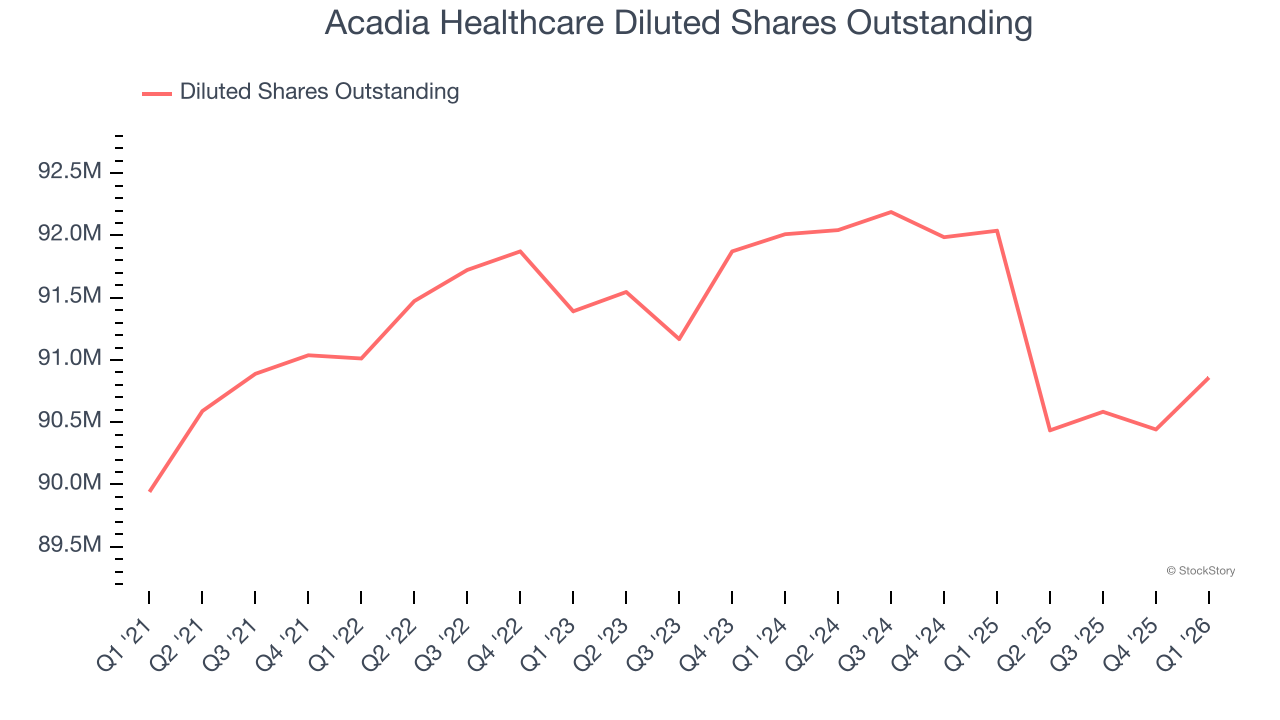

We can take a deeper look into Acadia Healthcare’s earnings to better understand the drivers of its performance. As we mentioned earlier, Acadia Healthcare’s adjusted operating margin declined by 8.4 percentage points over the last five years. Its share count also grew by 1%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q1, Acadia Healthcare reported adjusted EPS of $0.37, down from $0.40 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Acadia Healthcare’s full-year EPS of $1.99 to shrink by 23.9%. This is unusual as its revenue and operating margin are anticipated to increase, signaling the fall likely stems from "below-the-line" items such as taxes.

Key Takeaways from Acadia Healthcare’s Q1 Results

It was good to see Acadia Healthcare beat analysts’ EPS expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 5.9% to $26.60 immediately after reporting.

Acadia Healthcare didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).