Casual restaurant chain Brinker International (NYSE: EAT) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 3.2% year on year to $1.47 billion. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $5.8 billion at the midpoint. Its non-GAAP profit of $2.90 per share was 1.3% above analysts’ consensus estimates.

Is now the time to buy Brinker International? Find out by accessing our full research report, it’s free.

Brinker International (EAT) Q1 CY2026 Highlights:

- Revenue: $1.47 billion vs analyst estimates of $1.47 billion (3.2% year-on-year growth, in line)

- Adjusted EPS: $2.90 vs analyst estimates of $2.86 (1.3% beat)

- Adjusted EBITDA: $223.7 million vs analyst estimates of $222.4 million (15.2% margin, 0.6% beat)

- The company slightly lifted its revenue guidance for the full year to $5.8 billion at the midpoint from $5.80 billion

- Management slightly raised its full-year Adjusted EPS guidance to $10.73 at the midpoint

- Operating Margin: 11.3%, in line with the same quarter last year

- Free Cash Flow Margin: 12.3%, up from 9.3% in the same quarter last year

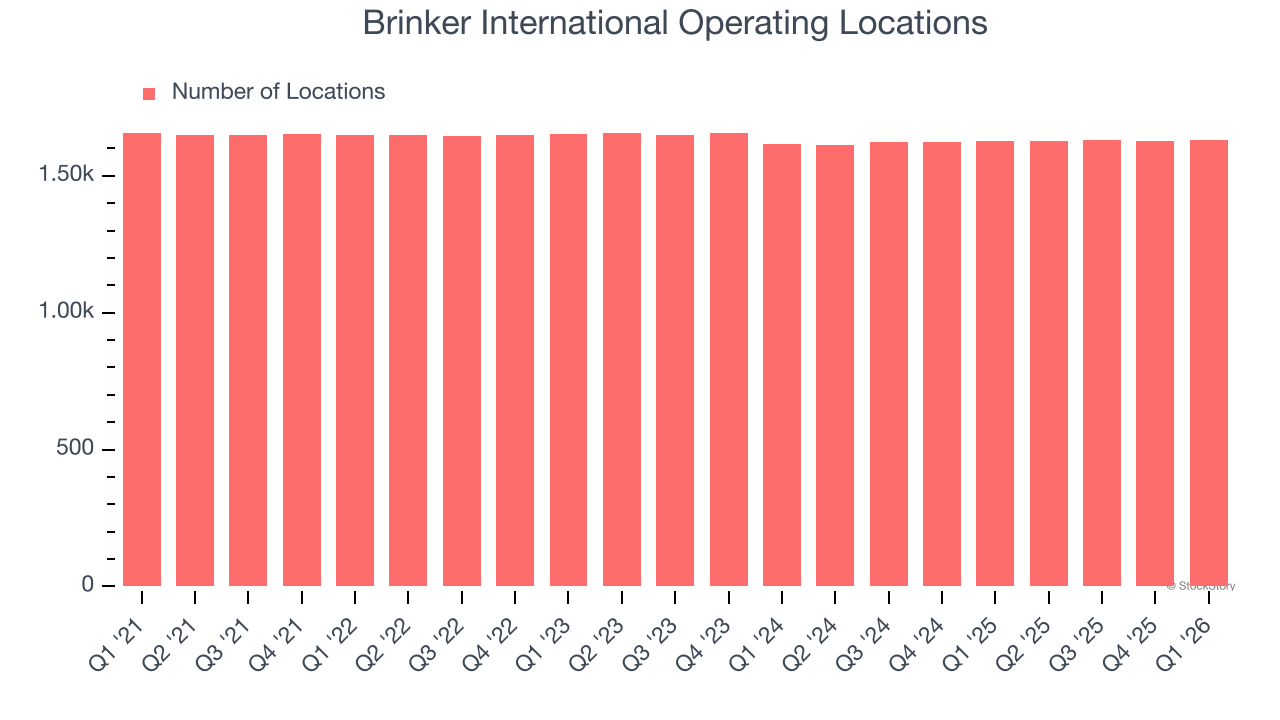

- Locations: 1,632 at quarter end, up from 1,626 in the same quarter last year

- Same-Store Sales rose 3.3% year on year (25.9% in the same quarter last year)

- Market Capitalization: $5.62 billion

"Chili's delivered its 20th consecutive quarter of same-store sales growth, up 4%, lapping a 31% increase a year ago," said Kevin Hochman, President and CEO of Brinker International.

Company Overview

Founded by Norman Brinker in Dallas, Brinker International (NYSE: EAT) is a casual restaurant chain that operates the Chili’s, Maggiano’s Little Italy, and It’s Just Wings banners.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $5.73 billion in revenue over the past 12 months, Brinker International is one of the larger restaurant chains in the industry and benefits from a well-known brand that influences consumer purchasing decisions.

As you can see below, Brinker International grew its sales at a decent 8.7% compounded annual growth rate over the last seven years despite not opening many new restaurants, implying that growth was driven by higher sales at existing, established dining locations.

This quarter, Brinker International grew its revenue by 3.2% year on year, and its $1.47 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.5% over the next 12 months, a deceleration versus the last seven years. This projection is underwhelming and indicates its menu offerings will face some demand challenges.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Brinker International listed 1,632 locations in the latest quarter and has kept its restaurant count flat over the last two years while other restaurant businesses have opted for growth.

When a chain doesn’t open many new restaurants, it usually means there’s stable demand for its meals and it’s focused on improving operational efficiency to increase profitability.

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth at restaurants open for at least a year.

Brinker International has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 15.4%. Given its flat restaurant base over the same period, this performance stems from a mixture of higher prices and increased foot traffic at existing locations.

In the latest quarter, Brinker International’s same-store sales rose 3.3% year on year. This was a meaningful deceleration from its historical levels. We’ll be watching closely to see if Brinker International can reaccelerate growth.

Key Takeaways from Brinker International’s Q1 Results

We struggled to find many positives in these results. Overall, this was a weaker quarter. The stock traded up 2.8% to $132.73 immediately after reporting.

So should you invest in Brinker International right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).