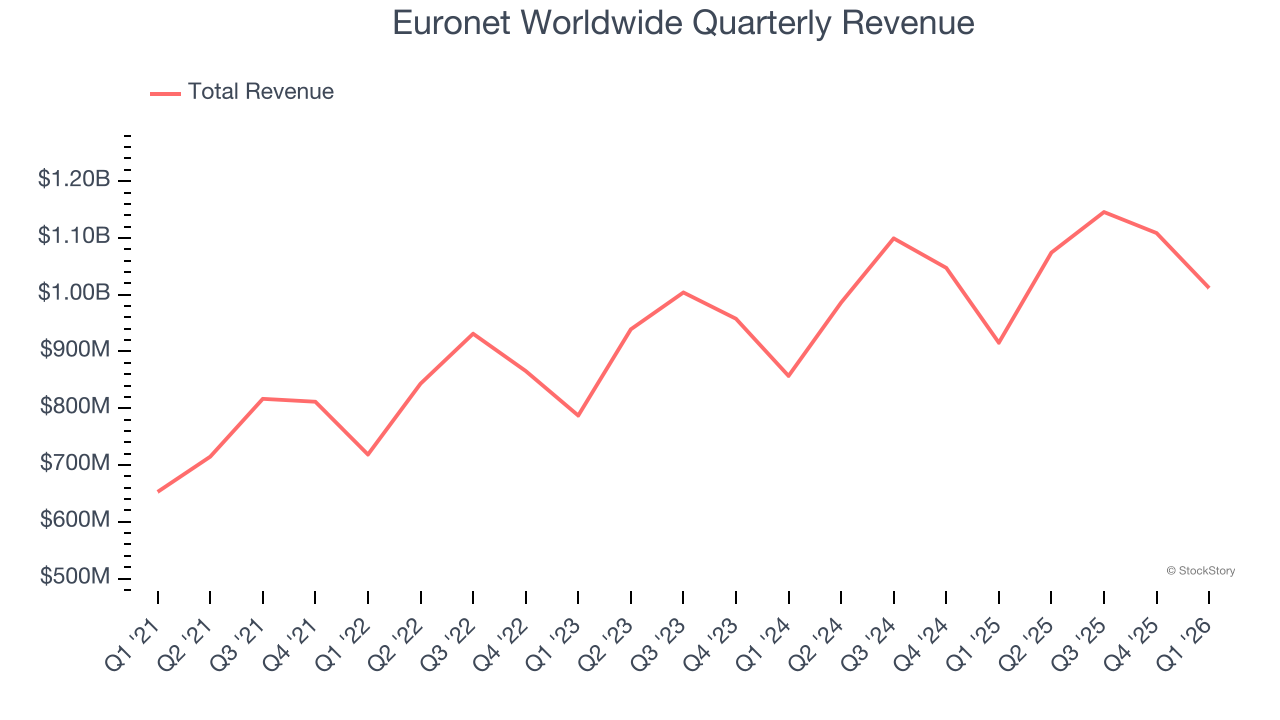

Financial technology provider Euronet Worldwide (NASDAQ: EEFT) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 10.5% year on year to $1.01 billion. Its non-GAAP profit of $1.58 per share was 8.5% above analysts’ consensus estimates.

Is now the time to buy Euronet Worldwide? Find out by accessing our full research report, it’s free.

Euronet Worldwide (EEFT) Q1 CY2026 Highlights:

- Revenue: $1.01 billion vs analyst estimates of $969.7 million (10.5% year-on-year growth, 4.3% beat)

- Pre-tax Profit: $66.3 million (6.6% margin)

- Adjusted EPS: $1.58 vs analyst estimates of $1.46 (8.5% beat)

- Market Capitalization: $2.87 billion

“We believe Euronet’s first quarter 2026 results reflect meaningful progress across our growth initiatives as we continue to navigate a challenging geopolitical and economic backdrop,” said Michael J. Brown, Euronet’s Chairman and Chief Executive Officer.

Company Overview

Operating a global network of over 47,000 ATMs and 821,000 point-of-sale terminals across more than 60 countries, Euronet Worldwide (NASDAQ: EEFT) provides electronic payment solutions including ATM services, prepaid product processing, and international money transfer services.

Revenue Growth

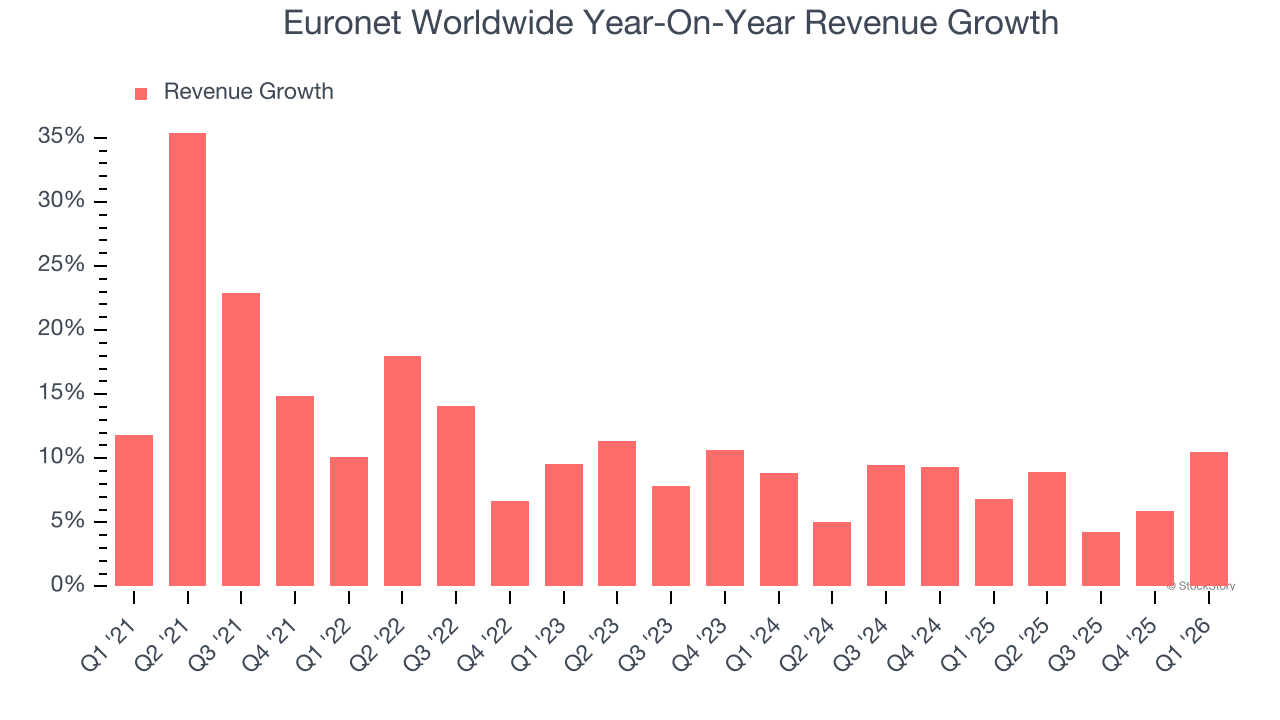

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Euronet Worldwide’s revenue grew at a solid 11.2% compounded annual growth rate over the last five years. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Euronet Worldwide’s recent performance shows its demand has slowed as its annualized revenue growth of 7.5% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Euronet Worldwide reported year-on-year revenue growth of 10.5%, and its $1.01 billion of revenue exceeded Wall Street’s estimates by 4.3%.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Key Takeaways from Euronet Worldwide’s Q1 Results

We enjoyed seeing Euronet Worldwide beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its EBITDA missed. Zooming out, we think this was a solid print. The stock traded up 1.2% to $76.60 immediately after reporting.

Sure, Euronet Worldwide had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).