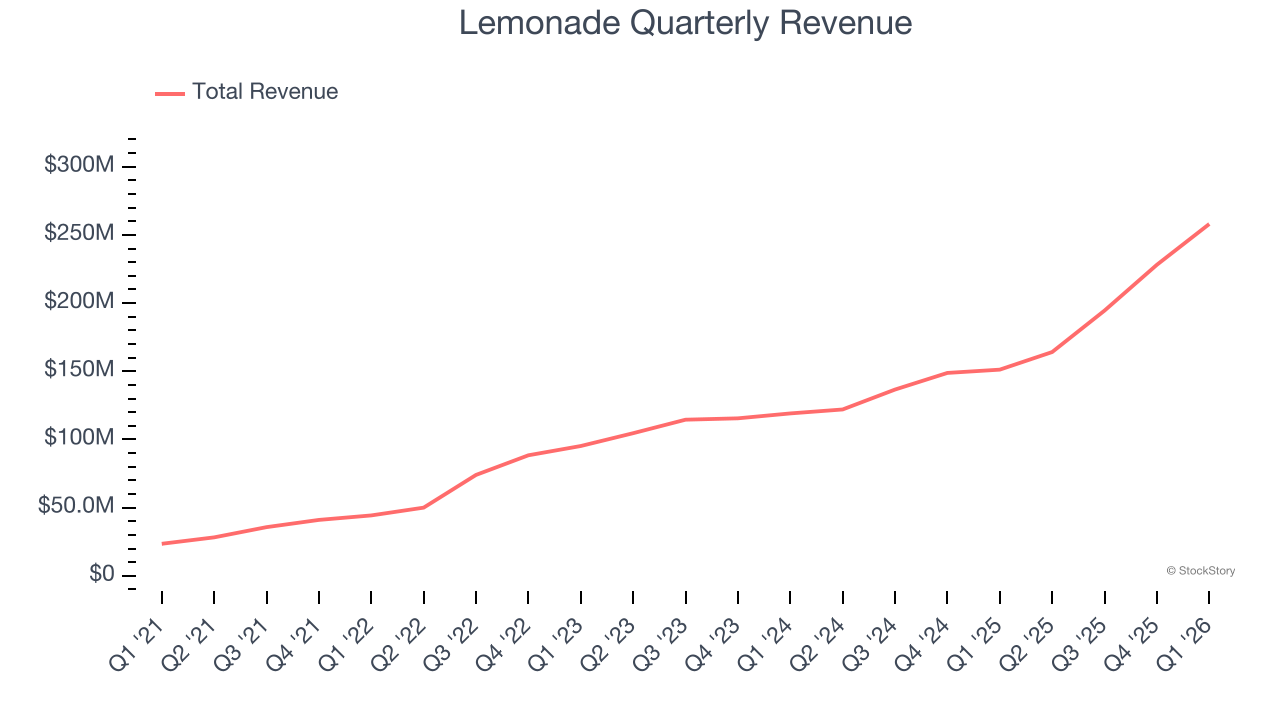

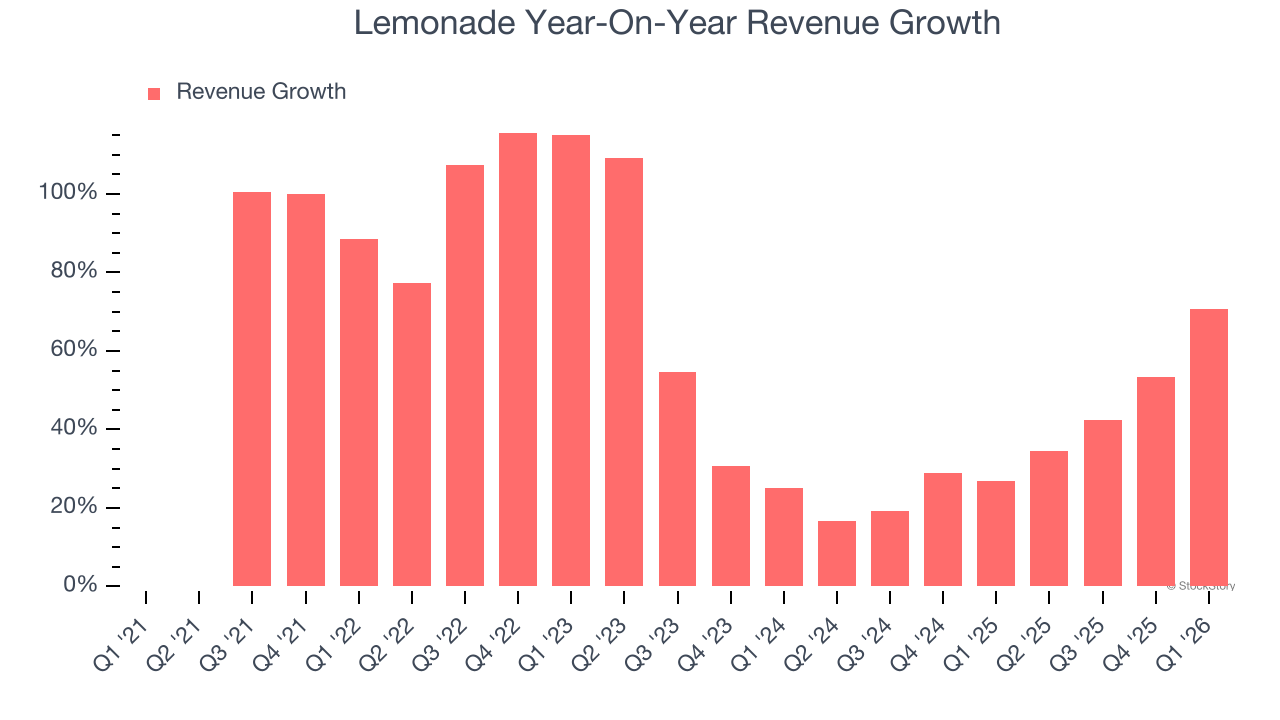

Digital insurance provider Lemonade (NYSE: LMND) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 70.6% year on year to $258 million. Its GAAP loss of $0.47 per share was 17% above analysts’ consensus estimates.

Is now the time to buy Lemonade? Find out by accessing our full research report, it’s free.

Lemonade (LMND) Q1 CY2026 Highlights:

- Net Premiums Earned: $212.6 million vs analyst estimates of $204.4 million (104% year-on-year growth, 4% beat)

- Revenue: $258 million vs analyst estimates of $251.9 million (70.6% year-on-year growth, 2.4% beat)

- Pre-tax Profit: -$34.6 million (-13.4% margin)

- EPS (GAAP): -$0.47 vs analyst estimates of -$0.57 (17% beat)

- Market Capitalization: $5.05 billion

Company Overview

Built on the principle of giving back unused premiums to charitable causes selected by policyholders, Lemonade (NYSE: LMND) is a technology-driven insurance company that offers homeowners, renters, pet, car, and life insurance through an AI-powered digital platform.

Revenue Growth

Insurance companies generate revenue three ways. The first is the core insurance business itself, represented in the income statement as premiums earned. The second source is investment income from investing the “float” (premiums collected but not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from policy administration, annuities, and other value-added services. Luckily, Lemonade’s revenue grew at an incredible 55.9% compounded annual growth rate over the last five years. Its growth beat the average insurance company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Lemonade’s annualized revenue growth of 36.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Lemonade reported magnificent year-on-year revenue growth of 70.6%, and its $258 million of revenue beat Wall Street’s estimates by 2.4%.

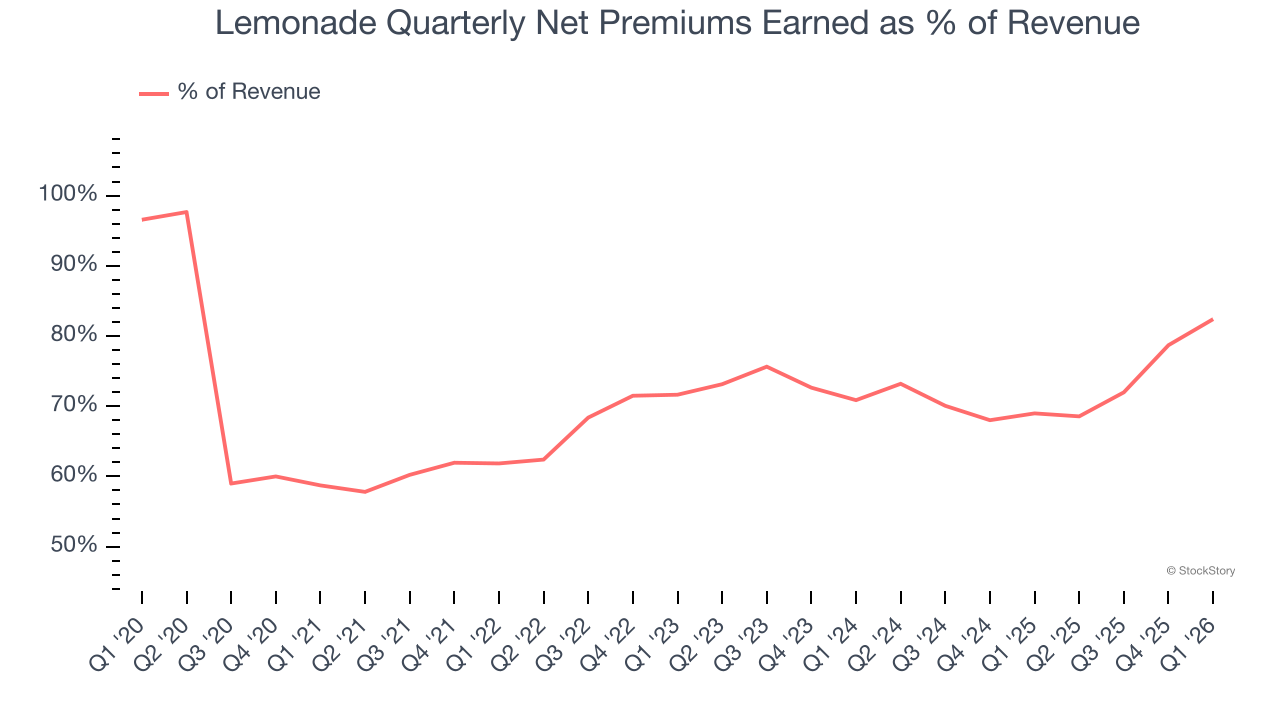

Net premiums earned made up 72.2% of the company’s total revenue during the last five years, meaning insurance operations are Lemonade’s largest source of revenue.

Markets consistently prioritize net premiums earned growth over investment and fee income, recognizing its superior quality as a core indicator of the company’s underwriting success and market penetration.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Net Premiums Earned

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are:

- Gross premiums - what’s ceded to reinsurers as a risk mitigation and transfer strategy

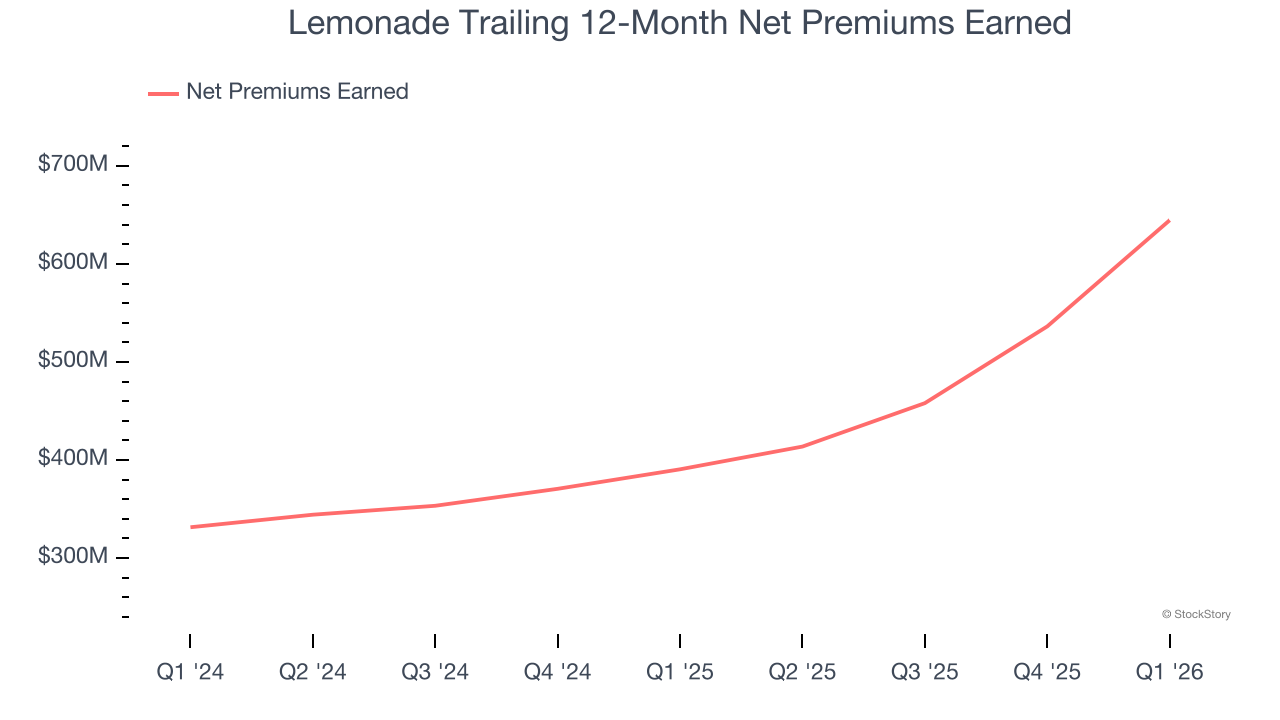

Lemonade’s net premiums earned has grown at a 57.8% annualized rate over the last five years, much better than the broader insurance industry and faster than its total revenue.

When analyzing Lemonade’s net premiums earned over the last two years, we can see that growth decelerated to 39.5% annually. Since two-year net premiums earned grew faster than total revenue over this period, it's implied that other line items such as investment income grew at a slower rate. These additional streams do play a key role in the bottom line, but their impact can vary. While some firms have excelled in consistently investing their float, sudden shifts in the fixed income and equity markets can heavily sway short-term performance.

In Q1, Lemonade produced $212.6 million of net premiums earned, up a hearty 104% year on year and topping Wall Street Consensus estimates by 4%.

Key Takeaways from Lemonade’s Q1 Results

We were impressed by how significantly Lemonade blew past analysts’ net premiums earned expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 3.4% to $68 immediately after reporting.

Lemonade had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).