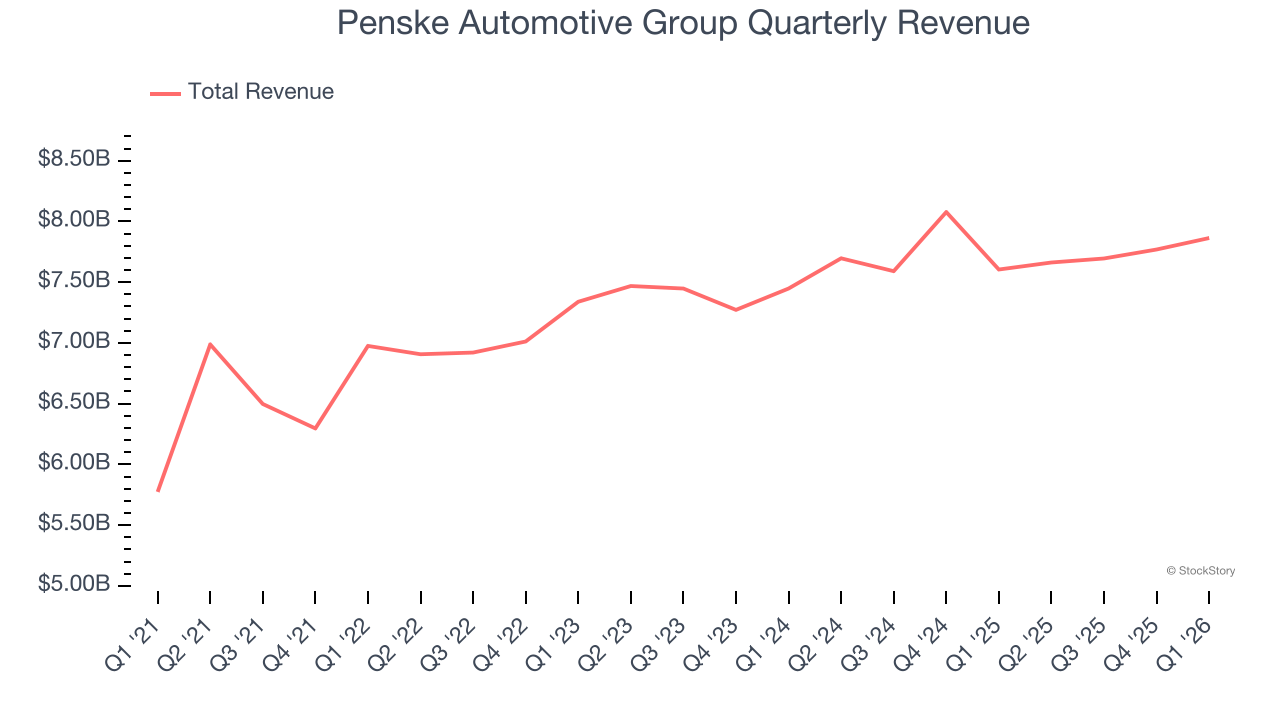

Global automotive retailer Penske Automotive Group (NYSE: PAG) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 3.4% year on year to $7.86 billion. Its GAAP profit of $3.56 per share was 20.9% above analysts’ consensus estimates.

Is now the time to buy Penske Automotive Group? Find out by accessing our full research report, it’s free.

Penske Automotive Group (PAG) Q1 CY2026 Highlights:

- Revenue: $7.86 billion vs analyst estimates of $7.65 billion (3.4% year-on-year growth, 2.8% beat)

- EPS (GAAP): $3.56 vs analyst estimates of $2.95 (20.9% beat)

- Adjusted EBITDA: $349.5 million vs analyst estimates of $333.8 million (4.4% margin, 4.7% beat)

- Operating Margin: 3.7%, in line with the same quarter last year

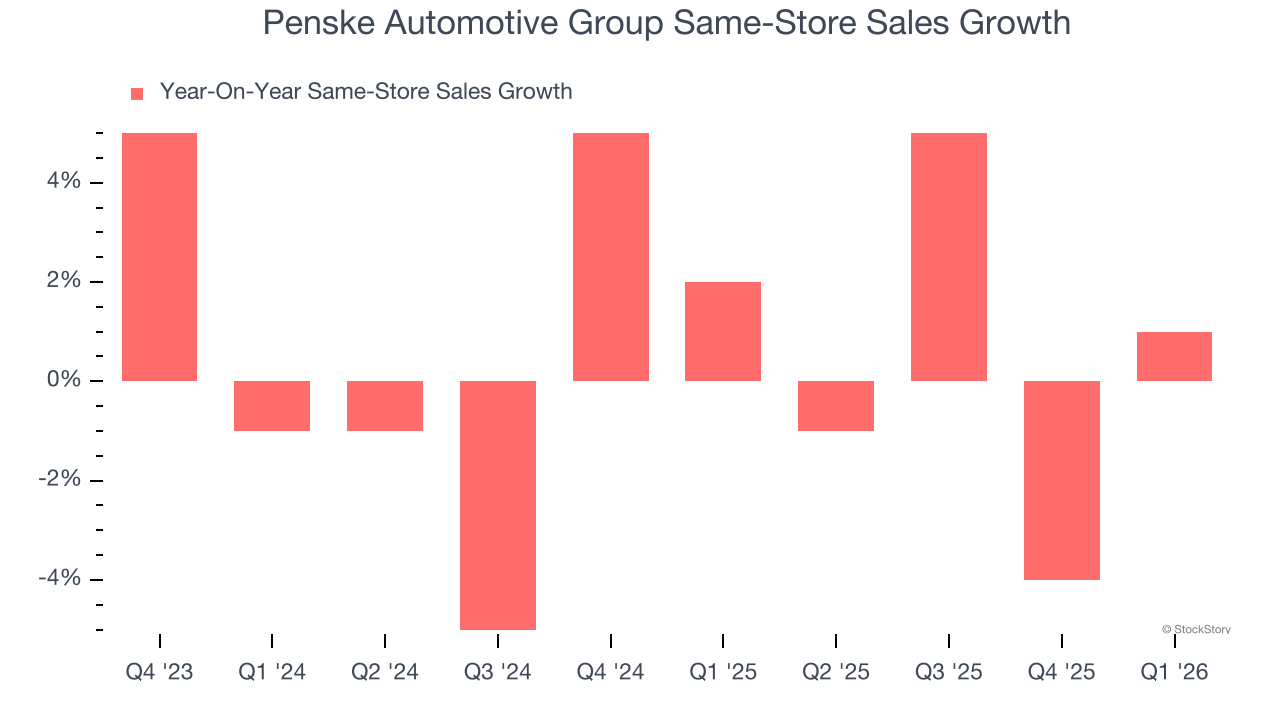

- Same-Store Sales rose 1% year on year (2% in the same quarter last year)

- Market Capitalization: $10.62 billion

Company Overview

With a diverse global network spanning the US, UK, Canada, Germany, Italy, Japan, and Australia, Penske Automotive Group (NYSE: PAG) operates automotive and commercial truck dealerships across the globe, selling new and used vehicles while providing service, parts, and financing options.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $30.99 billion in revenue over the past 12 months, Penske Automotive Group is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. To expand meaningfully, Penske Automotive Group likely needs to tweak its prices or enter new markets.

As you can see below, Penske Automotive Group’s 3.2% annualized revenue growth over the last three years was sluggish.

This quarter, Penske Automotive Group reported modest year-on-year revenue growth of 3.4% but beat Wall Street’s estimates by 2.8%.

Looking ahead, sell-side analysts expect revenue to grow 2.5% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and indicates its newer products will not lead to better top-line performance yet.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Store Performance

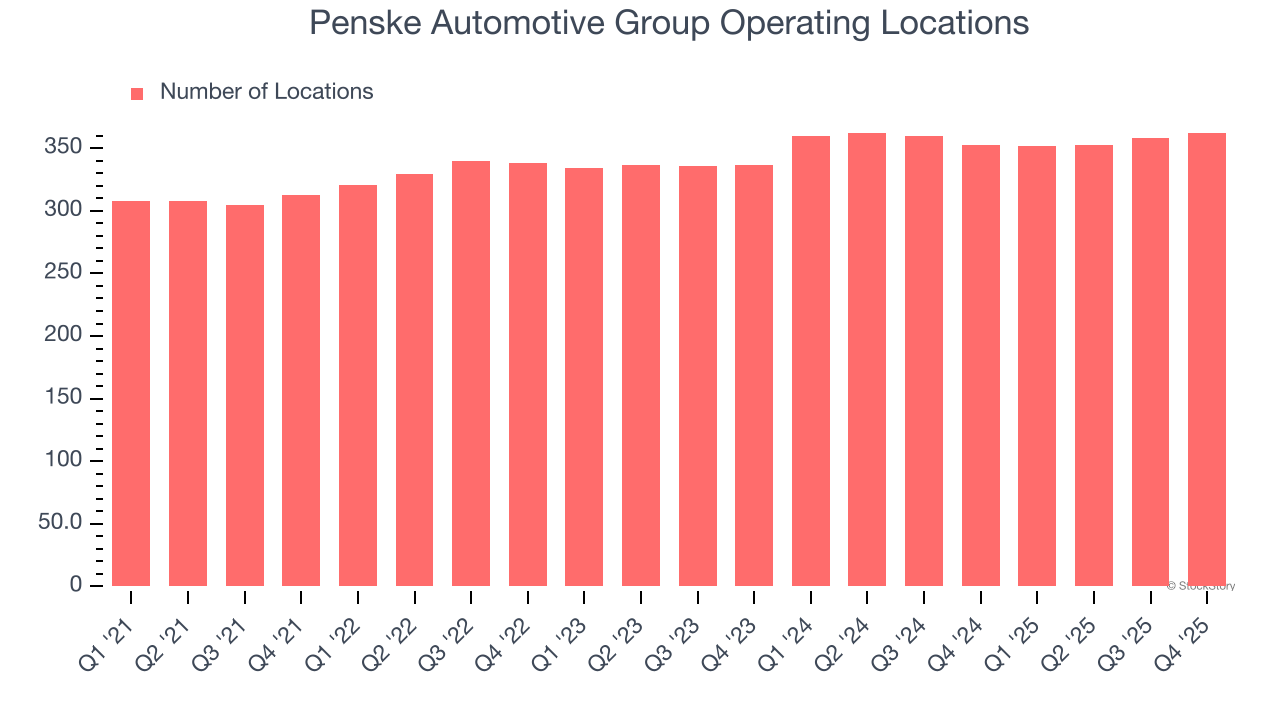

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Over the last two years, Penske Automotive Group opened new stores quickly, averaging 2.4% annual growth. This was faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Note that Penske Automotive Group reports its store count intermittently, so some data points are missing in the chart below.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Penske Automotive Group’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. Penske Automotive Group should consider improving its foot traffic and efficiency before expanding its store base.

In the latest quarter, Penske Automotive Group’s same-store sales rose 1% year on year. This performance was more or less in line with its historical levels.

Key Takeaways from Penske Automotive Group’s Q1 Results

We enjoyed seeing Penske Automotive Group beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its gross margin was in line. Zooming out, we think this was a solid print. The stock traded up 2.6% to $165.80 immediately after reporting.

Indeed, Penske Automotive Group had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).